Just two years after regaining access to markets, ending more than a decade as a financial pariah, Argentina has once again found itself shut off from global capital after a new financial crisis hit the country, forcing it to ask for help from the International Monetary Fund.

The crisis, which has been brewing since the Banco Central de la Republica Argentina ditched inflation targets in December, culminated in a run on the peso.

Three emergency hikes, which took rates to a record 40%, failed to stop the bleeding, leaving Buenos Aires with little option but to call the IMF.

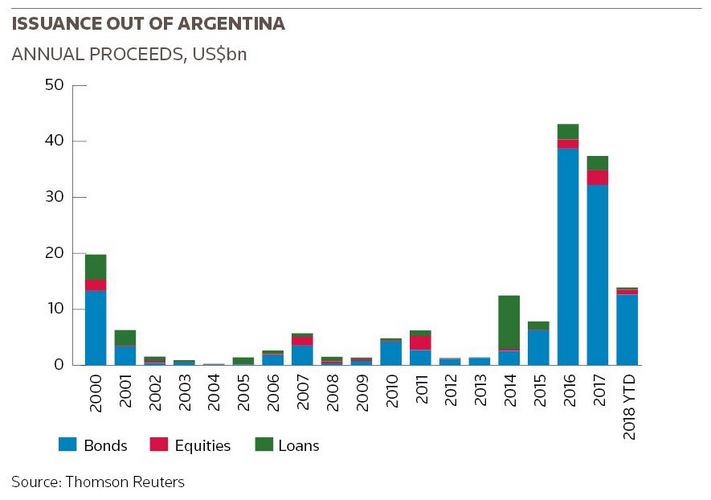

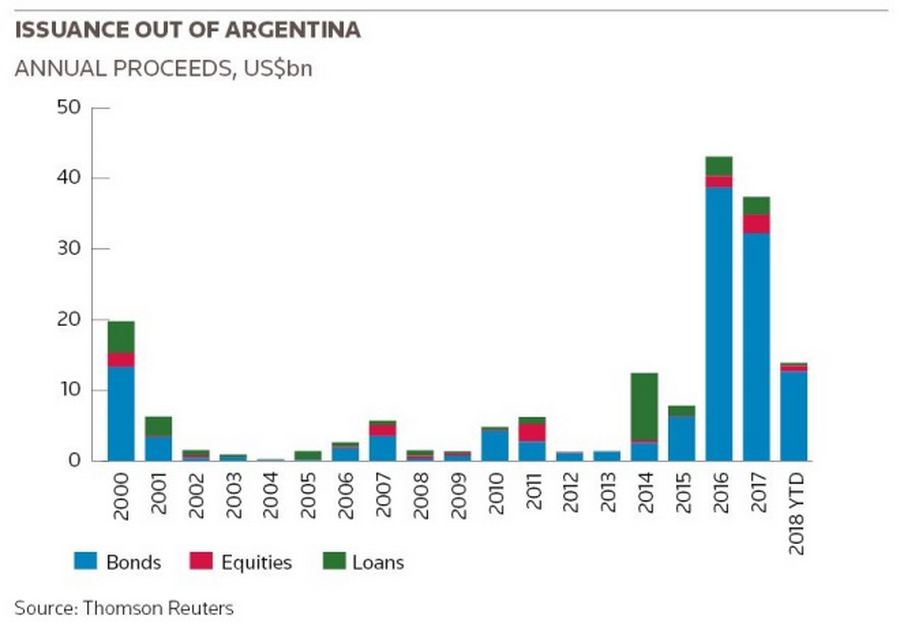

It’s a reversal in fortunes for the country, which briefly became the darling of markets after hatching a historic deal with creditors in March 2016. Almost US$100bn of cross-border bond, loan and equity deals priced in the following two years, injecting much-needed capital into Argentina’s economy after decades of malaise.

Issuers that just months ago had printed deals that were many times oversubscribed are now once again shut out.

The equity capital markets haven’t seen a deal since February, while a healthy pipeline of bond deals that had been planned has now dried up after a series of cancellations over the past fortnight.

“Argentina enjoyed a honeymoon with external markets over the last two years but it now looks like they are going through a separation, with the IMF helping out,” said Donato Guarino, emerging markets strategist at Citigroup. “So much depends now on the dollar and the wider prospects for emerging markets.”

CAUGHT IN THE CROSSHAIRS

While the BCRA’s ditching of inflation targets and policy mis-steps from the government – including ill-judged new taxes on bonds – have contributed to the crisis, Argentina is in many ways a victim of a turning tide of investor sentiment towards emerging markets that has its roots in US monetary policy shifts.

