Turkey’s IPO market has never lived up to its potential. Official moves to get more companies listed and instill an equity culture face many difficulties. But bankers are confident that a new crop of IPO candidates could bring the market to life, despite the problems facing equity markets around the world. Nick Lord reports.

On May 6 and 7, over 2000 corporate executives, brokers, auditors and other assorted service providers met to discuss why so few Turkish companies sought a public listing. The IPO Turkey Campaign – Istanbul Summit, organised by the Istanbul Stock exchange, had three aims: to find suitable candidates for listing, to address the hurdles they faced in going public and to emphasise that having a deep public equity market was a crucial component of national economic growth.

Speaking at the event, Huseyin Erkan, chairman and CEO of the ISE was explicit: “Going public and trading on the ISE is essential for the companies to have continued access to the funds they need for growth and for ensuring sustainability,” he said. “Numerous Turkish companies fail to make sufficient use of such opportunities because they are not traded on the ISE. I am sure that prominent Turkish companies will become global companies if they have sufficient access to the opportunities offered by the capital markets.”

That Turkey lacks an equity culture is self evident. The size of the listed equity market is small, making up just 37% of GDP, compared to over 90% for most developed markets. Moreover, the biggest companies in the country are the family owned conglomerates such as Koc Holdings and Sabanci Holdings. Of the 30 stocks that make up the main ISE Index, 15 are family companies.

These companies are structured in the classic emerging market conglomerate waterfall: ultimate control is retained by the family, who through a holding company structure then control a range of subsidiaries in a variety of sectors. There are some minority listings of subsidiaries or even the holding company, but these listings are not meaningful, either in terms of the size of the public share, nor the control that they give public investors.

Over the past five years other large companies have come onto the exchange, but these have largely been secondary privatisations of government owned entities such as Turk Telecom or Turkish Airlines. In 2008 and 2009, during the crisis, new issue activity ground to a halt. But 2010 has seen a remarkable comeback, with eleven companies applying for a listing since the beginning of the year and two starting to trade. Economy Minister Ali Babacan said at the conference that he expects up to 40 new companies to seek a listing by the end of the year, which would be the highest number since 1988.

“In 2009 there was very little equity capital market activity in Turkey,” said Ugur Bayar, CEO of Credit Suisse in Turkey. “But in 2010 there has already been an unprecedented level of activity.”

Deals Scrape Through

The first deal to successfully list this year was Koza Gold which raised TL576m (US$378.5m) in April from the sale of 33% of the company at a price of TL36.80 per 100 shares. The deal was lead by Goldman Sachs and JPMorgan for the international tranche and Akbank and Isbank for the domestic tranche.

The deal did have some trouble getting away, coming as it did during a period of market turbulence. It priced at the bottom of the range of TLK36.80-TL46. The shares opened at TL33.25 and then ended the first day’s trading at TL34.75.

The company itself is a gold mining concession that is owned by the Ipek family. The equity story sought to capture both the historical preference that domestic investors have for gold with the rise in the present day price of the metal. It also emphasised how investors are looking for alternative ways to play gold without buying the physical commodity.

Since Koza Gold listed, the market is closely watching the travails of two large companies that are seeking to list: Aksa Energy and Akfen Holding. Aksa Enerji is one of the largest independent power producers in Turkey and is part of the Kazanci Holding conglomerate. It plans to sell 13.5% of the company (15.5% with Greenshoe) in a deal that will bring in TL619m, if it prices at the top of the range of TL4.9-TL7.2 per share. Bookbuilding for the deal closes on May 14 and 70% of the transaction is allocated to foreign investors.

Aksa is watching with some trepidation as the global downturn in the IPO market has reached Turkey’s shores. In particular the experience of Akfen Holdings, a construction company, will cause some consternation. It tried to sell 29% of the company through an IPO that could have raised up to US$700m. However it tried to build its book during the week of May 1-8, when the Greek contagion fears were at their height. A number of European IPOs either had to be shelved or needed price or size cuts to get them finished. On Monday May 10, Akfen announced that it was cutting the size of its IPO to just 7% of the company’s share capital and that it would be priced at the bottom of its TLK12.5 to TL17.5 price range.

