The troubles of a relatively small market on the geographical fringes of Europe have threatened to jeopardise the whole grand project, and dragged a number of other countries in similar predicaments to the brink. It has been a bumpy ride for Greece, a classic example of how rapidly problems can escalate when investor fear sets in. Michael Winfield reports.

This year the Hellenic Republic has a financing requirement of around €54bn. It had sold three benchmark deals in the first four months of the year, raising about €24bn by early April. The bulk of this was made up of a €8bn August 2015 deal and a €5bn June 2020 issue, together with the €5bn through a new seven-year bond. The balance of about €6bn consisted of bills sold in January and a €2bn FRN also sold at the beginning of the year.

In April there was a successful refinancing of these bills which attracted good levels of cover. It saw around seven times for the six-month and one-year bills, and 4.6 times for the three month bills on offer, just before the sovereign opened talks with the European Union and the International Monetary Fund for assistance. The reality was that Greece was unable to borrow longer-dated debt despite the inference from the bill auctions that there was very good demand for Greek assets. This presented the sovereign with a unique predicament within the eurozone.

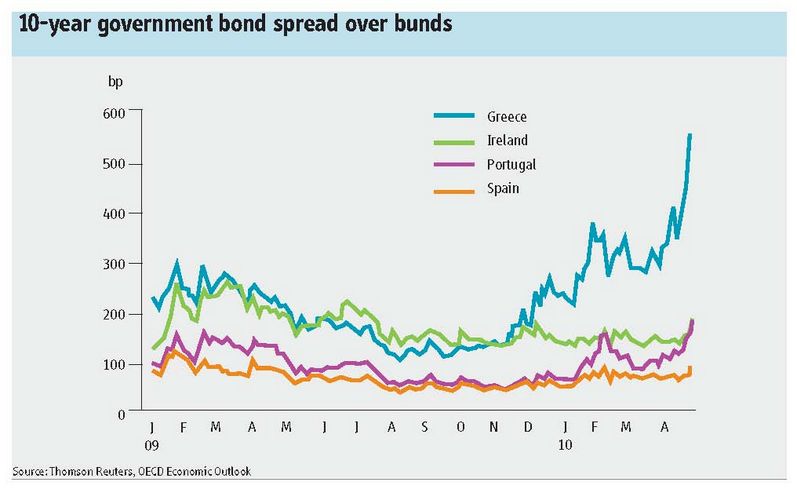

The success the Hellenic Republic had previously enjoyed in accessing the capital market was brought into question after both the five and seven-year deals sold this year suffered the ignominy of sharp spread widening after pricing. By mid-April the 10-year spread to Bunds peaked at around plus 630bp, compared to plus 225bp in early January. The liquidity of its outstanding debt continued to deteriorate as investors shunned the high returns on offer in favour of the liquidity of core European government bonds.

The deterioration in Greece’s standing relative to that of its peers saw the inversion of its outstanding curve. Doubts were growing over the sovereign’s ability to repay maturing issues, resulting in shorter dated spreads coming under the most pressure. After completing the new benchmark euro-denominated issues, Greece had started to consider other funding options. The US dollar market was one option, having been receptive to European sovereign debt as an alternative to high grade debt and Latin American sovereigns. This plan was subsequently placed on hold.

The risk for Greece is the possibility that the austerity programme it may have to agree to as a result of receiving EU/IMF support will create a deeper economic downturn, further reducing its ability to service its debt burden. The current state of the economy presents a challenging background against which the new measures are to be implemented: the quarterly profile for Greek GDP in 2009 was Q1 –1.0%, Q2 –0.3%, Q3 –0.5% and Q4 –0.8% and the official projection for this year is for a further decline. However, the Greek finance minister recently said he expected this to be less than the overall 2.6% contraction seen in 2009.

The problem is that the GDP figures make it much more difficult for the government to deliver fiscal reforms as the public are unlikely to support painful cost-saving measures. Fiscal adjustments are also more difficult to achieve: the lower GDP moves, the more work needs to be done to move the deficit/GDP figure lower. The application for external support can be read as recognition that the widening of spreads would probably deter many investors, and of the strain financing at these levels would put on its already stretched finances. Assuming that Greece was forced to borrow at the 8% yields at which its 10-year bonds were trading at one point, the refinancing of the €39bn in debt it has coming due over the next 12 months would add some €1.4bn–€2.5bn to its annual debt maintenance costs, according to Reuters. That would have raised Greece’s budget deficit by as much as 1%.

The Greek dilemma

The choice of a seven-year maturity by Greece was a fairly obvious one after it had already sold five and 10-year benchmark deals and avoided a fairly congested part of the existing curve in early 2012. The new issue was priced at mid-swaps plus 310bp, after trading in the grey market at less 15 cents. In the days after pricing it was quoted at mid-swaps plus 350bp–340bp.

One criticism of the transaction was the reliance the sovereign still had on domestic bank participation, which was significantly higher than for its previous two deals. Banks accounted for 42% and domestic investors 43% of the bonds sold.

By comparison the 10-year issue, which attracted a final book of more than €16bn, saw banks account for 24.5% and Greek investors 23%. The five-year comparables were 28.5% and 26.2% respectively with a final book in excess of €25bn. Clearly, the sovereign had a much higher reliance on the Greek banking sector for this deal, which in turn uses the asset as repo-eligible collateral with the ECB.

The change in the ECB’s rules relating to repo collateral meant that Greece, rated A3/BBB+/BBB- after Moody’s and Fitch’s latest downgrades in April (from A2 and BBB+ respectively), leaves the sovereign close to a point where its debt ceases to be eligible. The latest downgrade was sparked by an increase in fiscal challenges amid increased interest costs and worsening growth potential. It will likely cost the country more than expected to finance its wide deficit. Fitch said current circumstances would make Greece’s plans to reduce its deficit to 8.7% of GDP this year more difficult. Moody’s believes there is a significant risk that debt may only stabilise at a higher and more costly level than previously estimated.

The maintenance of a minimum Single A minus rating remains crucial for the domestic banking sector which uses Greek debt as eligible repo collateral. The credit threshold for marketable and non-marketable assets was previously lowered from A– to BBB–, with the exception of asset-backed securities, and a haircut add-on of 5% on all assets rated BBB–. The ECB has, however, recently offered a higher degree of flexibility in the conditions applied to repo operations with the introduction of a new hair cut regime to allow for credit differentiation between sovereigns. This takes the form of a schedule of graduated hair cuts for the valuation of assets rated between BBB+ and BBB-, replacing the uniform 5% hair cut that had previously been applied.