The European high yield market is coming of age. A broader range of companies are looking to extend debt maturities and refinance loans with bonds, while a strained banking community continues to restrict its corporate lending activities. But can the market ever reach the same level of maturity as its US equivalent? Hardeep Dhillon reports.

A total of €32bn of high yield debt was issued in 2009. It is a remarkable feat for a market that only re-opened in July that year. Increasing primary market activity could set new records this year, with forecasts ranging from SG’s €35bn to Barclays Capital’s €40-€45bn.

Issuance now derives from a wider range of industry sectors and geographies. DFS, Virgin Media, Manchester United Football Club, Ladbrokes, Matalan and Gala Coral have launched sterling transactions. Euro deals include US bottle firm Owens-Illinois, engineering group Durr and container shipping firm Hapag-Lloyd from Germany, investment firm Wendel and frozen food retailer Picard Surgelés from France and Hungarian oil and gas group MOL.

“Liquidity both in euro and sterling market is much greater than even a year ago and many European issuers are now largely able to fund themselves in their functional currencies, even for significant amounts, without tapping the US market,” said Arnaud Tresca, head of high yield capital markets at BNP Paribas.

Issuer diversification is growing as more companies turn to the bond markets for the first time. New corporate borrowers include German car parts manufacturer Hella, Spanish environmental biotech company Abengoa, holiday company Thomas Cook and Dutch cable company Ziggo. Debut leveraged buyout refinancings have originated from chemical company Oxea, paper company Nordenia, Spanish helicopter services company Inaer and also Care UK in the sterling market.

The increase in the number of corporates losing investment-grade status is also transforming the foundation of the market. Fallen angels now include household names across Europe, like Michelin and Lufthansa. Their funding requirements will boost volumes, potentially adding between €50bn and €150bn of supply.

Many have already tapped the high-yield markets including, Fiat, Pernod, Renault and Heidelberg Cement. Continental alone issued €3bn across three placements this year and is forecast to issue more debt in the first quarter of 2011 to help refinance around €8bn of syndicated bank loans maturing within the next two years.

Credit Suisse estimates that European high-yield redemptions will gradually rise from €15bn this year and peaking at €23bn in 2014, though leveraged loan redemptions will spike from €6bn to €61bn in Europe, the Middle East and Africa. This could create a huge funding gap for Europe, with roughly €255bn needing to be refinanced between 2013 and 2016.

“There is potential for the bond market to grow because not all of the huge lump of loan maturities will be able to refinance in the loan market,” said Parmeshwar Chadha, fund manager at Newton. “Hence, the European high yield market could possibly double in size in the next four to five years and grow to €300bn.”

Follow the leader

Despite the strong culture for close relationship banking in Europe, the greater impetus toward bank disintermediation is transforming the market to be more in line with the US. “Banks have had to de-lever, reduce balance sheets and constrain loan lending since the credit crisis,” said Eugene Regis, high yield and leveraged finance credit strategist at Barclays Capital. “This is pushing more credits to the bond markets because companies can no longer depend on their traditional sources of financing.”

Roughly 70% of new issues this year have been refinancings of existing debt. This trend will continue, as loans at LBO companies and fallen angels near maturity, he said.

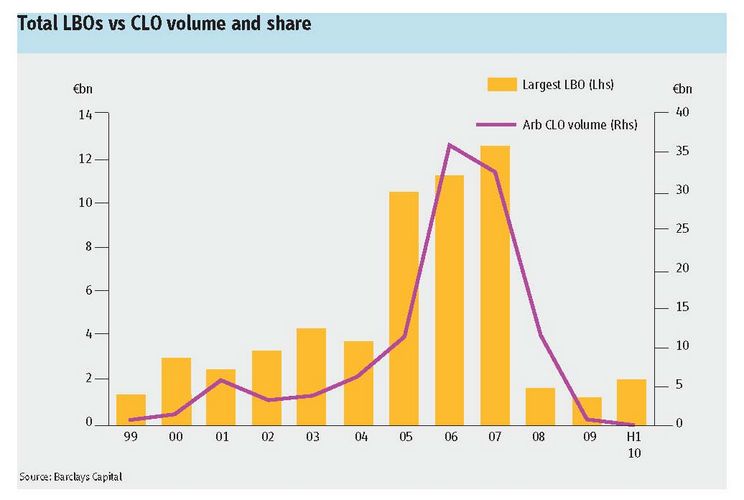

More LBO-type borrowers will look at refinancing in the high-yield bond market next year, he predicted. The return of a stronger LBO market is also possible, though new bond transactions will be smaller than before, Regis said, because of the much-reduced CLO bid compared to the market heights between 2004 and 2007.

