Europe’s covered bond market passed an important test at the end of August when a glut of issuance proved there was life after the European Central Bank’s purchase programme. However, activity could slump again as fears over sovereign risk re-surface. David Rothnie reports.

The European Central Bank launched its covered bond purchase progamme in June 2009. Its purchase of covered bonds helped to stabilise prices and boosted issuance to a record €105bn in the first half of the year. The programme, which also helped the covered bond market weather the sovereign debt storm, came to an end in June, raising concerns about the market’s sustainability.

Despite the removal of the safety net, the market has rebounded sharply. Covered bond issuance enjoyed a late summer surge, thanks to a combination of factors, while the results of the bank stress tests eased investors’ worst fears over the solvency of the Eurozone banking sector. Meanwhile, the introduction of austerity programmes by European governments mitigated concerns over sovereign risk, enticing issuers to exploit low borrowing costs to offer investors some spread pick-up over sovereign debt.

However, the glut of issuance also shows that a flight to quality remains. Investors clearly remain wary of covered bonds from peripheral issuers, while the sovereign crisis is only one bad news story away from spooking markets.

“The big change is that pricing in covered bonds has move from bank credit to sovereign risk,” said Heiko Langer, a senior credit analyst for covered bonds at BNP Paribas. “It is not so much who the issuer is but where they are from.”

This approach is dictated by the risk approach of investors, who pull or extend credit on a country-by-country basis. Langer added: “There has been little difference between the covered, the senior and the sovereign with all asset classes stigmatised at the same level, so the added protection afforded by covered bonds is less relevant.”

While the banking stress tests were criticised for their leniency and did little to restore faith in the Eurozone’s weakest banks, they did nothing to harm stronger banks and stabilised flagging consumer sentiment.

No rest for the covered

“The big difference from a year ago was that we had quite a lot of issuance in the first half of this year because of the ECB purchase programme and there was a sense that issuers were front-loading,” said Langer.

This does not appear to be the case. The seasonal pick-up in covered bond issuance began with €8.2bn of deals announced in the last week of August, led by ING which issued €2bn of five-year notes and DNB Nor raising €1.5bn of seven year debt.

The pace continued into September, with the Royal Bank of Scotland launching a €1.5bn five-year UK covered bond at mid-swaps plus 127bp with a coupon of 3.000% on September 1. On the same day, French CM-CIC Covered Bonds (CMCICB) used a €1.00bn French common law covered bond. The deal, which carries a coupon of 3.125%, was priced at mid-swaps plus 73bp.

The revival of the market was underscored by the return of Spanish banks, which have been shut out of the wholesale financing markets since May. In the first four days of September, Spanish banks issued US$4bn of paper, of which US$2.5bn was in covered bonds. Spanish commercial bank Banco Sabadell issued a two-year €1.000bn Cedulas Hipotecarias at mid-swaps plus 210bp, while La Caixa issued €1bn of three-year covered bonds. In the non-benchmark space, Spanish commercial bank Banco Popular (POPSM) issued a €700m three-year Cedulas Hipotecarias at mid-swaps plus 215bp, while Italian Banca Carige issued a €500m deal at mid-swaps plus 105bp on September 1.

On September 5, Santander exploited the improving sentiment by tapping the market for €1bn of three-year unsecured bonds at 145 bps over the benchmark swap rate, with strong international demand.

The rebound in issuance came after a strong first-half, albeit one undermined by a closure of the covered bond markets in May following contagion fears after the Greek sovereign debt crisis. “In peripheral countries such as Spain, spreads on government and covered bonds widened in May,” said Torsten Elling, head of covered bond syndicate at Barclays Capital. “Covered bonds traded close - or flat to - senior debt, as investors demanded more spread relative to sovereigns.”

After an average of €18bn of monthly issuance between January and April and a total deal value of €73.7bn, there was only one deal in May – a €1bn four-year trade launched a mid-swaps plus 40bp from France’s CDEE. Issuance rebounded to €20bn in June, before falling back to €3bn in July. Analysts at Barclays Capital predict €18bn of issuance in September, and around €15bn in October, but a high level of redemptions will reduce net issuance for the two months to around €8.3bn.

