Seize the moment: The past 12 months were hazardous for international banks. Market volatility and economic uncertainty ran into transformational changes brought about by sweeping regulatory change. One bank took some very early and courageous decisions, moved aggressively to boost capital and liquidity, and cut risk-weighted assets at the same time as it began executing on the first stages of a bold shift in its corporate and investment bank strategy. BNP Paribas is IFR’s Bank of the Year.

It is no easy matter for a bank to deleverage, strengthen capital, secure access to alternative sources of funding and drive strategic change. It is even harder to do so without losing sight of the underlying business. But that is what BNP Paribas group chief executive Jean-Laurent Bonnafe and his executive board achieved in 2012.

That the reasons for the accelerated progress of the bank’s makeover were steeped in the trauma of the second half of 2011 makes those achievements all the more impressive.

“We’re back to business and ready for growth despite the uncertainties in the economy and around regulation,” Bonnafe said. “The adaptation process is behind us and we are out of the blocks ahead of most of our competitors.”

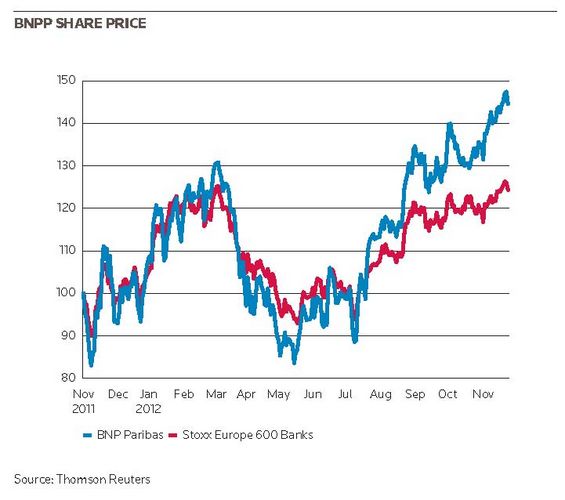

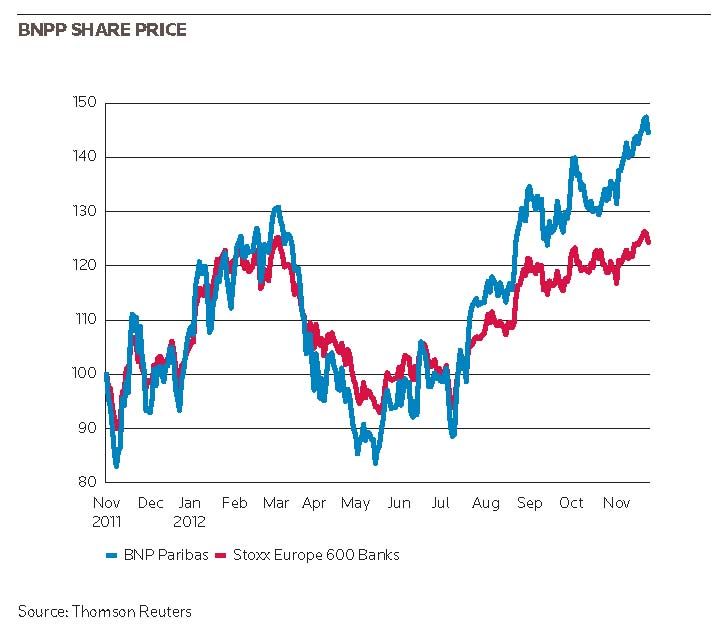

The change in the external perception of the bank has been nothing short of remarkable. From the dark mutterings of 2011, after US money market funds cut dollar exposure to BNPP and other European banks, almost all analysts now rate BNPP shares “buy” or “hold” – a best-in-class performance. The bank’s share price was up 50% between January and early December 2012.

Among other things, the withdrawal of US dollar money-market funding forced management to execute changes that were planned for a much longer period of time. “We were under too much pressure from stakeholders and the market to wait, so we decided to do something which would differentiate us from our competitors: do it quickly, and I mean very quickly,” said Alain Papiasse, deputy group COO and head of the corporate and investment bank.

“When you take a long time to adjust, it’s easier for people because it’s less painful. But by the same token it can upset your business for a long time. Brutal decisions are more painful, but the impact is short-lived.”

The transformation was impressive indeed: the bank cut dollar funding by US$65bn by April 2012, eight months ahead of schedule; exceeded the year-end capital target, hitting a 9.5% fully-loaded Basel III core Tier 1 ratio by September 30, and reduced risk-weighted assets by €45bn by September, when the target had been year-end. And because the assets that had to come off the books were good quality, the bank was in aggregate able to sell them more or less at par. The net cost of asset sales was just €250m against estimates of €800m.

