The election of a conservative president ends 12 years of populism in Argentina – but investors should be realistic about the pace and scale of proposed reforms.

Argentina likes to confound and lived up to its reputation with the election in late November of conservative Mauricio Macri as president, bringing to an end an era of populism that has isolated and stunted its economy.

The result was a clear vote for change, despite the slim margin of victory by the centre-right candidate (Macri won 51.5% of the vote, compared with 48.5% for his Peronist rival, Daniel Scioli of the ruling Frente para la Victoria).

But although markets responded enthusiastically to Macri’s pro-business agenda, investors would do well not to overestimate the prospects for dramatic reform: the new administration inherits a toxic legacy of endemic inflation, stifling currency controls and debt default – and the political support it will need to engineer change is flaky where it matters most.

Edward Glossop, emerging markets economist at Capital Economics, said: “The outlook for the economy has undoubtedly brightened. We still see some reasons to be a little bit cautious, but the economic adjustment that the country desperately needs could be just around the corner. It is the start of a new era because undoubtedly we are going to see positive change – the only question is how much change and how quickly.”

Macri is a two-term mayor of Buenos Aires and leader of the Cambiemos opposition alliance. His victory over Scioli – hand-picked as the Peronist candidate by the outgoing president, Cristina Fernandez de Kirchner – tapped into deep frustration with “Kirchnerism”, a protectionist and confrontational style of statism that in recent years has stunted growth.

As the investors’ choice for his promise of shock therapy, Macri’s win sent ripples of unease through left-of-centre governments in neighbouring Brazil and as far afield as Venezuela, while raising the prospect of improved ties with the US and Europe.

Nevertheless, the scale of the task confronting him should temper excessive optimism.

Plugging the holes

Official Argentine figures put economic growth in 2014 at 0.5% but many analysts cast doubt on this and suggest Latin America’s third-largest economy contracted. Estimates for this year among multilateral bodies have varied wildly from 0.4% to 1.6%.

There is broad consensus that Argentina needs access to international finance to plug a soaring budget deficit financed by printing money that has fuelled double-digit inflation. Fiscal and monetary policies have been excessively loose as Fernandez and her predecessor, Nestor Kirchner, expanded welfare programmes, and high inflation has pushed up the real effective exchange rate, fuelling concerns about dwindling reserves.

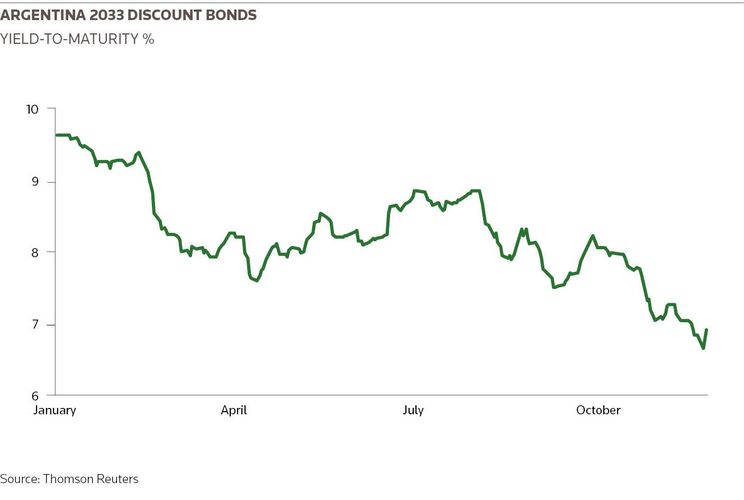

Officially these stood at US$27bn in October, but in reality are generally thought to be much lower once debt arrears and other outgoings are subtracted. Buenos Aires must tap external capital, and to do that a new government must settle with the holdout creditors who refused to participate in debt restructuring after 2001.

For the capital markets, the approach of the presidential candidates to the holdouts was the key barometer of their commitment to change – Scioli was steadfastly ambivalent, and the consensus view was that Macri would be more decisive.