The shift of funding towards bonds away from bank loans started in 2009 and is an important dynamic improving the composition of the European high yield market. “A greater diversification in sources of funding is a healthy development and the demise of the CLO and collateralised debt obligation markets is giving European high yield an added impetus and extra liquidity,” said Jonathan Trower, managing director at DC Advisory Partners. “Issuers have more certainty of raising funds in Europe because of the large increase in the size of the euro and sterling investor base.”

As banks face relatively higher funding costs and lending restrictions, corporate issuers are locking in attractive rates and lengthening maturity profiles by accessing the high-yield bond market. “It is a more competitive funding source than the loan market for some borrowers and has the added attraction of no amortisation and no maintenance financial covenants,” said Trower.

New financial regulations are dampening bank appetite to lend to lower rated companies, and high yield financing should become less of a priority due to stricter capital requirements. Basel II has already forced banks to lift the risk weightings of leverage finance assets from 100% to 250% and curbed demand for leveraged lending significantly, which should stay diminished under Basel III, said Jonathan Butler, head of European leveraged finance at Pramerica.

The Capital Requirements Directive III (CRD3) will tighten up the way banks assess the risks connected with their trading book to better reflect the potential losses from adverse market movements in stressed conditions. The rules come into force at the end of 2011 and are expected to result in banks holding three to four times more capital against their trading risk than they currently do. “CRD3 should cause more risk aversion towards leveraged loans which could drive further high-yield issuance,” said Butler.

Issuers, such as chemical company LyondellBasell and TMD Friction, being able to access funding following bankruptcy or restructuring, highlights the high yield market’s importance. Dividend recapitalisation deals have also re-entered the market. The Matalan, Nordenia and Oxea transactions have all been used to help pay down existing debt but also to pay a dividend to company owners. “That was not doable 12 months ago and it shows the market is becoming more mature and more diverse in the use of proceeds,” said Tresca at BNP Paribas.

The European market traditionally lacked diversification compared to the US. However, this is changing, as borrowers from more regions, such as Spain and Eastern Europe, launch transactions. “It is a more diverse market in terms of geographies and by ratings, with deals all the way down to Triple C,” said Tresca. “Event driven issuance will help the market truly take off, however merger and acquisition and LBO activities have so far been limited.”

Reaching down the credit specrum

More companies with ratings at the lower end of the ratings scale are forecast to tap the market. During 2009, mostly Double B rated companies issued in the high-yield bond market, but now a much higher percentage of Single B companies are gaining access. “Last year investors were risk averse, but this year they are more comfortable with risk and looking for yield,” said Butler at Pramerica. “The market has opened up for greater issuance and we will probably see more Single B issuance.”

Because leveraged loans need to be refinanced, the market will continue to see a greater issuance of senior secured bonds, where investor take up has generally been good, predicted Tarun Buxani, portfolio manager at Pramerica. “For new issuers coming to the market, seniority and security can offer good relative value when compared to repeat issuers of unsecured paper with a similar credit rating,” he said. But the more racy deals will still be hard to place as European investors tend to be more risk averse than our US counterparts, he added.

The majority of senior secured transactions were previously issued in the loan market and having more bond deals provides investors with additional diversification. Bonds commonly had no pledge on the assets and were always paid off after the banks got their money back, said Chadha. “Deals now are structured reasonably well, generally better rated and include a first or second lien pledge on assets, so if something goes wrong then recovery rates will be much higher than they were in the past,” he said. “Given the current outlook, it is better to be at the top of the capital structure in secured bonds than the bottom in subordinated or paid-in-kind notes.”

Despite the uncertainty over whether the European market will ever mature to closely resemble US high yield, more global portfolios referencing US and European high yield will appear, said Paul Appleby, head of leveraged finance at Pramerica. Drawing from a global investment universe will allow more asset mangers to take greater advantage of opportunities in European high yield, he said, stimulating overall appetite for, and acceptance of, the asset class in Europe.

“Our integrated investment process looks at both markets together to find the best relative value opportunities from a security level on up across the whole asset class,” he said. “The prudent thing for the next couple of years would be to be more globally positioned and adjust the mix over time.”

The uncertain economic outlook is yet to deter investors from funding junk-rated companies. Strong appetite has seen consistent inflow into high yield funds throughout the year. Demand is a symptom of investors search for better returns. Equity markets are too volatile, while “at a time when interest rates are so low, getting a carry of 7% to 9%, along with a potential of capital appreciation providing a total return of 13% to 15%, is very attractive,” said Chadha.

An alignment of interests across market participants is helping further development of the European market and building momentum for a good period of expansion. “The growth of the market this time seems to be based on firmer foundations because of the diverse nature of the investor, the extent of demand and the reduced reliance on the US-based investor,” said Trower.

All parties – issuers, investors and banks – are pushing towards in same direction: the bond market, said Tresca. “Capital constrained banks do not want to lend as much as before, issuers realise the need for diversification and investors are very eager to put money to work and looking for yields.”