Back from the brink: Perhaps nothing symbolised the global financial meltdown more than the downfall of AIG. But with a little time (ok, four years) and a little help (ok, slightly more than a little), the biggest insurance company in the world has managed to turn Armageddon into opportunity. For pulling off what may be the most spectacular recovery in the history of corporate finance, AIG is IFR’s Americas Issuer of the Year.

To see the full digital edition of the IFR Americas Review of the Year, please click here.

It’s a story that will be talked about for generations. Caught desperately short in the midst of the financial crisis, and suddenly fatally exposed to a tumult shaking the globe, AIG was getting ready to die – and die without much love lost. The poster child for what many saw as the market’s reckless abandonment of first principles, the storied shop might easily have just folded up the tent and disappeared under a cloud of public anger and disgust. All those stupidly unhedged derivatives positions? An initial swagger in the face of disaster that looked a lot like arrogance? If ever there was a Goliath that every David thought deserved its comeuppance, AIG was it.

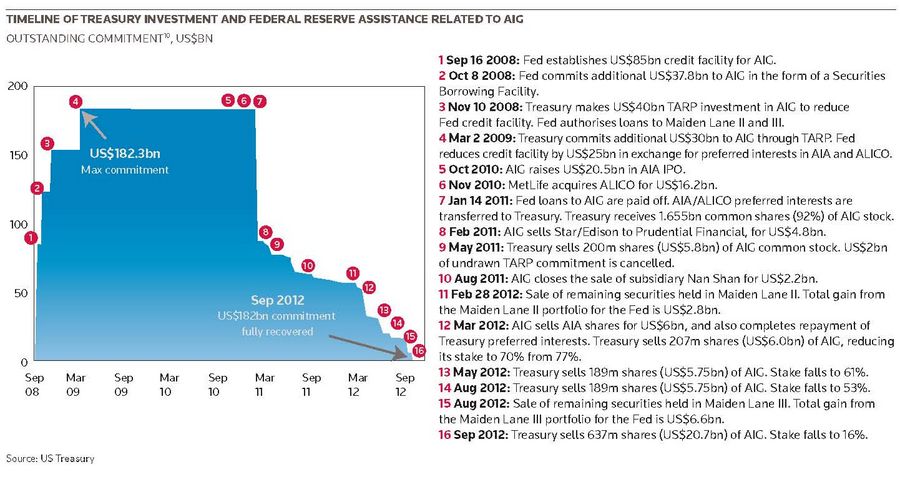

Yet if a week is a long time in politics, four years in the markets is a virtual eternity. And in four years, the insurance firm – once the world’s largest – has transformed itself from pariah to performer, managing to do what very few people thought possible. After taking what turned out to be US$182.3bn in total assistance from the government, it has repaid its debt to US taxpayers (with a handsome profit, to boot).

In a final US$20.7bn sale of stock on September 10 2012, the company achieved full recovery. With great creativity, AIG and its former subsidiaries have sold US$85.7bn of stock in the past three years. The wounded giant has also raised US$21.6bn of debt across its funding complex and secured access to an additional US$21.7bn of bank facilities.

And though the US still holds a 15.9% stake, the company is once again standing on its own two feet, a fully functional player in financial services and the capital markets. Quite simply, AIG is back.

No easy way out

At the time, of course, the way out of the mess was not obvious at all. Standing on the brink of collapse, AIG had exhausted all private market solutions by September 2008, when it turned to the Federal Reserve Bank of New York. The bank stepped in with a whopping US$85bn credit facility that propped up AIG and a number of other wobbly financial institutions, including Goldman Sachs, Bank of America, Citigroup, Societe Generale and Deutsche Bank.

“The Fed facility was based on draft terms for a private sector solution that a couple of leading banks had tried to put together,” said Tim Massad, assistant secretary for financial stability at US Treasury. “It was an incredibly unusual thing for the Fed to provide this kind of assistance. The financial system was really on the precipice.”

The terms of the facility extended to AIG underscored just how dire the situation was. In addition to a rate of Libor plus 850bp on borrowings, the company had to pay a 2% commitment fee, while the facility was structured with a 3% floor on Libor. The bottom line was that AIG would have to pay at least 11.5% on any borrowings – and 2% even if it did not tap the liquidity.