The lesson is that while the big picture for the IPO market looks rosy, short term market turbulence plays havoc with the IPO process. “The fact is that the macro picture in Turkey is quite constructive for IPOs from the region, but issuance obviously to some extent remains hostage to the overall markets,” said Nick Williams head of EMEA ECM at Credit Suisse in London. “Deals in play always need to navigate what is going on in the wider market.”

Another potentially large deal that is used to dealing with turbulence of a different sort is Pegasus Airlines. This is a private sector airline that operates out of Istanbul’s second airport, flying to domestic holiday destinations within Turkey and to major European markets such as Germany and the UK. The company has appointed Credit Suisse and Is Yatirim to undertake its IPO in the second half of 2010. It has yet to formally apply for a listing on the ISE.

New Companies

What these new listings all show is that there has been a subtle shift in the types of companies that are listing. On the energy side, companies such as Aksa Energy have been set up to take advantage of the government’s energy privatisation plans. This process will take four to five years and will see the government sell off all of Turkey’s generation and distribution assets. In the past, the government would have been content to maybe just list the companies themselves. While this is on the cards for the generation assets (see Privatisation article), it is likely that it will undertake a blended process where it sells some assets directly to the private sector while also potentially listing companies as well.

For the private sector to buy the assets, a range of financing options are needed, from local bank funding to international credit to domestic equity. Aksa Energy and others are therefore seeking IPOs in order to be able to bid for the auctions of these assets. Indeed Aksa Energy was the winning bidder for two distribution grids sold by the government in February this year.

Away from the energy sector, financial services will also play a role, although less in the pure IPO market and more in the secondary public offering (SPO market). Halk Bank is likely to have some form of public offering at some stage this year while fully state owned Ziraat Bank is also a listing candidate although most observers believe this will not happen until next year.

On the private equity side there is only one real IPO candidate of any note. Supermarket chain Migros was bought from Koc Holdings by BC Partners and Cinven in 2008 for US$3.15bn. The acquisition has been a success according to bankers close to the transaction and at some stage the private equity firms will be looking for an exit. But any decision on a possible IPO is understood to be at least a year away with a likely IPO at some stage after 2012.

One final sector that is garnering interest and which will see a number of deals before the end of the year is the Real Estate Investment Trust (REITS) market. Two REITS have applied for a listing so far this year: TSKB REIT applied in February while Idealist REIT applied in April. TSKB plans to raise TL50m through the sale of up to 57.5% of the company. Idealist has applied to sell 25% to raise a rather meagre TL2.5m. Other deals are understood to be in the pipeline.

This all means Turkey’s IPO market is either on the verge of a transformational new beginning or that official efforts to help it come to life will founder on the rocks of global market volatility. There is no doubt that the official agencies are keen to get more companies listed. At the IPO Summit, a panoply of the great and good from Turkey’s economic and financial polity all took turns extolling the need to expand the IPO market. Representatives from the Capital Markets Board of Turkey (CMB), the Union of Chambers and Commodity Exchanges of Turkey, and the Association of Capital Market Intermediary Institutions of Turkey, all gave their endorsement to the plans.

