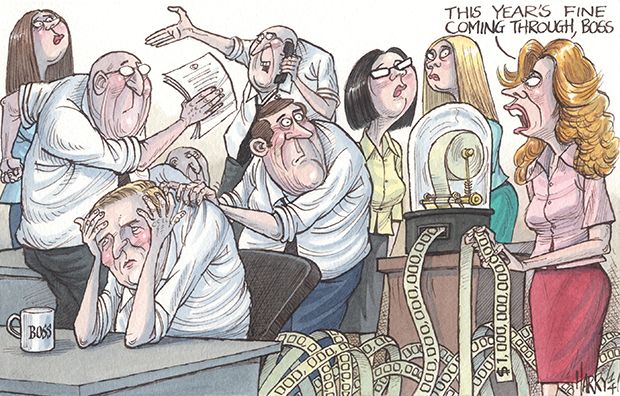

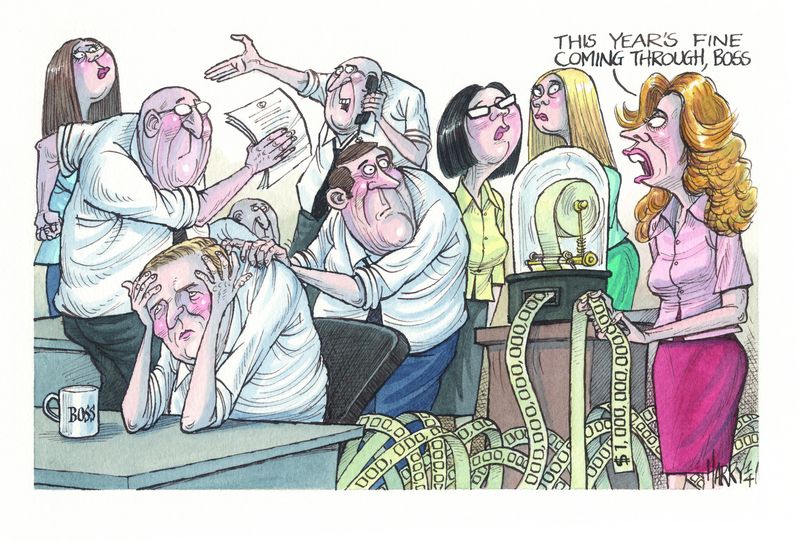

Fines for previous misdemeanours reached all-time highs in 2014 as regulators became more assertive in extracting large settlements that, while eye-popping, wouldn’t break the banks. But with the last of the big scandals reaching a close, banks are hoping the era of penalties may be behind them.

One record fine has barely earned its place in the history books before the next eye-popping settlement has supplanted it. Such has been the case of inflating penalties over the past two years. JP Morgan’s US$13bn fine for mortgage-linked misbehaviour held the record for just six months before a new record – a US$17bn penalty at Bank of America for similar wrongdoing – topped it.

Wrongdoing linked to an array of offences from mis-selling to market manipulation and sanction breaches, and a new-found confidence from regulators in extracting big fines from a banking system no longer teetering on the brink of collapse, has been a lucrative business for regulators, which have reaped about US$150bn from banks – mainly US firms but also European ones.

The size of the fines marks a step change, with Peter Henning, professor of law at Wayne State University Law School, saying that regulators now feel compelled to fine big if they want to get the attention of a large institution – many of which have more than US$250bn in assets, or a trillion dollars in some cases.

“There was a time when a hundred million dollar fine would have been effective. Now, anything less than a US$1bn fine is considered chump change,” he said.

So, even these days a billion dollar fine runs the risk of being called a slap on the wrist. When UBS was hit with a US$1.5bn fine from US, UK and Swiss regulators in 2012 after admitting its role in the Libor rate-rigging scandal, the US Department of Justice rather than being congratulated was criticised for not being more aggressive in the fine levied or in pursuing a criminal indictment.

The US attorney leading the case, Lanny Breuer, said the Libor scandal was one of the most significant to ever hit the global banking industry. In doling out the fine he fired back at critics that the goal was “not to destroy a major financial institution”.

