Deutsche Bank paid some of the widest spreads in the European senior market so far this year as it brought a €3.57bn-equivalent four-tranche transaction last Tuesday, its first public bond sale in what is likely to be a pivotal year for the beleaguered bank.

The German national champion reported its first annual profit in four years on February 1, but its ongoing struggles to overhaul the business, and speculation over a potential merger with Commerzbank, have taken their toll on its funding costs.

The self-led senior non-preferred trade found good traction and each of the four tranches were launched 20bp tighter than initial price thoughts. Combined books for the three euro note tranches passed €6.5bn with more than 450 accounts taking part.

But the absolute spreads - as well as the final concessions - were high. Deutsche sold a €1.5bn two-year at 180bp over mid-swaps, the joint widest senior bond in any tenor sold in the year to-date apart from CaixaBank’s €1.5bn February 2024 SNP (Ba1/BBB/BBB+) issue, which was priced at swaps plus 225bp.

The bank’s fully loaded Common Equity Tier 1 capital ratio looks sound at 13.6% and its liquidity reserves sit at a healthy €259bn, but many investors remain relatively cautious on the credit.

“They have a challenging restructuring plan, which at the end of the day doesn’t lead to particularly attractive returns,” said Andrew Fraser, head of financial research at Aberdeen Standard Investments.

“They’ve obviously got funding requirements to do and their loss-absorbing buffer has to remain quite high, which helps maintain ratings. But funding costs are quite high and have an impact on earnings, so they’re caught between a rock and a hard place.”

KEY PRIORITY

The bank is on negative outlook at Moody’s, and a downgrade of its SNP debt from the current Baa3 would take it into junk territory. That could reduce demand from certain investors who manage against a benchmark, potentially further weighing on spreads.

Deutsche’s management stressed on last week’s investor call that lowering its funding costs is “a key priority” for the bank as it strives to generate long-term, sustainable profitability.

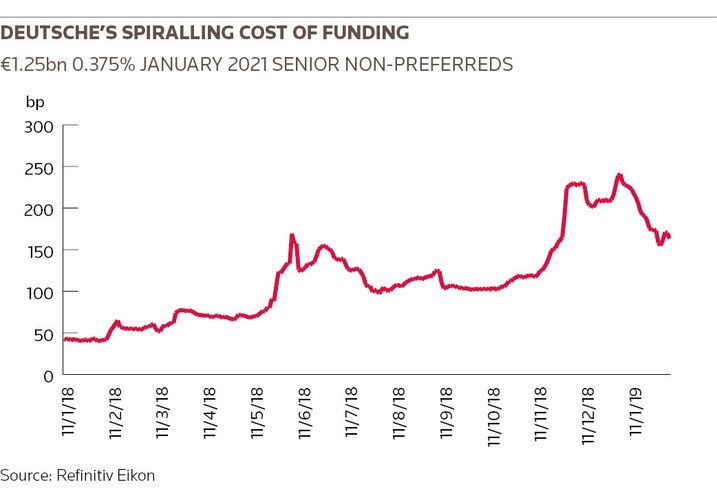

But Wednesday’s transaction, executed just two days after that call, nonetheless lays bare the extent to which its funding costs have deteriorated over the last year.

It sold a €1.25bn three-year SNP issue last January at 40bp over swaps, which was trading at around four times that level last Tuesday, opening in the high 150s before widening another 10bp.

Banco Santander issued €1.25bn of January 2025 bonds the same day last January at swaps plus 60bp, but its subsequent widening has been less severe – it was last quoted at swaps plus 120bp last Tuesday, according to Tradeweb.

The bank was “not pleased” with its spread levels in recent months, Dixit Joshi, group treasurer at Deutsche Bank, said on the investor call, adding: “Notwithstanding the fact that iTraxx financials over the year had widened significantly, we had widened much more.”

GUNNING FOR SIZE

Deutsche also launched a €750m three-year at 200bp and a €750m seven-year at 230bp. Its £500m five-year was launched at a spread of Gilts plus 305bp on the back of more than £1.1bn of orders. All bonds are rated Baa3/BBB–/BBB+.

The bank was admittedly looking for size but final concessions of at least 20bp on the shorter euro tranches and sterling bucked the trend of diminishing concessions seen in recent weeks.

The seven-year looked cheaper, given that Deutsche’s March 2025s opened at around swaps plus 189bp, but this part of the curve is artificially tight after the bank repurchased bonds due 2025 and 2028 last November.

A Deutsche syndicate banker told IFR that it had a strategy “to minimise overall funding costs, ensure investor diversification and minimise new issue premiums”.

“[The deal] succeeded impressively … It is the largest transaction in the European FIG sector this year. The deal closed 5bp tighter, highlighting that it was priced appropriately,” the banker said.

KICKING THE CAN?

The issuer has plenty of funding tools at its disposal, including private placements, covered bonds and access to deposits, which should help reduce its blended cost of funding. But the inclusion of short-dated tranches was arguably surprising given MREL-eligible debt, which loses regulatory value in the last year of its life, tends to be issued in longer maturities.

Bankers away from the deal said Deutsche’s approach of hitting short to intermediate tenors - and taking the largest size in twos - made sense given longer-dated tranches would come at a punitive cost.

“They are probably seeing this as a temporary blip and not wanting to pay up for the full cost of the curve by taking size further out,” said a rival syndicate banker.

“It sort of kicks the can down the road a bit, and they’re going to have an aggressive redemption profile if they keep issuing short, but it’s probably cost concerns dictating that.”

The bank is already compliant with its MREL target, reporting a €21bn buffer over its requirement at year-end 2018. It has sizeable MREL-eligible roll-offs this year, however, amounting to some €16bn – twice the SNP maturities due in 2020.

The issuer is aiming to raise €9bn–€11bn through SNP paper and €6bn–€8bn through senior structured/preferred over 2019, according to its funding plan.