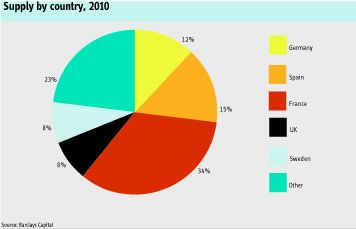

Langer estimated issuance for 2010 will be €150bn, and as of September 12 there were €115bn worth of covered bonds issues. Of these, roughly 81% were issued prior to the cessation of the ECB purchase plan, according to Barclays Capital. Of the total, 26 deals were originated in France, 12 each in Germany and Spain, eight in the UK and four in Italy.

Dark clouds on the horizon?

The rush by banks to access cheap sources of funding could be short-lived. Barclays projected covered bond volumes “could become subject to a pronounced downward revision should concerns regarding the re-financing capabilities of non-core European sovereigns re-emerge.”

These concerns, which lurk the back of investors’ minds, flare up whenever there is negative news flow. There remains considerable spread differentiation between covered bonds and senior financial debt, depending on the issuer’s country of origin. Even after the EU and International Monetary Fund worked out a sovereign rescue plan in May, investors are still demanding a high premium for buying Greek debt. As of the beginning of September, the yield was 11.28% on 10-year Greek bonds, compared with 2.34% on similar German bonds.

At the end of August, yield spread was the widest it has been since the peak in May, just before European leaders agreed on the bailout. Stress tests have not been a panacea. “The covered market remains partially open but full market access will not return until trust in the weaker banks is restored,” Langer said.

A broad re- opening of non-core covered bond markets with new issuance from lower rated banks has not materialised. Langer wrote in a recent report: “While we have seen with the recent €2bn 3y Cedulas issue from BBVA that a high new issue premium can attract significant investor demand, weaker issuers may find it difficult to generate similar demand, even at higher spread levels, as uncertainties about a swift recovery of such banks remain flat to senior bank debt, given the dual recourse of the covered bondholders.”

Covered bonds have mirrored government bonds in peripheral countries, so the return of sovereign risk fears would hit the covered bond market. However, Barclays Capital notes a recent “decoupling” between the two asset classes that will make covered bonds look cheap on a relative basis. It added: “ A rally of government bond spreads should, as has historically be the case, sooner or later be reflected in a parallel move of covered bonds as investors, in an attempt to secure the usually higher-yield, start-shifting funds into the covered bond markets. Yet, the recent (and ongoing) swap-spread decoupling between covered and government bonds must not necessarily be the starting point for a covered bond rally. We believe that for the time being macroeconomic concerns will continue to cast their shadow on the markets.“

Covered bonds provide precisely the sort of guarantee that investors are seeking and while yields are low, they are more attractive than treasuries.

Tim Skeet, head of covered bonds at Bank of America Merrill Lynch, observed further momentum for the asset class coming from the US, whose experience of the covered bond market is limited to quasi-government backed issuance from Canadian banks. “US real money investors want quality paper that will provide a pick-up to Treasuries while at the same time diversifying away from corporate high grade,” he said. “European banks are actively looking at the 144a market as an alternative to the traditional euro sector.” Skeet predicted around ten covered bond transactions in the US between now and the end of the year.

One long-term attraction of covered bonds is their stability. That has been important for both borrowers and issuers, as the European sovereign debt crisis closed down other funding avenues for financial institutions. “Since the financial crisis, funding diversification has been a crucial issue for banks, “said Skeet. “In uncertain times, investors want to know they will get their principal back. That is a fundamental attraction of covered bonds.”

The importance of covered bonds as a funding mechanism is enhanced by more flexible and more frequent issuance. “Banks will no longer feel they have to issue benchmark size deals,” said Skeet. “Smaller deal sizes will become more common as banks seek to diversify funding and issue covered on an opportunistic basis.”

“Covered bonds will become even more important as a funding source in the future as there is a potential lowering of public support for banks,” added Langer. “If banks are allowed to fail in future, covered bonds will become more attractive for investors.”