Overcoming tough obstacles

In a year that was the most difficult and turbulent in emerging markets since the financial crisis, banks needed to display great skill and leadership. None did so better than Citigroup, which is IFR’s Emerging Markets Bond House, Asia Bond House and Emerging EMEA Bond House of the Year.

From a corruption scandal in Brazil to an economic slowdown in China and continuing political ructions in Central and Eastern Europe and the Middle East, 2015 has proven to be the most tumultuous year in emerging markets since 2008.

Throw in the volatility driven by an indecisive US Federal Reserve, the European Central Bank’s bond-buying programme and renewed worries around Greece, and it is little wonder that bankers covering the emerging markets debt capital markets have been left feeling a little frazzled.

Most banks can no longer offer a comprehensive global emerging markets business – and many are scaling back their ambitions.

So in a year in which clients needed their hands held more tightly than ever, issuers turned to the banks that have long-standing credentials with the best global platforms. It’s no coincidence that HSBC and Citigroup are a clear one-two in the global emerging markets league table.

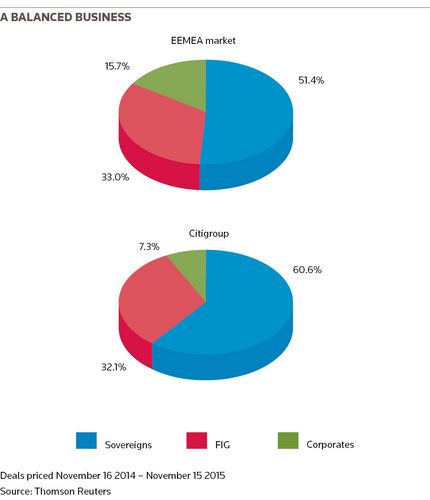

While HSBC is top of that table, Citigroup’s strength across regions is the reason it takes the award for best global EM Bond House. It is the only bank that ranks in the top four for international bonds for every developing region over the awards period, according to Thomson Reuters data – Asia, Latin America, Central and Eastern Europe, the Middle East, and Africa. Africa, which has seen decent flow this year, remains a thorny market for HSBC, where it’s not even a top 20 player.

The US bank, moreover, has also been involved in IFR’s best EM bond deals. Jamaica’s US$2bn dual-tranche offering from July is IFR’s Latin America Bond of the Year, while the US$8bn multi-tranche offering from Alibaba from November 2014 is the equivalent in Asia.

Syndicate

One reason for the bank’s success is that it is one of the few houses that still has experienced syndicate officials dedicated to just emerging market transactions. Most other banks have combined their emerging markets capabilities with other sectors such as corporates or FIG, especially in emerging EMEA – where volumes have halved from just two years ago even with redemptions hitting a record level.

“A specialist emerging markets skill-set is needed more than ever,” said Geoff Hunter, head of EM syndicate at the bank. “As distribution becomes more challenging, the ability to read demand from around the world is really important.”

While Citigroup is still winning plenty of business – a challenge in itself given the reduced needs of issuers to raise funds in a slow-growth environment – executing deals has proven even trickier, especially for clients used to tight pricing.

“There’s a massive fixation on the secondary market levels and the new issue premium needed. That’s where trust and advice come into play,” said Samad Sirohey, head of CEEMEA debt capital markets.

That has meant adopting different strategies to fit clients’ needs. Sometimes that has led to deals being delayed. “It’s about manoeuvring around the volatility,” said Peter Charles, head of EMEA fixed-income syndicate.

Romania is one such example. It mandated banks in February but waited until October to print. “That was about having the confidence not to rush to market,” said Charles.

At other times, it has meant identifying different ways of accessing liquidity, through different structures. In March, for example, Citigroup was a bookrunner on ICBC Leasing’s US$1bn dual-tranche offering of three and five-year Reg S bonds, while in November Citigroup helped ICBC Leasing access the 144A market for the first time with a US$1.5bn triple-tranche transaction that included floating-rate notes.

While Asian accounts dominated both deals, the issuer now has the opportunity to build a more diverse investor base.

“Liquidity has become a global pool [for Asian issuers],” said Adrian Khoo, co-head of Asia debt origination.

Asia strength

Asia has become by far the most dominant emerging region in terms of new issuance. So the fact that Citigroup is also IFR’s Bond House of the Year in Asia is a big reason behind the bank winning the global award.

Its lean team of DCM specialists did more than their fair share to develop the Asian bond markets, helping lead many of the milestone trades across the region.

While Citigroup has thinned out its structure and slashed billions of dollars from its balance sheet since its own 2008 crisis, it has hung on to corporate relationships across Asia and clawed back its share of the G3 market, proving that it is possible to be a top bond house without piling on credit risk in the process.

Top of its list of transactions is Alibaba, which smashed the record for the biggest international offering from an Asian credit. The deal required a bold sales pitch, pricing more in line with US technology names than any of its regional peers.

Then in May, Citigroup helped South Korean corporate issuers find a way to access offshore investors and diversify their funding sources, bringing department store operator Shinsegae to market with a US$300m credit-enhanced perpetual, the first bank-guaranteed hybrid globally.

It followed this with a top-line mandate on China’s first core Tier 2 capital offering – for China Life Insurance in June. The deal introduced a new format for regulatory capital, but came before Chinese authorities had clarified what would constitute a trigger event. Careful structuring and comprehensive investor education around the deal’s extendible maturity paid off, as China Life met its US$1.28bn target at a yield of just 4%.

Citigroup also worked on two landmark covered bonds in 2015, first as a joint bookrunner for DBS Bank’s US$1bn trade, Asia’s first statutory covered bond, and then as one of three leads – and the only US house – on a US$500m Triple A benchmark from Kookmin Bank, half of which went to US investors.

