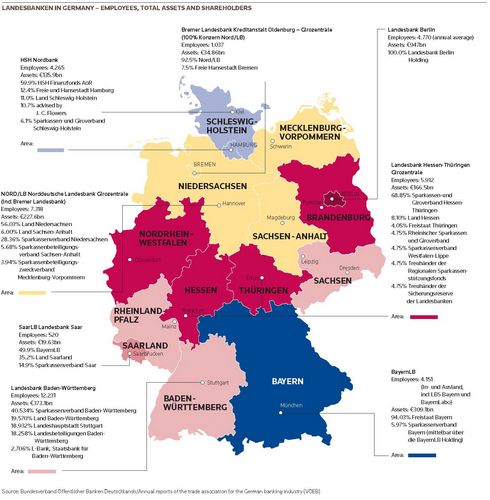

Landesbanken have been through a process of balance sheet restructuring and strategic review. Stability now seems to have returned to many of the regionally-controlled banks, but questions remain over their future role and purpose.

To view the digital version of this report, please click here.

When WestLB was formally wound up in July 2012, following a series of trading scandals and losses, the future for Landesbanken appeared gloomy, with consolidation seemingly the most likely destiny for the remaining eight banks. A year later the outlook appears to have improved, and talk is now focused on financial security and restructuring rather than wholesale change.

“Given the large amount of state support that they received it was natural following the financial crisis that the structure of the Landesbanken should be called into question,” said Tim Brandi, a partner at Hogan Lovells International in Frankfurt, which worked on the WestLB process.

“However, with the banks being state-owned there is a lot of political capital at stake, and as the financial situation improves talk of consolidation has faded.”

In a sign of the evolving regulatory landscape in Europe, the demise of WestLB was instigated not in Berlin, but Brussels, where the European Commission ordered a change of ownership in response to the billions of euros in state aid and guarantees the lender had received.

The Commission had also demanded restructuring at Landesbank Baden-Wuerttemberg, which incurred substantial losses on exposures to Southern European governments and state-related companies (particularly in Greece) and BayernLB, for state aid it received in the financial crisis.

“LBBW was traditionally the strongest Landesbank because it had a strong retail franchise but then became overly ambitious with its capital markets business,” said Michael Dawson-Kropf, an analyst at Fitch in Frankfurt. “Now they are in restructuring mode.”

In February LBBW said it had largely completed its restructuring, cutting risky assets and raising its Tier 1 capital ratio to 15.3%, as 2012 profit rose to €399m, compared with €86m the previous year. The lender received €5bn in capital and €12.7bn in guarantees at the height of the financial crisis.

BayernLB, meanwhile, is paying for ill-fated purchases in Europe; notably the €1.625bn acquisition of a 50.01% share in Austria’s Hypo Group Alpe Adria in 2007, which, following more than US$4bn of losses in the US subprime crisis, was sold back to the Austrian government for one euro.

During the crisis, the State of Bavaria provided the bank with a €7bn equity injection and a €3bn silent participation, increasing its indirect shareholding from 50% to 94% and diluting the Association of Bavarian Savings Banks’ stake from 50% to 6%.

Another bank to have encountered significant problems is HSH Nordbank, the world’s largest shipping bank, which estimated earlier this year that around half of its €30bn shipping portfolio is struggling to repay loans.

HSH Nordbank received a €30bn state-funded bailout in 2011 and in March agreed with its owners, the states of Hamburg and Schleswig-Holstein, a hike in its guarantees to €10bn.

“HSH Nordbank is on its way to stabilising but they made a big mistake when they paid back loans too early, when they should have kept the public money invested in the bank,” said Stephan Rabe, a director at the Bundesverband Offentlicher Banken Deutschlands (VOEB), the trade association for the German banking industry.

Roots of the problems

While the immediate problems of the Landesbanken were caused by the financial crisis, the roots of their difficulties were established in 2005, when the banks lost their explicit state guarantees. As the positive effects of state support lingered in the years before 2008, the banks went on a borrowing spree, gorging on cheap money and spending on risky investments such as US mortgage-backed securities.

“After the abolition of state guarantees in 2005 the banks retained good ratings and took up liquidity which they used to expand their global footprint,” Rabe said. “It was unfortunate timing because soon after we had the US housing market collapse and financial crisis, which hurt all the Landesbanken and particularly WestLB.”

Another bank to have been hit, and to subsequently restructure was Landesbank Berlin, which in December said it would sell its fund business to DekaBank, the asset manager for Germany’s savings banks, and concentrate on establishing itself as retail and commercial real estate specialist.

“In the next few years, Berlin will face numerous structural issues. These will include population growth, residential space becoming scarcer and the development of companies,” said CEO Johannes Evers in March. “For this reason it needs a saving bank to help the city. We look forward to this task.”

Prudence pays off

The Landesbank to emerge from the financial crisis least scathed was Helaba Landesbank Hessen-Thueringen, based in Frankfurt. Helaba refrained from taking big bets on structured credit products before the financial crisis and its prudence paid off with relatively meagre loan provisions and write-offs. Among its rewards was the valuable legacy assets from the WestLB restructuring.

“Out of the circa €140bn of assets that were transferred in 2012 around €100bn went to the Erste Abwicklungsanstalt [winding up agency] and €40bn were acquired by Helaba,” Brandi said.

One of the keys to Helaba’s success, analysts said, had been its role as a central bank for the savings banks in Hesse, Thuringia, North Rhine-Westphalia and Brandenburg, accounting for about 40% of Germany’s savings institutions.

Saving banks also have a significant shareholding in Helaba. As of July 5 2012, the largest shareholders were the savings banks and Giro Association Hesse-Thuringia, which together held a 68.85% stake. The Federal State of Hesse held a stake of just 8.1%, a much smaller level of local authority involvement than at other Landesbanken.

“People are always saying we don’t need Landesbanken but those people ignore the fact that they provide around a quarter of the credit to German enterprises”

With Helaba as the outstanding success story of recent years, and given that Germany has more credit institutions than any other European country, there has been a debate over whether there is still a need for state-ownership of banks, or state-owned banks at all.

Still needed

The German banking sector is characterised by numerous institutions, extreme competition, low margins and low profitability. However, some observers said those that doubt that Landesbanken were necessary underestimate the importance of their role in lending to Germany’s small and medium-sized enterprises.

“People are always saying we don’t need Landesbanken but those people ignore the fact that they provide around a quarter of the credit to German enterprises,” VOEB’s Rabe said. “So saying the sector is on the verge of being abolished is ridiculous.”

In fact Landesbanken’s share of corporate lending has been falling in the recent period, as several of the banks have reduced risk-weighted assets, but it remains above 22%, according to figures from Deutsche Bank, despite competition from larger savings banks, big commercial banks and foreign operators.

This sector has been among the most active bond issuers in German, at the peak with almost €500bn of debt instruments outstanding. After aggressive deleveraging, Landesbanken bond commitments are now down to about €340bn, but state government investors show few signs of reducing their commitments. In fact, quite the opposite.

As a proportion of the total, state investors as at June 2012 held some 40% of the outstanding bonds of the Landesbanken, compared with as little as 22% in previous years. Meanwhile non-public sector banks have cut their share. That suggests more, not less state support, in the short term at least.

“The process of deleveraging is continuing and following the financial crisis states have been required to increase their support,” said Harm Semder, director European Financial Services – Financial Institutions at Standard & Poor’s in Frankfurt.

“The most probable outcome is that there will be no general rule, and each bank will evolve its individual role as it develops its business model.”