Latin America looks set for a slowdown in bond issuance this year as falling commodity prices and a crisis in Brazil take their toll on issuers, but there are some bright spots where the market could still grow.

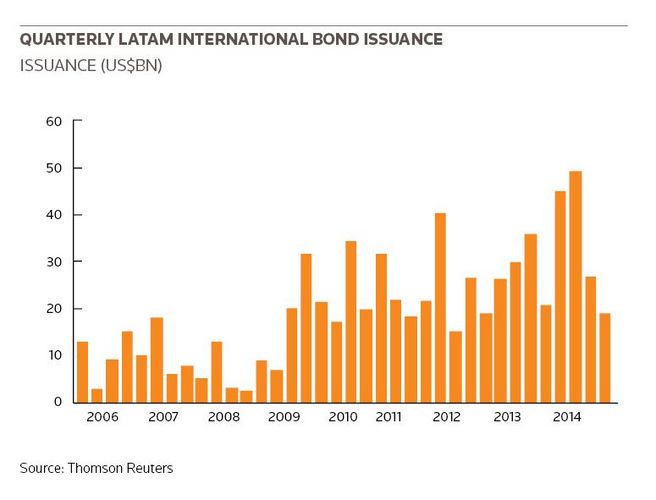

Latin America’s bond markets have enjoyed exceptional growth since the financial crisis, with a diversified supply of sovereign and corporate issuers driving total issuance in the region from US$24.3bn in 2008 to US$139.8bn in 2014.

However, as political and economic headwinds take their toll on Brazil, which has historically been the most active country for issuance, market participants are bracing themselves for a significant drop in volume this year.

“We have had an unusually slow start to the year, although Latin America primary had caught up in volume terms with 2014 by the end of February. But the number of issues in the region is still trailing last year, mainly due to the complete absence of Brazil.

”In addition, some of the bigger corporate issuers appear to be less active, despite the very low interest rate environment. The lack of clear supply, especially from Brazil, leaves investors struggling to find ways to deploy excess cash. Simply put, there just aren’t as many issuers with immediate financing needs as there have been in previous years,” said Carlyle Peake, head of Latin America syndicate at BBVA.

The likelihood of a slowdown has been apparent for some time, and while 2014 was a record year, it was also a year of two halves, with record-breaking issuance in the first two quarters, followed by a sharp decline in the second half. With US$44.9bn issued in the first quarter and US$49bn in the second, issuance fell dramatically to US$26.8bn in Q3 and US$19bn in Q4.

Falling bonds

The fall in bond issuance in the region has been driven by multiple factors, but the political and economic challenges facing Brazil, coupled with a high-profile corporate scandal, are likely to have played a significant role. In October, Brazil’s socialist leader Dilma Rousseff secured a second term after narrowly winning the presidential election, but her government is now struggling to deal with economic recession.

Meanwhile, Brazilian oil giant Petrobras, previously a major bond issuer in Latin America, has become embroiled in a massive bribery scandal, leading to the resignation of its chief executive in February. (See separate chapter on Petrobras.)

“Whether it is because of investor disappointment with the election outcome and a belief that another four years of the current government won’t result in growth in Brazil, or the Petrobras situation, which doesn’t look like it will resolve itself any time soon, issuance in Brazil is expected to be much lower this year,” said Mark Tuttle, head of Latin America debt capital markets at UBS.

A slowdown in Brazil will have a marked impact on issuance for the whole region, given that the country has boasted the largest bond market in Latin America since 2009, beaten only narrowly by Mexico in 2013.

With US$44.6bn issued out of Brazil last year, the country accounted for 31.9% of the regional market, followed by Mexico with 29.7%, according to Thomson Reuters data. With the Petrobras scandal still ongoing, it seems unlikely that Brazil will account for anywhere near the same proportion of the region’s issuance this year.

“Petrobras has historically accounted for as much as 15% of bond issuance in Latin America. At this point it’s fair to assume that it’s unlikely the company will be able to raise as much as last year. Brazil also faces a weaker macroeconomic environment and investor sentiment, which reduces the number of potential issuers. It will probably be 2016 before we see Brazilian issuers return to the market at the same level as previous years,” said Lisandro Miguens, head of Latin America debt capital markets at JP Morgan.