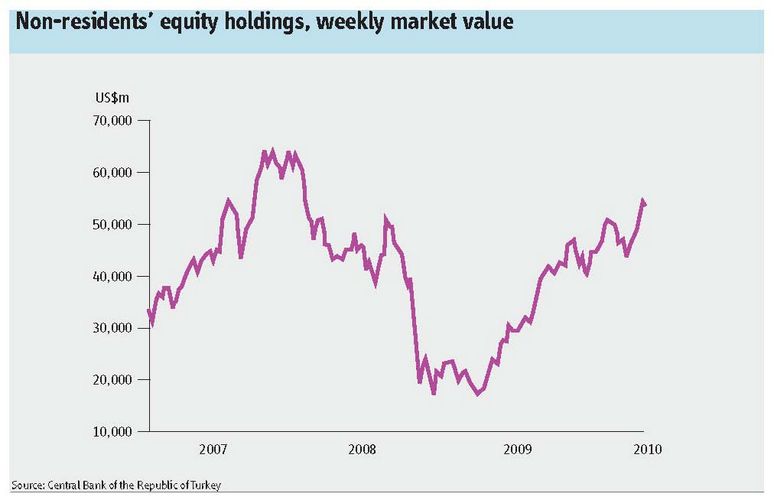

Given the response of the delegates to the conference there is no shortage of potential listing candidates. However most of the companies that are planning on listing are too small to garner investor attention, especially international investor attention. And given that foreign investors already own 70% of the stocks listed on the ISE and that most IPOs revert to about 95% foreign ownership after three months of listing, the size of companies does matter.

“If you look at ECM activity in Turkey, historically it has been relatively lumpy,” said Williams at Credit Suisse. “There are not that many deals above US$100m. Looking forward the potential privatisation pipeline of jumbo deals is however substantial.”

The small deals that have applied for a listing include the TL8 million listing of 50% of Latek Logistic, a transportation company; the TL3.4 million listing of 33% of Mango Gida, a fresh produce company; and the TL26.4 million listing of 33% of Ihlas Gazetesi, a newpaper and magazine publisher.

While these deals and this pipeline are important, they are not enough to be the catalyst that the market truly needs. That can only truly come when the large family companies decide to focus on a limited number of sectors and thus sell off companies in sectors they no longer want exposure to. There is very little sign of that happening.

In the meantime, changes do need to be made to the listing rules which leave companies and their advisers wholly exposed to weeks if not months of market risk. Companies are obliged to say how many shares they are selling and the price range when they apply for a listing. It then takes usually at least two months before the actual sale goes through. In this time conditions change but the system is inflexible: if the size or price has to change, then documents need to be refilled. In the case of Koza Gold, the deal only managed to get through because the selling family actually bought 13% of the deal themselves. This situation perhaps best encapsulates the dilemma facing the IPO market: the families need to be willing sellers, but they are also the only buyers. For the market to really take off the local institutional investor base has to develop significantly (see box).

| Turkish IPO pipeline | |||

| Company | Sector | Paid in capital (US$m) | IPO ratio (%) |

| Mango Gida Sanayi ve Ticaret | Food | 4.29 | 34 |

| BIS Enerji Elektrik Üretim | Energy | 13 | 34.5 |

| Aksa Enerji Üretim | Energy | 430.3 | 16.92 |

| Akfen Holding | Conglomerate | 86.45 | 29.2 |

| Ihlas Gazetecilik | Media | 52 | 33 |

| Çemas Döküm Sanayi | Heavy manufacturing | 15.11 | 35.48 |

| Idealist Real Estate Investment Fund | Real Estate | 6.5 | 25 |

| Euro Yatirim Menkul Degerler | Financial services | 13 | 25 |

| Gedik Yatirim Menkul Degerler | Financial services | 23.4 | 25 |

| Anel Elektrik Proje Taahhüt ve Ticaret | Energy | 29.9 | 34.33 |

| Source: Istanbul Stock Exchange | |||

| Turkey's pension system | |||||

| No. of contracts | No. of participants | Total amount of contributions (TLbn) | Total invested amount (TLbn) | Total amount of participant's funds (TLbn) | |

| 04/01/2010 | 2,207,126 | 1,990,623 | 7.1 | 6.89 | 9.12 |

| 02/01/2009 | 1,935,824 | 1,747,086 | 5.47 | 5.29 | 6.4 |

| 07/01/2008 | 1,583,117 | 1,464,008 | 3.95 | 3.82 | 4.59 |

| 08/01/2007 | 1,149,413 | 1,079,289 | 2.62 | 2.54 | 2.85 |

| 02/01/2006 | 715,766 | 675,864 | 0.94 | 0.2 | 1.1 |

| Source: EMG | |||||