Fine inflation

But as banks have grown healthier post-crisis, the ability of regulators to impose bigger fines without threatening the stability of the firm has risen. That has boosted the confidence of regulators, which in addition to record fines have also forced banks that no longer feel they can fight their regulatory overlords as strongly into signing guilty pleas.

In a US$2.9bn settlement with Credit Suisse over charges that it had conspired to aid tax evasion, the bank became the first financial institution in more than a decade to plead guilty to a crime. It wouldn’t be the last. BNP Paribas later agreed to settle up with the DoJ for US$8.9bn, pleading guilty to breaching US sanctions against Sudan, Iran and Cuba over a period of eight years.

The potential for future bank fines was enough for at least one money manager, Neil Woodford, to cut bait. Woodford sold his stake in HSBC, citing the risk of “fine inflation”. The bank paid a US$1.9bn money laundering fine in 2012, another US$2.3bn for mis-selling financial products in the UK and could be on the hook for more after Belgian authorities charged the bank with tax evasion and money laundering.

Banks were attracting fines as regulators and policy makers had cracked down on wrongdoings both old and ongoing, Woodford said, adding that the fines were increasingly sized on a bank’s ability to pay, rather than on the extent of the transgression.

That is a concern that US analyst Dick Bove has been raising for years. “There’s no economic backing or sense of justice behind the fines,” he said. “If the Justice Department thinks they can get the fine, they go after it.”

Bove argues that the fines have ballooned because banks themselves have been too willing to settle with regulators. Rather than face criminal prosecution of individuals or the institution, banks have been willing to open their cheque books. “You get a massive increase in the amount of fines when there is no opposition,” Bove said.

Several attorneys involved in settlement talks have described negotiations as aimed at putting a cap on liabilities, ending investigations and limiting fines – rather than pushing back against the fine itself.

Let the punishment fit the crime

Not everyone agrees with the fine inflation as a theory. The massive fines, many argue, are in balance with an unprecedented level of malfeasance: Culpae poenae par esto, or let the punishment fit the crime.

“We are not necessarily in an era of massive fines,” said Daniel Fetterman, a partner with Kasowitz Benson Torres & Friedman and former federal prosecutor. “Recent settlements and penalties arising out of the financial crisis have been so substantial because of the huge dollars involved in the alleged misconduct during the financial crisis.”

According to Fetterman, determination of a settlement is based on a range of factors, including the level of co-operation and strength of a company’s pre-existing compliance programme, and the application of those factors is highly discretionary. “It obviously is not a process that lends itself to quantitative analysis in the same way Wall Street firms run financial models,” he said.

Barclays chairman David Walker, who was set to leave his post at the end of 2014, argued that some penalties in the aftermath of the crisis could be considered disproportionately large. He said the overall scale of enforcement initiatives against the banks could only be regarded as indicative of grave failures of banks, essentially making it hard for the industry to win back public trust.

He stopped well short of vowing to fight overly aggressive fines. Still, in November, Barclays backed out of a five bank settlement over currency rate manipulation – not because the bank was gearing up to fight, but because the settlement did not include New York State’s Department of Financial Services, currently run by Benjamin Lawsky.

The DFS has the power suspend or revoke banking licences in New York, which has given Lawsky a role in many settlement talks next to the Securities and Exchange Commission, Commodities Futures Trade Commission, state attorneys general, the Office of the Comptroller of the Currency, the Federal Reserve and the Federal Deposit Insurance Corporation.

In addition to the US$8.9bn fine paid by BNP, the bank was slapped with a ban on its clearing US dollar payments for a year. That ban was imposed by Lawsky. His role as a power player has led lawyers for the banks to accuse regulators of trying to one-up one another in a race to grab fines and headlines.

“The government has a lot of cards to play,” said Jill Fisch, law professor at the University of Pennsylvania. “Since 2008 we are seeing fines like we’ve never seen before.” The view of some regulators at least is that the public has an appetite for accountability and they have decided to sate that appetite with big fines, she said.

“In order to make a point, however, each scandal seems to warrant a bigger fine than the scandal before it,” Fisch said.

To see the digital version of the IFR Review of the Year, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.