But during the long political campaign that culminated in Macri’s victory, several factors qualified the conservative candidate’s robust image. He moved inexorably towards the centre, softening his stance on orthodox policies, and faced the recurrent threat of divisions within his own eclectic coalition.

Walter Molano of BCP Securities and author ofIn the Land of Silver, a history of Argentina’s political economy, said: “Macri really has a strong conviction of applying a shock therapy to the country and addressing some of the things that really need to be addressed very quickly, ie, devaluing the currency, realigning it with trading partners, and in a very short time period removing subsidies and normalising the fiscal accounts. But he’ll still have to deal with the legislature and senate, controlled by the Kirchneristas.”

Nervousness among voters

A recurrent theme during the electoral campaign that limits his room for manoeuvre was nervousness among voters about the prospect of pro-market policies that threaten to erode salaries and dent pensions. Kirchnerism was built on welfare spending and subsidies, and in the 2000s generated strong growth on the back of rising commodity prices, higher government spending and higher public sector employment.

Moreover, the country has a troubled relationship with non-Peronist presidents – Macri is only the third since 1983 – and his rivals lost no opportunity to fuel fears of a future crisis on his watch rooted in long memories of the 2001 collapse under Fernando de la Rua.

These factors strengthen the old saw in politics that radical change must be undertaken quickly, and Macri is likely to spend his honeymoon period furiously trying to build cross-party backing for reform.

That will be easier said than done. While he has a potent power base in the federal government, Buenos Aires province and the country’s capital, in congress he will have to forge alliances with other parties that might not be politically or economically aligned to his own coalition, which itself includes centre-left groups that will bridle at his more radical ambitions.

“No matter how you spin it, to push through all the necessary changes there has to be a guy who is 100% committed to reforms and not 70% committed: credibility is crucial”

Tim Umberger, senior adviser at East Capital, said: “No matter how you spin it, to push through all the necessary changes there has to be a guy who is 100% committed to reforms and not 70% committed: credibility is crucial, and it is very clear that the market will assign much higher credibility to Macri.

“Given Argentina’s problems, if you simply look at things in economic terms it is very clear what has to be done; but what is of course more complicated – as it always is in Argentina – is that you have interim elections every two years, and you always need to manoeuvre politically.”

Small window

A poor showing in the mid-terms could weaken Macri’s mandate further – and set the Peronists up for a presidential comeback in 2019 after the centre-right leader has taken the flak for the inevitable belt-tightening. In the meantime, the continuing popularity of Kirchner, despite the country’s economic malaise, will limit her successor’s long-term options. Some observers are already speculating that she will bounce back to run for a third presidential term in 2019.

While Macri is likely to move quickly to restore the credibility of official economic data and eliminate taxes on grain exports, it may take longer to dismantle capital controls and unify the exchange rate.

Currency traders have been betting on a steep devaluation, and Macri indicated that he would allow the exchange rate to float freely straight away. But efforts to scale back energy and transport subsidies that have swelled the fiscal deficit will be deeply unpopular, suggesting such moves could take longer than he has promised.

“It is the start of a new era because undoubtedly we are going to see positive change – the only question is how much change and how quickly”

Roberto Lampl, head of Latin American investments at Alquity, said: “The transition from failed country to global power is likely to be both bumpy and slow. Macri will have to undo 12 years of damage but looks set to prioritise the economy and growth during his presidency.

“Whilst we might still see a currency devaluation, this won’t necessarily hinder progress. More importantly, under Macri the country must normalise relations with the capital markets and start attracting the all-important foreign investors.”

The prospects of real change are undoubtedly stronger than they have been for 15 years, but don’t hold your breath – Argentina has a long history of disappointing, and outsiders have an equally long record of misreading the runes.

“With Macri’s reforms Argentina could probably return to growth of somewhere between 3% and 3.5% over the medium term – but of course that comes with the caveat that there is going to be short-term pain that may push the economy into recession next year as a result of tighter monetary and fiscal policy,” said Glossop of Capital Economics.

“So … the financial markets might be getting a bit carried away in terms of how quickly the adjustments might bear fruit.”

To see the digital version of the IFR Americas Review of the Year, please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@tr.com .