Rate hikes from the US Federal Reserve have reversed capital flows, sucking money back into the world’s largest economy, where investors can earn decent rates in relatively risk-free assets.

As the US dollar rises, currencies such as the Argentinian peso, Turkish lira and Indonesian rupiah have hit record lows.

“While each country has its own domestic issues that could justify the decline, the real culprit is a greenback that has risen sharply,” said Joshua Roberts, an associate at advisory firm JCRA. “Tremors in US trade and monetary policy will not stop sending shockwaves around the world any time soon.”

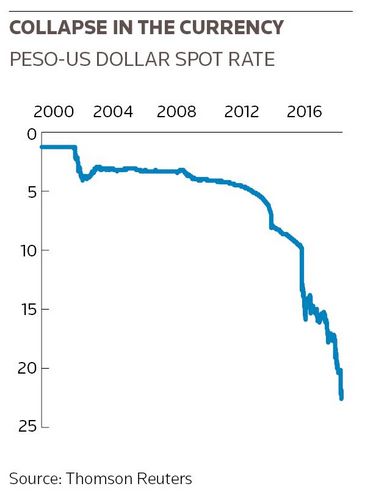

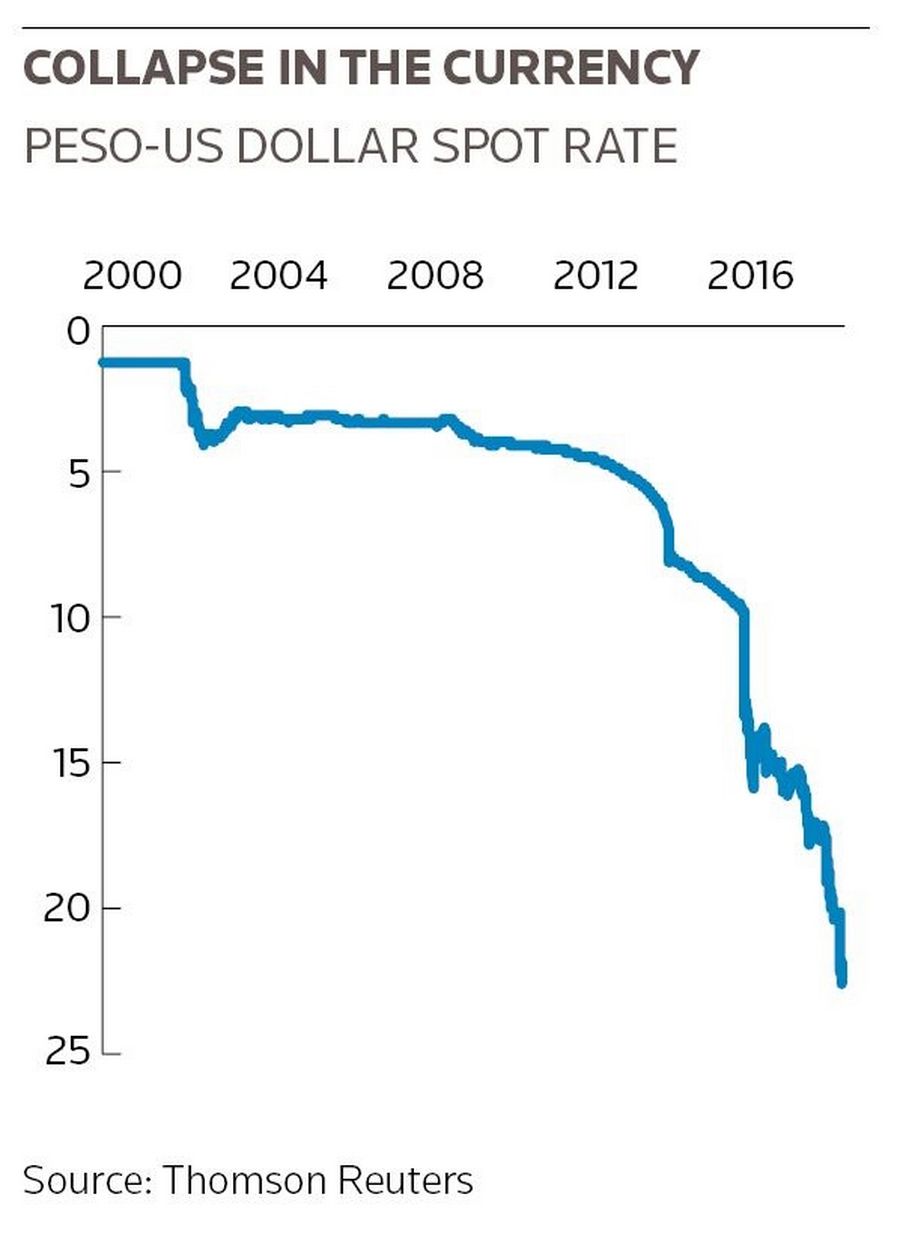

News of Argentina’s appeal to the IMF on Tuesday helped calm markets, sparking a brief rally in the peso, which earlier in the day had touched a record low of 23.1 to the dollar. That is just over half the level it was trading at after President Mauricio Macri removed currency controls at the end of 2015.

Attempts over previous days to stem the rout had largely failed. The BCRA raised rates three times – by a total 1,275bp – in just a week, sending policy rates to 40%, the highest in the world. The central bank also spent over US$5bn of its foreign currency reserves supporting the peso.

HELP NEEDED

Macri said external help was necessary because the government’s gradualist reforms, introduced since he took power just over two years ago, required markets to keep funding a large deficit.

The sovereign needs to raise about US$20bn a year from external markets over the next four years.

“During our first two years, we’ve benefited from a very favourable global backdrop, but today that is changing,” Macri said in a televised speech. “The problem we have is that we are among the countries most dependent on external financing, a product of the enormous public spending we inherited.”

But the decision to call in the IMF is political dynamite, coming less than 20 years after the country’s last international bailout. That forced deep cuts to government spending that many believe led to the emergency economic measures known as the “corralito” in 2001 and a default shortly after. With elections next year, there are risks that the gambit could backfire.

Still, many believe Macri had no other option.

“Their only real options were to hike even more, to impose capital controls, or seek help from the IMF,” said Dirk Willer, head of emerging market strategy at Citigroup. “Given that Macri’s administration so far has been all about dismantling capital controls, the IMF was the only real option.”

DEAL WITH CREDITORS

The appeal also comes just two years after Macri’s government lifted a pari passu injunction preventing payments on the debt the country defaulted on during the 2001 and 2002 crisis.

