The potential risk posed by Venezuela and Argentina to Andean development bank CAF – flagged up by Standard & Poor’s in October – is largely illusory.

The photographic term “double exposure” may have been coined to describe an occupational hazard when using traditional film cameras, but it also captures well the real nature of the risk posed to Latin American development bank Corporacion Andina de Fomento by its two main creditors.

Just as in the accidental effect when one photographic image is superimposed upon another, the supranational’s exposure to the problems of its largest sovereign borrowers Argentina and Venezuela – flagged up by Standard & Poor’s in October – is largely illusory.

The ratings agency may have revised its outlook on Corporacion Andina de Fomento from stable to negative but the real picture at CAF is bright, not blurred, with growth assured by Latin America’s insatiable appetite for infrastructure development.

Diego Ferro, co-chief investment officer at Greylock Capital, said: “This is the typical kind of response from a ratings agency. From a regulatory standpoint and a ratings agency standpoint, I’m not surprised S&P said this. But it doesn’t reflect the reality for CAF – which is one of solid credit.”

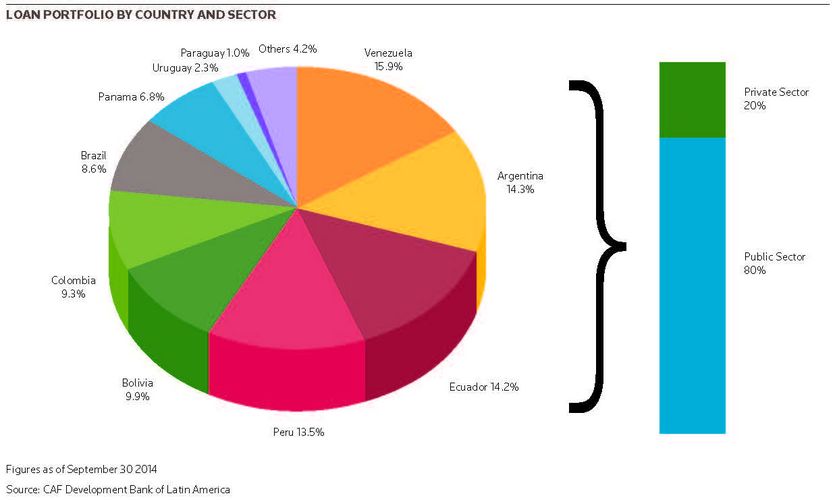

CAF has become the leading development bank in financing infrastructure and energy projects in the region, but S&P said weakening credit conditions in Venezuela and Argentina posed mounting downside risk for its risk-adjusted capital adequacy. Collectively, the two countries’ exposures accounted for 28% of CAF’s loans as of August 31 last year.

S&P is concerned about continued economic deterioration and tightening external liquidity in Venezuela and said the likelihood of Argentina remaining in default on its discount bonds for a protracted period had risen.

The ratings agency revised its outlook on CAF to reflect its view that there is a greater than one-in-three probability that Venezuela could default on its foreign-currency commercial obligations while Argentina remains in non-payment status. If this occurs, it expects CAF’s risk-adjusted capital ratio to fall below the 15% lower threshold of its adequacy range.

S&P’s position is important because CAF’s success in accessing the international capital markets is mostly due to high credit ratings – the highest of Latin American debt issuers. It is rated Aa3 by Moody’s, AA– by Fitch, and AA by JCR.

The broadside also follows S&P downgrades of Argentina to selective default in July and Venezuela to CCC+ in September.

Limited significance

Nonetheless, there is a clear consensus among those spoken to by IFR that the S&P revision has limited significance.

Walter Molano, head of research at BCP Securities, said: “It is all super-senior credit so there is no risk. CAF is very strong and well regarded. It issues a good deal and has extremely solid roots in the region.”

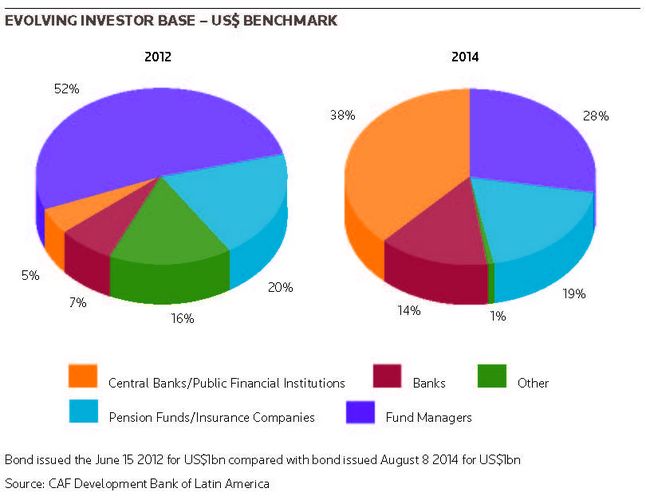

A senior DCM banker in the US pointed to CAF’s remarkable transformation in recent years from emerging market lender to the elite status of supranational.

“The S&P revision means nothing – or very little. Why? Because of CAF’s transformation over time. They had for many years just been regarded as something of an emerging market issuer, a blue-chip iron-clad emerging market issuer, but an emerging market issuer nonetheless. But with their Double A ratings they have now graduated into an elite class and we have seen it with their spread performance,” he said.