But AIG desperately needed that liquidity. As an insurance company, it was unable to access the Fed discount window like a bank holding company could and would. And in addition to the rapidly escalating amounts of collateral it needed to back up its disastrous derivatives positions, it was saddled with the liabilities of its subsidiaries, which were then relying on the parent’s balance sheet.

As borrowings on the facility peaked at US$72bn within weeks, it became clear that a more viable funding structure was needed.

One part of the solution was the creation of Maiden Lane, a series of specialty purpose vehicles designed to purchase CDOs housed in AIG’s financial products group. Funded by both the Fed and AIG, the arrangements capped exposure and eventually removed US$89.9bn (par amount) of securities.

Another key pillar of the solution turned out to be TARP, which injected capital into the company in November 2008 and again in March 2009. The US$40bn infusion – structured as equity-like 10% perpetual preferred securities and warrants that gave the government a 79.9% equity stake – was used to reduce the size of the Fed credit facility to US$65bn.

Change of terms

And some of the most punitive terms of the facility were dropped. The interest rate was cut to Libor plus 3%, the commitment fee reduced to 0.75%, and the term was extended from two to five years. As collateral, the Fed received preferred equity interests in AIA and ALICO, AIG’s prized Asian and foreign life insurance businesses.

“With access to TARP and the remaining capacity on the Fed facility … we were probably one of the best capitalised insurance companies,” said AIG Treasurer Brian Schreiber. “That helped us get through 2008, 2009. It prevented us from a forced liquidation of the company at a terrible time.”

Even so, the company’s management still faced a seemingly insurmountable wall of debt at time when the global capital markets were in a deep freeze. It was clear that removing the senior secured credit facility was essential to establishing a standalone financing structure, but at the same time it was still dependent on that facility to service its obligations.

“[It] was drawing on facilities to refinance maturities as they were coming due – one of the first things I did was say that doesn’t make a lot of sense,” said Jim Millstein, the former Lazard banker brought in by the Treasury Department in the spring of 2009 to help restructure AIG. “We had to figure out whether there was any equity value to protect.”

One important decision was to focus on AIG’s core businesses and get rid of the more peripheral pieces. While AIG sold American General Finance, a consumer credit firm, in October 2010 for just US$125m, for example, the transaction eliminated some US$17bn of debt in the process.

Another obvious piece of value was AIA – and just as the company was considering spinning the Asian unit off as a listed entity, Prudential stepped up and made an offer in early 2010.

“The Prudential offer came out of left field, but it was a price we were willing to accept,” Millstein said. “We had determined otherwise to do an IPO.”

AIG eventually decided to go with the public offering.

“I distinctly recall saying to the board in the year-and-a-half since the AIG bailout, this is the first time they had two really good options,” said Millstein. “The word from the underwriters on the IPO is things are going to be great. Don’t take a discount.”

Indeed, the Hong Kong listing of AIA exceeded all expectations. Led by Citigroup, Deutsche Bank, Goldman Sachs and Morgan Stanley, the HK$158.7bn (US$20.4bn) listing in October 2010 achieved top-end pricing for a valuation of US$30.55bn.

It was the largest ever Hong Kong-only offering and, at the time, the seventh largest of all time globally. Combined with the sale of ALICO to MetLife for US$16.2bn a week later – partially in the form of MetLife equity – the company suddenly had more than enough to fully repay the Fed.

“From a sequencing standpoint,” said AIG’s CFO David Herzog, “the first thing the company had to do was get the Fed out.”

AIG would not fully repay the Fed’s credit facility until January 2011, but as a condition of the exit it had to demonstrate that it could once again access the credit markets – something it did with unsecured bond offerings in late November 2010.

A US$500m three-year note printed at 3.65% to yield 295bp over Treasuries, inside guidance of 312.5bp and with a negative new issue concession to relevant benchmarks at the time; a US$1.5bn offering came at 6.4% and 362.5bp, a 5bp concession. Bank of America Merrill Lynch, Barclays Capital, Citigroup and Morgan Stanley were joint bookrunners on the debt offering, the first by AIG since August 2008.