Waning appetite

Falling oil and commodity prices are also playing their part in the declining appetite for new issuance across Latin America, given the large number of companies with businesses linked to commodities. With prices sliding, banks report that many issuers have been reassessing their strategies and scaling back any financing plans.

In Mexico, the government last year enacted reforms to open up its energy sector to new competitors and break the monopoly of state-run energy giant Pemex, a major bond issuer. But as the price of oil plummeted from nearly US$100 per barrel in mid-2014 to less than US$50 per barrel, the popularity of commodity-linked debt has fallen.

“Our expectation was that there would be more issuance out of Mexico as large multinationals sought to carve out a share of the energy market on the back of the energy reforms, but the fall in the price of oil has naturally caused investors to reconsider the value of new projects. New investment into Mexico will therefore be delayed until the oil price stabilises,” said Tuttle at UBS.

Move over bonds, here come loans

Given the impact of the crisis in Brazil and falling oil prices, some see a shift away from bonds towards other markets, including loans. While bonds had previously tended to be more popular than loans due to low interest rates and the reluctance of many banks to lend at a time when balance sheets were being restructured, the loan market now appears to be gaining ground.

Syndicated loan issuance in Latin America reached US$31.7bn last year, up from US$22.9bn in 2013, according to Thomson Reuters data.

“Given the volatility in debt capital markets, issuers are turning to local markets and syndicated lending. The local debt markets in Brazil and Mexico are fairly deep and liquid, with less volatility and spread widening, while the loan market is also more liquid than it has been for some time. I expect substantial volume to move from the bond market to the loan market this year,” said Miguens of JP Morgan.

Chile on the rise

While Latin America’s bond market may face a more challenging outlook in 2015 than in previous years, there are some bright spots on the horizon. Last year saw significant year-on-year growth in a number of markets, most notably Chile, where issuance ballooned from US$11.4bn to US$16.1bn, and Venezuela where it grew from just under US$2bn to US$8.5bn.

Chilean retailer Cencosud has already put Chile on the map this year when it issued US$650m of 10-year bonds and US$350m of 30-year bonds in early February, demonstrating the popularity of the country’s corporate debt.

“It is quite rare to see a Chilean corporate do a 30-year issue in the international market because there is no way to hedge it back into local currency. But the Cencosud issue was oversubscribed and really highlighted that investors are inherently looking for yield through longer-dated investments,” said Gabriel Bochi, head of Latin America debt capital markets at BBVA.

Argentina could also see significant activity this year, following two popular issues in February by state-controlled oil company YPF and the City of Buenos Aires. Issuance in Argentina has historically lagged some way behind other countries in Latin America, with just under US$1.5bn issued last year, but some believe that could now change.

“The impact of commodity prices and the situation in Brazil are clearly cause for concern, but overall investors are committed to fixed income in this region”

“These two issues by YPF and the City of Buenos Aires showed that there is a diversified global pool of real money and institutional investors with an appetite for Argentine debt. Both deals were widely distributed in Europe and the US, and it could open the door to other Argentine issuers to consider financing through the bond market as things get settled,” said BBVA’s Peake.

These positive developments in Chile and Argentina give market participants some cause for optimism that an overall slowdown in issuance this year will be a short-term blip rather than a long-term trend. Another positive surprise could come from mergers and acquisitions-related bond issuance, which historically accounted for only a small proportion of activity in Latin America, according to JP Morgan’s Miguens.

“There is little doubt that issuance this year will be down from 2014 and it’s hard to see volume getting back to US$140bn any time soon, but we do expect to see more M&A activity in the region, which could translate into new issuance and reduce the gap between 2014 and 2015 volumes,” said Miguens.

“The impact of commodity prices and the situation in Brazil are clearly cause for concern, but overall investors are committed to fixed income in this region. We will continue to see investment spending to improve infrastructure in Latin America and there will be financing that comes with that, so there are certainly reasons to be positive,” added Tuttle of UBS.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.