Earlier this year Indonesia and the Philippines joined the club of emerging market nations able to borrow larger amounts of money for longer periods on the international capital markets – proving they have come into their own on the international debt scene. But sustaining investor enthusiasm against a challenging global backdrop will require an unwavering commitment to structural reform.

To view the digital version of this report, please click here.

Every emerging market nation, as it progresses along the path towards becoming a fully fledged market economy, aspires to improve its standing with the international investment community by lengthening its sovereign debt curve.

Indonesia and the Philippines issued bumper bonds with 30 and 25-year tenors, respectively, to an enthusiastic audience of domestic and international investors. From this point on, most investors believe there’s only upside to be had for both nations. Their improving macro fundamentals, bolstered by the structural reform agenda they have undertaken, can only place them on a solid footing for the future, particularly when compared with an increasingly lacklustre Europe, where for many nations the future looks quite dim.

“The fiscal fundamentals have been very favourable to both Indonesia and the Philippines,” said Rajeev De Mello, head of Asian fixed income at asset management firm, Schroders in Singapore. “During a time when budget deficits and total debt have risen substantially in Europe, the US and Japan, many Asian governments appear relatively virtuous. Both countries have demonstrated lower deficits as a percentage of GDP and their total debts are no longer the worry they were in the early 2000s.”

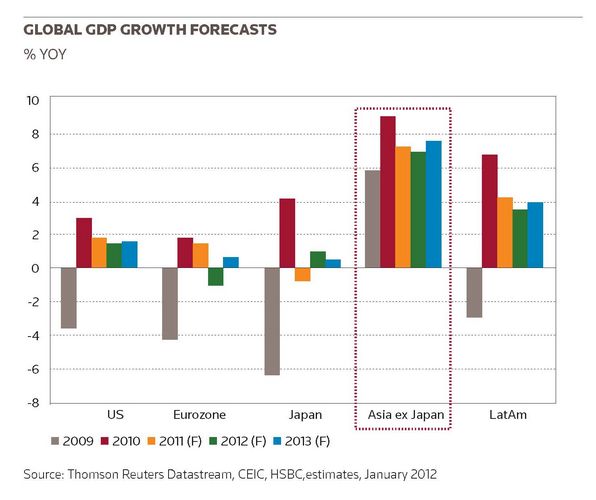

Both Indonesia and the Philippines attest to the growing divergence between developed and emerging markets, said Arthur Hovespian, senior emerging markets strategist at investment firm Payden & Rygel in Chicago. “We have seen improvements in many indicators that ratings agencies look at, notably debt-to-GDP levels, reserve accumulation and low fiscal deficits. These have been working towards the positive for Indonesia and the Philippines, while in developed countries, the indicators have been heading in the wrong direction. Overall, Indonesia and the Philippines demonstrate the qualities that attract investors to sovereigns and they are an example of the overall emerging market story.”

In fact, the strong fundamentals of both nations have caused the spreads on their external, dollar-denominated debt to narrow to levels at which they are no longer that attractive to investors such as Hovespian. The opportunities are better, he says, in the quasi-sovereign and even corporate sectors of both countries – which is a good sign and yet another testament to the improving picture both countries present.

“We have seen improvements in many indicators that ratings agencies look at, notably debt-to-GDP levels, reserve accumulation and low fiscal deficits. These have been working towards the positive for Indonesia and the Philippines, while in developed countries, the indicators have been heading in the wrong direction”

“Corporates [in Indonesia and the Philippines] will continue to increase their issuance to take advantage of lower yields and spreads,” said De Mello.“Global investors are also increasingly interested in buying corporate bonds from emerging market countries. Global pension funds have to invest and they do have large holdings in fixed income. In an environment of extremely low yields in the US, Germany, France and Japan, I do expect allocations to Asia to continue to increase.”

From here on, then, things can only get better, investors believe, given the juxtaposition of the global economy and each country’s individual strengths as they support their growth.

Indonesia is an exporter of a broad range of commodities, and higher commodity prices have been a real plus for its economy, while the Philippines has always benefited from and continues to take advantage of inflows of remittances from its large expatriate communities around the world.

It is also one of the world’s most important centres for business process outsourcing, and “in the last five years, the country has seen a significant growth in its call centre and related off-shoring services”, said De Mello.

The Philippines has also benefited from low inflation – a real plus point today, when inflation is a major concern for many emerging markets, and the government is doing a “fine job in applying the right policies to keep it under control”, said Hovespian. “The authorities don’t want the currency to appreciate too fast, so they are using the right policy tools to maintain a good balance for their economy.”

But as much as these countries may be set on a positive course for future growth, things can also turn around very quickly for them if they are not mindful.

At the macro level, their dependence on China – which has been a huge plus for both countries – could eat away a good part of their growth, said Sanjeev Kumar, director and group CEO at Delamore & Owl in London.

Both Indonesia and the Philippines trade actively with China, and the slowdown in China’s demand for resources is hitting many domestic companies hard, he said. “Indonesia is an open economy but cheap imports from China have caused a lot of headache for authorities in Indonesia as smaller producers there continue to struggle and go under.”

And at the micro level, inflation in Indonesia could prove to be a concern. Thus far, monetary policy in Indonesia has been directed more towards stimulating further growth rather than addressing the risk of future inflation, and even though recent inflation data show only a 4% increase over the past year – a very low figure for Indonesia – investors need to monitor this closely, De Mello said, because the low inflation rate has largely been a consequence of governmental subsidies for gasoline, which are a subject of great debate and which could be removed at short notice.

A strict commitment to structural reforms will be key for both Indonesia and the Philippines if they want to keep up the positive momentum and continue to attract foreign investment.

“The recent announcement by the government of Indonesia to limit and restrict the foreign ownership of the country’s mining assets is probably a step in the wrong direction,” said Kumar, “and while there is always legal uncertainty in Indonesia, the government is going to have to work doubly hard to make sure they fast-track reforms and continue to keep foreign investors interested.”

That said, though, the ratings agencies have been upgrading both countries and in January, for the first time since the 1997 Asian financial crisis, Moody’s moved Indonesia up to investment-grade level.