Then came the country’s dramatic return to capital markets a few weeks later. It sold US$16.5bn of bonds in what at the time was the largest-ever bond deal from emerging markets.

That return opened the door to a flood of capital into the country, with municipal government, utility companies and corporates keen to load up on financing after years in the financial wilderness.

But easy financing conditions have come to a decisive end.

Telecom Argentina and Petroquimica Comodora Rivadavia have both postponed planned bond deals in recent days, citing uncertain market conditions. Crop specialist Bioceres also pulled the plug on its New York IPO in February, while potential listings from Molino Canuelas and Gennaia are uncertain.

“IMF talks help the tone … but investor anxiety around the situation remains,” said one DCM syndicate manager. “There is a lot of financing to be done. There are lots of issuers that have financing needs.”

IMPACT ON GROWTH

According to Guarino, access to external capital is key.

“The local market doesn’t have the capacity to absorb the funding needs of the government, provinces and corporates,” he said. “And a lack of access to credit, especially for corporates, could lead to the cancellation of investments and eventually to lower economic growth.”

Others are more sanguine about the situation, and believe markets should reopen before too long.

“Investors do not believe there’s been a change in fundamentals or that the thesis for investing in Argentina has changed,” said Sebastian Loketek, head of investment banking for Argentina at Bank of America Merrill Lynch, who added that “dedicated players are generally not selling”.

“There needs to be a catalyst to change the current sentiment,” he said. “Nothing tells me that the market is going to be closed for too long but investors are definitely going to be more selective and very focused on valuations.”

But with emerging markets in general feeling the impact of the rising dollar, the future of Argentinian issuers may be completely out of their hands. A further three rate hikes are expected from the Fed this year, which could make matters worse.

“Some have labelled the situation a sudden stop, and there are certainly aspects of that,” said Willer.

“It’s not surprising that this is happening during a period when the dollar has been strengthening. You can’t have higher US rates and a stronger dollar and expect emerging markets to do fine – and you especially can’t expect emerging market countries that need a lot of financing to be fine.”

Others think the problem is isolated, and point out that wider emerging markets are fundamentally sound.

“Markets have naturally focused on weaker credits,” said Jan Dehn, head of research at Ashmore, who added that the reaction in markets was “tediously predictable”.

“Emerging markets in general are solid,” he said.