Management was keen to deleverage without affecting the client franchise or being accused of stop-go banking. This was all achieved. In fact, the only business the bank exited was reserve-based lending in the US, which had relatively limited synergy with the rest of the group. Beyond that, it sold a 28.7% stake in shopping centre operator Klepierre for €1.52bn.

Where it exited customer relationships, these were customers who did not fit the new profile – predominantly clients to whom the bank was lending but not receiving the business it wanted in return, or who were no longer in what Papiasse calls the “magic circle”.

The results of the adaptation plan were delivered at the same time as nine-month earnings showing net income attributable to equity holders of more than €6bn. CIB’s third-quarter revenues were stunning, up 33% to €2.38bn. Advisory and capital markets revenues rose 41.5% to €1.58bn; fixed income rose 38% to €1.1bn, while equities and advisory jumped 51% to €444m. Corporate banking, which bore the brunt of the RWA reduction, reported revenues in line with deleveraging at €805m, down 16.3% (net of loan sale effects).

With a cost-income ratio in CIB of 61.5%, towards the bottom of the scale, and a lower risk profile than most of its competitors, the annualised pre-tax return on equity in CIB is above 20%.

“Thanks to our highly differentiated CIB model built on long-term relationships with customers, we consistently deliver returns above our cost of equity and we control our costs, resulting in a lower expense ratio,” Papiasse said.

Total transformation

BNPP is not a monoline investment bank. As a universal institution, the bank offers corporate finance, M&A, equity and debt underwriting, and the full suite of trading businesses. But Papiasse also has at his disposal the benefits of a global corporate bank, housing transaction banking and securities services as well as a world-leading structured lending business that encompasses commodity and energy finance, asset finance (real estate, shipping and aerospace, export finance), project and media finance, leveraged and acquisition finance, syndicated lending and loan trading.

The big play in 2012 was leveraging the corporate bank and the investment bank to become a fully integrated CIB. Papiasse strengthened and simplified internal lines of communication, and reorganised the businesses in order to drive an aggressive monetisation effort.

“The magic ingredient is getting flow business, because that gives you insight on a daily basis into what your customers are doing in areas like FX or vanilla derivatives,” Papiasse said. “When you provide clients with the corporate banking capabilities they need and you follow them around the world, they will give you some of their investment banking business as long as you have the right platform – even if you’re not number one in a given category.”

Building deposits

The French lender plans to finance its entire corporate loan book through deposits in the medium term, and has launched a major campaign to win over new corporate depositors – especially in the Middle East, Africa and Latin America, where the firm has traditionally lagged behind rivals. Papiasse believes the investment bank’s presence in 45 countries will make its proposition to corporate clients more appealing. At group level, it has a presence in 80 countries.

As well as rapidly building up its corporate deposit base, BNPP won dozens of cash management mandates in 2012 from the likes of Schlumberger, Thales, and UCB in India and China. BNPP is now number one in the eurozone for cash management – and number five worldwide.

If the first plank in BNPP’s CIB transformation was a more integrated approach to doing business, the second was embedding an originate-to-distribute model into its financing businesses, leveraging its strong origination capacity in structured lending into the institutional distribution engine of its fixed-income division.

“In years to come, the economy will not be financed through bank balance sheets as it used to be,” said Bonnafe. “In Europe, we’re going from 80% of bank balance sheet financing down to 50%. You have to acknowledge this is going to be the story, so you have to invest in markets businesses and use your origination ability to move clients, including mid-cap corporates, to the capital markets. That’s one of the key drivers of OTD that we’ve implemented in CIB.”

Dominique Remy, former global head of structured financing and now head of corporate banking Europe, worked with global head of fixed income Frederic Janbon to attempt to securitise structured bank risk for consumption by institutional investors.

“We are uniquely positioned within CIB as we have one of the best specialised finance platforms and a sizeable fixed-income distribution network,” Janbon said.

To facilitate the transition, the bank co-located loan and bond syndicate teams while undertaking an intensive process of customer education, as well as an education of its own fixed-income sales force. Management created sub units within fixed income by asset class, so there are now dedicated structuring teams – for example, in aircraft and project finance. “The co-operation with fixed income is great,” Remy said. “There is still a lot to do but what we did in 2012 was extremely promising.”

While the push is towards market-based solutions, the intent is not to distribute everything. “We want to be reasonable,” said Remy. “Our policy is to keep some risk on the balance sheet. If you distribute everything, you become a broker. That’s not what we want to become.”