Time for selldowns

Next on the agenda was selling the tricky matter of selling off the Treasury’s new stake in AIG.

“The stock wasn’t trading on fundamentals, and there were no institutional holders to speak of. It wasn’t a real indicator of what the value was,” said AIG’s Schreiber.

What was apparent was that the government’s break-even point was US$28.72, and that it was a seller.

“We had every major investment bank saying, we can sell US$20bn, US$30bn of stock. You might have to sell it at US$23 but you maybe you can make it up on the back end’,” said Matt Pendo, the Treasury’s chief investment officer.

“We said over and over again, we are going to recover every single dollar that the US government invested in this company. We’re not selling below our break-even. That was our commitment.”

But with everyone in the market aware of that, it was more than a little complicated to carry off a successful sale. AIG and Treasury undertook what was dubbed a “re-IPO” in May 2011, with shares sold at US$29 – a level that ensured Treasury a profit and reduced its stake to 76.7%. But the quality of the bookbuild and the subsequent poor performance of the shares left many with a bitter taste over the deal. AIG shares immediately broke offer and closed the following day at US$28.28.

JP Morgan, the stabilisation agent, was joined by Bank of America Merrill Lynch, Goldman Sachs and Deutsche Bank as global coordinators on the US$8.7bn offering. But the underwriting syndicate garnered fees of only US$43.5mn.

Meanwhile the overhang from the government position was still a weighty 1.365bn shares. In March 2012, US$6bn in stock was sold – overnight. Citigroup, Credit Suisse and Morgan Stanley were rotated in as joint global coordinators. The accelerated marketing was designed not only to ensure the government a profit, but also to thwart attempts by investors to predict timing and affect pricing. The March sale was structured with a 60-day lock-up agreement, allowing the government to sell again as soon as May 8.

“They were our shares to sell, and we decided when to sell. It was at our discretion and our choice,” said Treasury’s Pendo. “The entire market knows we were a seller. They know we want to get out and they know our break-even price. That was quite a corporate finance challenge.”

Treasury eliminated speculation on timing by conducting an over-the-weekend marketing of the next US$5.8bn stock sale, with a launch after the close in New York on Friday, May 4, and pricing prior to the open Monday. The sale of 163.9m shares to the public was accompanied by a US$2bn repurchase.

A third sell-down of US$5.8bn was scheduled for August. The offering launched on an intra-day basis on August 3, with trading suspended ahead of pricing that evening. The move took advantage of positive momentum on AIG’s second-quarter earnings release the night before, requiring legal advisors to sign off that the stock was properly seasoned. Once again, AIG stepped in to purchase US$3bn of stock, and the government’s stake was reduced to 53%.

The series of sell-downs conditioned the market for the final US$20.7bn sale by Treasury in September that reduced its holdings to 15.9%, and allowed the government to mark a US$15bn profit on the bailout – a result that only a very few would have predicted when the messy financial crisis first took hold.

Disenchanted

Of course, the AIG bailout didn’t go smoothly for everyone.

Traditional long-only fund complexes had not surprisingly become disenchanted with AIG. First irked by the lack of disclosure surrounding the company’s derivatives exposure, which began the troubles, they had also seen their equity stakes diluted by the government’s investment as well as a 1-for-20 reverse stock split.

Indeed, one remarkable aspect of all is that the government’s recovery came largely on the back of hedge funds, with little (if any) participation by traditional funds until very late in the game.

“I think that there was a broad awareness early in the year that AIG was materially under-owned in the long-only community,” said one ECM banker who worked on the AIG stock sales. “A lot of hedge funds took a technical view early in the year that AIG was undervalued, and that all or a lot of the long-only that owned pre-2007, pre-2008, eventually would have to come into the name.”

And with that eventual return of traditional investor funds, the company will have truly completed its remarkable comeback from toxic asset to valued holding. AIG’s Herzog does not think it will take much longer.

“I believe our current investor-base are long-term holders. But they know there will be a point in time, because of AIG’s performance, that large, long-only complexes will have to end up owning AIG,” he said. “Because there will be too much tracking error in their benchmarks not to own it.”