When two days after Lehman Brothers filed for bankruptcy Barclays announced that it was buying the collapsed bank’s prized US investment banking and capital markets business for just US$250m, the deal was widely seen as something of a coup.

Bob Diamond, who had spent a decade transforming Barclays’ sleepy investment bank BZW into a dominant European bond house, had long held ambitions to break into Wall Street. Lehman’s collapse was his chance. “This is a once in a lifetime opportunity for Barclays,” he said at the time of the deal.

Barclays had been circling around Lehman for months ahead of its collapse – an internal team had been working on what was known as Project Long Island since March. Lehman, with its strength in the US, especially in equities and M&A, seemed like a perfect fit for the European, bond-focused Barclays.

Only days before its collapse, Diamond had been preparing to bid up to US$4bn for the whole of Lehman – and much of the mess that lay within. UK authorities baulked at the deal, helping Diamond dodge a bullet. In the end he got the businesses he really wanted, without the mess, for a fraction of the price.

“All the conversations were initially about buying the entire Lehman business,” Diamond told IFR. “It fit us perfectly. Only after bankruptcy did it become clear to us that it might be possible to purchase part of it. If I’m perfectly frank, it was even more perfect for Barclays.”

On paper, the two promised to be a dominant force in the US - the source of almost half of all underwriting and advisory fees globally then and now. Barclays boasted that the combined entity would be a top three player in the US.

MIXED RESULTS

But, ten years on, the results are mixed. While Barclays is the top European investment bank in the US – just ahead of Credit Suisse – it now only ranks seventh, according to Thomson Reuters data, well short of the top-three it had targeted. It has slowly dropped down the rankings ever since the deal.

Globally, the bank also earns less in revenues from trading and investment banking activities than the combined Barclays and Lehman US businesses did the year before the deal.

That is in part because trading revenues have fallen across the industry, but mostly due to half a dozen strategy overhauls in the last few years that saw the bank pull back in many areas globally.

Still, initially at least, the deal was a game changer for the UK bank. Overnight, it gained 10,000 Lehman employees (around 4,000 were cut soon after the deal) and lucrative new relationships with huge US clients that previously Barclays could only dream of.

“To acquire a franchise that deep, with an incredible advisory business … it was transformational,” said Diamond. “There were so many talented Lehman people that stayed with us. It was a really tough environment, but exciting for us to have such a platform. We couldn’t have done that organically.”

It also gave Diamond the ideal excuse to rebalance the business outside of the US away from bonds. He sensed an opportunity for Barclays to be a full-service investment bank across the globe. New teams were set up and big names hired, especially in European equity capital markets.

BIG MANDATES

With the US economy growing and deals returning, the New York office won some big mandates: it advised Kraft on its acquisition of Cadbury’s, MetLife on its purchase of American Life Insurance, and Hewlett-Packard on Autonomy. None would have even been thinkable for Barclays before Lehman.

Revenues from the US surged, and by 2012 were treble what Barclays earned out of the US before the acquisition. That created a nice counterbalance for the bank’s dwindling fortunes in Europe, where the eurozone crisis was ravaging dealmaking. The Lehman deal was paying off nicely.

But then the Libor scandal hit the bank, forcing the departure of Diamond, who by that stage had been elevated from head of Barclays’ investment bank to chief executive of the entire group. With Diamond’s exit, the investment bank lost its biggest champion.

Two things then happened to dent the momentum of Barclays in the US. Incoming CEO Antony Jenkins launched a crusade to change the culture of the bank. This grated with former Lehman staff, who had been given a relatively free hand to do deals under Diamond. A divide that already existed between London and New York grew wider.

Then new rules on leverage and ring-fencing led to a dramatic rethink about what Barclays’ investment bank should be doing – so-called Project Elektra.

“It was clear that my successor was not supportive of a global investment bank or of investing in the US business,” Diamond said.

Over just a few months, the bank’s US top brass took the hint. Leavers included Skip McGee, global head of investment banking; Larry Wieseneck, head of global finance; Paul Parker, head of M&A; Jeffrey Weiss, head of FIG advisory; Ros Stephenson, co-head of corporate finance; and Jerry Donini, head of equities.