“We’ve been tested in origination and in execution,” said Duncan Phillips, head of Asia debt syndicate. “It’s been a challenging year, but it’s been an interesting year.”

Citigroup scored key roles across the region and across the asset classes. It demonstrated its structuring abilities on a US$289m offering for Delhi International Airport in January, the first high-yield issue from Asia in 2015 and a rare international issue from India’s infrastructure sector.

At the other end of the scale, it worked on many of the year’s biggest deals, including Petronas’s US$5bn multi-tranche deal in March, the largest ever from a South-East Asian issuer, followed by Asia’s largest dual-currency offering for Sinopec the following month, as well as a US$3.8bn trade for CNOOC.

Market share

As well as winning the Asian regional award, Citigroup is also IFR’s Emerging EMEA Bond House of the Year. In a tough year, Citigroup is top of the league tables.

“What’s pleasing is that we’ve maintained our market share and position,” said William Weaver, head of EMEA debt capital markets, albeit the former is down by a percentage point on 2014.

Still, Citigroup is the only bank in the region with a double-digit market share. It also executed more transactions than any other bank.

Citigroup faced strong competition from Barclays, in particular. But the US bank has had a better balance of business – Barclays has underperformed in the financials sector, especially in the Gulf, where it was involved in the most high-profile failed deal of the year, a pulled transaction by Abu Dhabi Commercial Bank.

“Whether it’s CEE, MENA or Africa, you’ll find us in the zip code,” said Weaver.

Citigroup’s impressive showing is not just limited to new issues, though. It leads the way in liability management too, which has become a growing opportunity.

“With what happened in December in terms of market dislocation, we made a huge effort in liability management,” said Sirohey, referring to a big sell-off in emerging markets bond prices at the end of last year.

Citigroup was involved in eight liability management transactions in the awards period – six from Russia, including for the likes of VTB, VimpelCom and IMH (formerly known as Koks). That latter deal was an exchange offer on the outstanding June 2016 bonds for new December 2018 notes. Those notes were the first new Russian securities issued in the international markets in 2015.

Citigroup was then involved in the first big benchmark trade by a Russian issuer, when it was joint lead on Norilsk Nickel’s US$1bn seven-year deal in October. A strong order book saw fund managers dominate the allocation, taking 76%. Significantly, as a 144A transaction onshore US investors demonstrated their support for high-quality Russian issuers, getting 34% of the new paper.

Citigroup’s ability to lead blockbuster transactions was again illustrated by its participation in the two biggest CEEMEA deals of the year – a US$4bn dual-tranche offering by Kazakhstan, which was issued in a tight window with markets rattled by Greece, wobbly oil prices and whipsawing Chinese equities, and a €3.1bn triple-tranche transaction by Bulgaria.

The latter is the largest euro offering by an emerging markets issuer and took advantage of the rally engineered by the ECB’s bond buying programme.

Leading outfit

Citigroup was just as strong in the Middle East and North Africa region, where the US bank was the leading outfit. It was involved in key bank capital trades, such as National Bank of Kuwait and National Bank of Abu Dhabi, as well as all sovereign transactions from the region.

These included two deals each by Lebanon and Jordan (with one backed by the US-Aid agency), as well as offerings from Egypt, Ras al-Khaimah and Tunisia.

“We believed MENA volumes would hold up and put more resources there,” said Sirohey.

The one relatively disappointing area was sub-Saharan Africa, but even there Citigroup was involved in one of the more successful deals of the year, for Cote d’Ivoire. At the time, in February, the US$1bn 6.375% March 2028 amortising note issue was the longest bond offering by a sub investment-grade African sovereign.

In Latin America, Citigroup was knocked off its top perch by Bank of America Merrill Lynch, but it still had a very consistent year with a top three position in every sub-sector and sub-region.

With Brazil, the region’s biggest market, closed for long periods because of the Petrobras scandal, banks had to turn to other areas for business. For Citigroup that was easier than it was for rival banks given the breadth of its operations in the region, which span over 20 countries.

Apart from Petrobras’s Century bond, Citigroup was involved in arguably all of the key deals from the region, including a US$2bn dual-tranche offering from Jamaica.

The deal allowed Jamaica to cut its consolidated public debt-to-GDP ratio by about 10 percentage points. Three-quarters of the proceeds are being used to buy back Petrocaribe debt from Venezuelan state-owned oil company PDVSA.

The bank was also involved in innovative Euroclearable transactions through the issuance of Certificados Bursatiles (Cebures) for Pemex and Opsimex, an infrastructure subsidiary of America Movil. The Cebures structure offers investors outside of Mexico a cost-efficient route to access domestic Mexican peso-denominated securities.

Another innovative deal was for Colombia Telecomunicaciones, the first hybrid corporate offering from the Andean nation. The deal received 50% equity content from the ratings agencies and enabled the company to continue meeting Colombian legal requirements after it migrated to IFRS accounting standards.

Citigroup’s ability to ride the waves of volatility was evident in the US$425m debut trade in November for Terrafina, a Mexican real estate investment trust. The deal was priced after a two-month wait. It was the first true corporate from the region since the summer sell-off.

“No one has the same expertise in the bond IPO space as us,” said Blake Haider, managing director in the bank’s Latin credit markets business.

Citigroup was also a bookrunner on a rare Green bond from the region for Brazilian food company BRF, which was a euro offering to boot.

To see the digital version of the IFR Review of the Year, please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@tr.com .

<object id="__symantecPKIClientMessenger" style="display: none;" data-extension-version="0.4.0.129" data-install-updates-user-configuration="true"></object>