“Spreads have compressed dramatically over the last year or so. They can do whatever they want: they can issue in virtually any market and they can look for the most attractive pricing,” said the DCM banker.

Moreover, S&P is also at pains to point out the steps that CAF has taken to fortify its capital position. Since the spring of 2014, the development bank has incrementally raised its current and projected capital adequacy by slowing loan disbursements and planning for loan diversification over the next few years.

CAF is recognised as being highly liquid and has taken steps to boost liquidity even further. S&P said that in 2014 the bank strengthened both the quantity and quality of its liquid assets, which stood at US$11.3bn by the end of September 2014.

Liquidity policy

A key move in mid-2014 by CAF was to update liquidity policy, which now stipulates that it holds liquid assets sufficient to meet at least 12 months of net cash requirements.

“CAF is incredibly liquid. They are sitting on a stockpile of cash. In the last year they have taken great measures and they should be well positioned for whatever may befall Venezuela and whatever happens in global markets,” said the DCM banker.

CAF’s strong position aside, how solid are S&P’s concerns about Venezuela and Argentina?

Opinion is divided over the risk of Venezuela defaulting, although since late last year some analysts have begun arguing that falling oil prices suggest this could be on the cards.

According to David Rees, emerging markets economist at London-based economic research consultancy, Capital Economics, a Venezuelan default is likely in 2015.

“The Venezuelan economy faces a multi-year recession following the recent fall in oil prices. GDP probably contracted by 3.5% last year and we now suspect that it could decline by another 5% this year. But recession is probably the best-case scenario. With the balance of payments on the verge of crisis, a default on foreign currency debt later this year is becoming increasingly likely,” said Rees.

Venezuela’s chief problem is its overvalued currency – but another issue is politics. There are concerns that President Nicolas Maduro will delay unpopular policy moves ahead of national assembly elections late this year. The market is already pricing in higher default probabilities going into 2017.

Yet this still does not mean a great deal for CAF and, while the falling price of oil has clearly hit Venezuela, Caracas is sitting on large assets that it can monetise.

Political factors also loom large over Argentina’s credit profile with analysts suggesting that the government is unlikely to reach an agreement with its holdout creditors before October’s presidential elections.

S&P also points to CAF’s preferred creditor status. Members have kept current on debt service to it even while running arrears to commercial creditors. The expectation would be that even if Venezuela were to default, the country would always pay CAF back first. Even Argentina, with all the problems it has faced, has never defaulted on an obligation to CAF.

Ferro at Greylock Capital said that from a practical standpoint when there is talk of a default CAF can be considered a multilateral.

“The market may be overreacting towards Venezuela. Yes, they are in a worse position because of the oil decrease, but for them to really stop paying CAF looks highly unlikely. And despite all the problems that Argentina has, it has been maybe the best performing emerging market in the last two months.”

In short, CAF’s hard-earned status as a key pillar of stable development in a region accustomed to turbulence makes it bullet-proof.

Its evolution has been consistently impressive since a process of expansion began in 2006 that has taken it well outside its original Andean base. Bank members now comprise 17 Latin American and Caribbean countries, Spain, and Portugal. Barbados, the newest member, joined this year.

Such has been its trajectory that its lending portfolio is on the verge of overtaking the IDB and CAF also eclipses the flagging Banco del Sur.

However, in many ways this growth should be no surprise in such a rapidly developing region. The economies of its core members have grown apace and infrastructure development is at the heart of the CAF story.

In a recent interview, Antonio Juan Sosa, CAF’s vice-president of infrastructure, acknowledged this, saying CAF had been able to take advantage of a de facto retreat from infrastructure development by the IDB and World Bank in the 1990s.

CAF’s strong business profile also reflects its concentration on public sector lending (80 per cent of its loans). Regular shareholder injections of new capital have reinforced its ability to weather downturns and CAF also has few non-borrowing members. Those with knowledge of the bank also point to its exhaustive international marketing to investors through roadshows.

Given its role, CAF has faced familiar criticisms about transparency from NGOs that all large multilateral funders of infrastructure periodically confront.

In a 2008 report the Washington-based Bank Information Center (BIC) said that despite its reach CAF had largely functioned beneath the radar of public scrutiny.

Christian Velasquez-Donaldson, the BIC’s Latin America acting programme manager, told IFR: “They still don’t have an access to information or transparency policy that will allow anybody to request any information regarding their projects either from the point of view of social and environmental policies or procurement.”

Regarding transparency, IFR was unable to secure an interview with CAF for this article. The bank also appears sensitive about the S&P revision: it has made no comment about it and only posted S&P’s October research update on its website in January – three months later – after being contacted by IFR.

Nonetheless, given the bank’s growing profile there is no doubt that for CAF the risk posed by the double exposure to Venezuela and Argentina is illusory – and its focus remains clear.

The senior DCM banker in the US said: “I believe the future is very bright for CAF and it will continue its ascendancy towards Triple A. Its superstructure is special: CAF has really done a great job of convincing investors, doing the right thing, running a very solid bank, while also doing good for the region as well through the myriad projects they finance.”

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.