Stand-out examples of the OTD initiative include the innovative €472m private placement of mortgage bonds to refinance the Lumiere building in Paris on behalf of real estate developer Tishman Speyer. The notes were secured by a first-ranking mortgage and were sold exclusively to insurance companies. The €175m floating-rate term loan facility for Belgian cable TV, internet and telecoms service provider Telenet was similarly sold entirely to investors.

This initiative has a strong US angle. If, as Bonnafe believes, banks are disintermediated by the capital markets, then BNPP will need deeper and broader access to the US investor base that drives so much flow. In this regard, the US platform is key to the group’s global business model. At the end of 2012, BNPP was in the final stages of signing off on its three-year US growth strategy, to be driven by Americas CEO Jean-Yves Fillion.

“We intend to add more strength to our DCM expertise by investing in distribution capabilities as part of our strategy to link issuers to investors,” Fillion said. “The challenge is to continue to protect and gain market share in the current regulatory and competitive environment, in which there will be fewer universal banks because it will be more expensive to be one.”

As well as the US, Asia is a BNPP growth play. Eric Raynaud, Asia-Pacific CEO, points to 14,000 group employees in the region as a sign of commitment to the region. “BNP Paribas is firmly established in Asia-Pacific and we have stuck with our clients throughout the market cycles. In addition to a strong pipeline of deals, we experienced growth in assets under management in our wealth management unit and in corporate deposits, which is important in today’s climate,” Raynaud said.

“Asia-Pacific is a strategic area; hence we continued to invest in our platforms over 2012 as we expect further growth in the future. We plan to expand our CIB and investment solutions activities in Asia-Pacific over the coming years.”

In terms of deals that demonstrated expertise across markets and businesses, BNPP was mandated by Trans Retail (CT Group) in Indonesia to be lead bank in the acquisition of Carrefour Indonesia. Elsewhere, the bank financed the purchase of a Boeing aircraft for Air China, financed through a short-term bridge loan and refinanced through a US Exim bond (an area in which BNPP ranks number one world-wide). A similar deal was concluded for Lion Air.

In the Dim Sim market, BNPP brought an array of first time issuers, including Banco Bradesco, Bank of East Asia, BMW, Orix Corp, Volvo, Taiwan’s Yieh Phui Enterprise and Korea’s Cheil Jedang Corp and Korea Finance Corp.

Beyond integrated cross-selling and OTD, the third plank in BNPP’s transition was reorganising management along regional rather than global lines. “Global banks used to run their operations on a global level,” said Bonnafe. “For a number of reasons, the way we will have to move in years to come will be towards achieving a balance between global and local. The added value of a global bank will be an ability to be both efficient globally and locally.”

The art of the deal

BNPP’s success was not all about divisional cross-selling. In DCM and syndicated loans, the bank maintained a leading presence, and it worked on some stand-out deals in corporate finance and ECM. The bank is ranked number one in EMEA loans, as well as euro DCM.

In terms of stand-out business, BNPP was one of four co-ordinators in the €9bn financing package to support the demerger of Snam from the Eni Group. The transformational and smoothly executed €11bn financing package was subsequently reduced to €9bn following two pre-close bonds of €1bn each.

BNPP was also one of four active co-ordinators on the complex €8bn Schaeffler transaction. Elsewhere, the bank successfully took European companies to the US market, US companies to the European market, did deals in frontier markets, sold a host of mid-cap deals and continued to syndicate global deals for global companies.

The powerhouse euro DCM franchise continued to beat all comers in 2012. BNPP was the number one underwriter of euro bonds, with a tally of 284 issues to December 7. Beyond euros, the bank maintained scale in Swiss francs, sterling, emerging EMEA, Euroyen and Dim Sum bonds. And it executed deals across the spectrum of hybrids, liability management, private placements, retail and Schuldscheine for a wide variety of issuer types, including from peripheral Europe.

If success is measured by opening channels to market and creating solutions for sophisticated borrowers, BNPP ticked all the right boxes.

Just some of its noteworthy achievements include deals for AB InBev (€2.25bn refi and pre-financing of US$14bn takeover of Grupo Modelo); GDF Suez (largest euro corporate deal of the year at €3bn; second-lowest coupon ever at three years, lowest ever at six and 10 years); Philip Morris (dual-tranche €1.35bn lowest ever coupon for a corporate in the seven and 12-year maturities); Snam (€4.5bn four-line refi and DCM debut) and Glencore (dual-tranche following Xstrata and Viterra M&A updates; sub investment-grade rating and M&A coupon step-ups on €1.25bn and £300m dual-tranche).