SHRINK IN BUSINESS

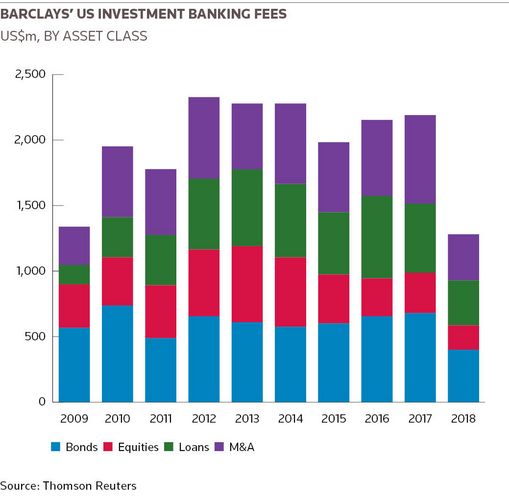

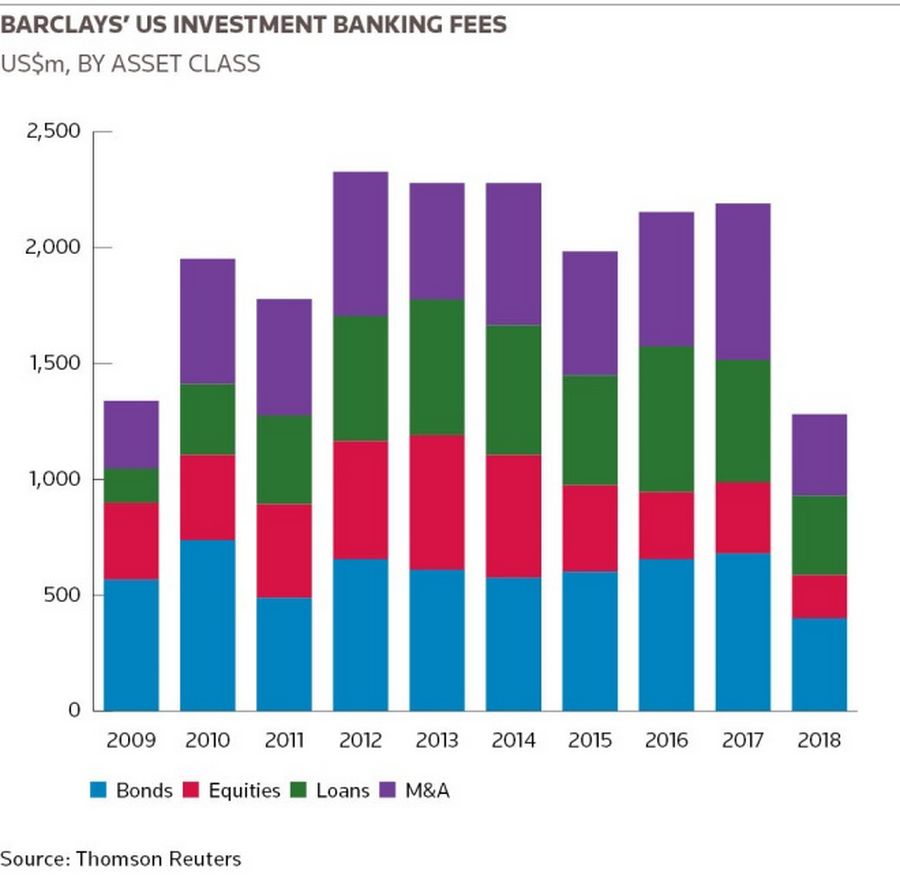

In an industry built on relationships, that hurt. Insiders say the franchise took a hit that it has struggled to recover from. Thomson Reuters data show that Barclays investment banking fee haul in the US peaked in 2012. While the overall pie has grown, it has seen US fees fall by about 6% since.

Jenkins was pushed out at the end of 2015, to be replaced by Jes Staley, a former JP Morgan investment banker. Under him, Barclays has sought to recharge its US operations. He has publicly said that the UK lender will seek to have a “bulge-bracket transatlantic investment bank”.

“In the years prior to Jes coming in there was certainly a loss of talent. But Jes has been very supportive of the US,” Diamond said.

The strategy appears to be bearing some fruit. In the US last year, the bank had its best year ever for M&A advisory fees, after winning mandates on some key deals such as the Mars acquisition of VCA and the buyout of Staples. This year, it ranks fifth in US equities.

Still, the top three it was aiming for in 2008 remains a long way off.

| US investment banking fees Bookrunners: year to date | |||

|---|---|---|---|

| Bank | Fees | (%) | |

| 1 | JP Morgan | US$3.12bn | 10.4 |

| 2 | Goldman Sachs | US$2.54bn | 8.5 |

| 3 | BAML | US$2.41bn | 8.0 |

| 4 | Morgan Stanley | US$2.11bn | 7.0 |

| 5 | Citigroup | US$1.77bn | 5.9 |

| 6 | Wells Fargo | US$1.41bn | 4.7 |

| 7 | Barclays | US$1.30bn | 4.3 |

| 8 | Credit Suisse | US$1.24bn | 4.2 |

| 9 | Deutsche Bank | US$930m | 3.1 |

| 10 | RBC | US$818m | 2.7 |

| Total | US$29.41bn | ||

| Source: Thomson Reuters |