In the US, BNPP is a top three underwriter of US agency paper and was an active bookrunner on benchmarks for prime US corporates, including Time Warner, IBM and Coca-Cola. As well as bringing US investment-grade corporates, BNPP closed deals in the Yankee, high-yield and US private placement markets.

Creating solutions

The DCM team worked hand-in-hand with corporate finance to deliver tailor-made solutions in credit-intensive situations such as corporate hybrids. It brought hybrids for RWE (the first dollar hybrid from a European corporate), BG Group (first ever triple tranche hybrid), SSE (first ever sub-6% dollar hybrid coupon) and ArcelorMittal. The bank also played a role on UBS’s US$2bn Tier 2 offering, the first Basel III-compliant transaction with contractual permanent loss-absorption from a European bank and the largest Asian-targeted dollar subordinated deal of 2012.

“The advisory and strategic dialogue we have with clients irrigates a lot of our business lines and activities,” said Thierry Varene, global head of corporate finance.

In M&A, BNPP was adviser to Carrefour on the sale of its Colombian subsidiary to Chile’s Cencosud for US$2.5bn, and to CT Corp in the acquisition of Carrefour’s Indonesian unit for US$673m. The bank also advised Polish miner KGMH on its US$2.9bn acquisition of Canada’s Quadra FNX Mining, and BAA on its £807m sale of Edinburgh Airport.

Elsewhere, the bank advised Tauron Polska Energia on its acquisition of Gornoslaski Zakład Elektroenergetyczny, and renewables company Renovalia Energy on its joint venture with First Reserve, the energy industry private equity and infrastructure investor, to own and operate wind projects in Europe and North America. “This demonstrates that we are not just a French bank,” Varene said. “We’re a truly international bank with international advisory capabilities.”

In ECM, BNPP was at the forefront of equity-linked, with 11* deals across a broad geographical spread. Among the lead-left roles were its first ever sole-managed US convertible for Meritor (US$250m) and a €420m convert for South African furniture company Steinhoff that stemmed from BNPP’s acquisition late last year of 60% of the broking business of South African equity derivatives broker Cadiz Securities. (The bank also obtained a full South African banking licence in 2012. Its commitment was rewarded with the mandate for the sovereign’s debut sukuk.)

Adapt to grow

If BNPP was an early adopter of deleveraging, the equity derivatives group was a true pioneer. The head of equities and commodity derivatives, Yann Gerardin, launched his own adaptation plan in 2009, transforming the business model to take on less risk, shrinking RWAs, resetting the customer profile and shifting the business focus away from products such as complex and long-dated options.

As a result, BNPP’s world-class equity derivatives business is now profitable after costs, cost of capital and bonuses. “Our market share has grown significantly this year,” said Gerardin. “And we’ve developed our franchise by adding elements that were missing.” One of those elements was the full internationalisation of the US domestic prime brokerage platform that BNPP acquired from Bank of America in 2008.

The bank also built from scratch an internet-based tool for structured products called SMART derivatives, which launched in mid-2012 to make the bank a go-to house for flow-oriented products. The results have been extremely powerful. The tool is now live in 16 countries, 80 clients are connected to it and have used its real-time pricing capabilities on more than 11,000 trades per month. Clients are able to price standardised products and can request a quote on more advanced products.

BNPP also continued to work with leading houses, such as JP Morgan and Goldman Sachs, as a hedge provider for their retail structured products. Late in 2012, Macquarie selected BNPP to take over its predominantly listed flow structured products business in Europe and handle all client-servicing related to its products. Amundi, the ninth-largest asset management company in the world, selected BNP Paribas to be its main market-maker and sole swap provider for its equity and commodity ETF business.

The team structured a number of popular products this year, including the Duo Garantie 2000 certificate, created on the back of reverse enquiry from clients who wanted to capture market opportunities while retaining high capital guarantee levels. In essence, 50% of invested capital earns a fixed rate of 5%, while the other half is partially indexed to eight European stocks, equally weighted in the portfolio. A range of other products was also launched to a positive reception.

In commodity derivatives, to increase the level of cross-selling, the bank created a joint venture with the energy and commodities financing group. “The collaboration we have between commodity finance and commodity derivatives may once have been a nice-to-have but now it’s a must-have,” Gerardin said. The bank is now working on a similar cross-sell joint venture with the project finance division.

Making a difference

To do all this in a period beset by market volatility, economic uncertainty and dramatic regulatory change is miraculous. To do it while moving aggressively and courageously to boost capital and liquidity, and kicking off a bold shift in its corporate and investment bank strategy is even more impressive.

What a difference a year makes.

* Correction. This number was originally given incorrectly as 21.