Despite lacklustre demand for banking services over recent years, a number of foreign banks are pushing into Germany, keen to grab market share. With incumbents unlikely to give up easily, the industry is set for an intense battle.

German banks should be in a sweet spot right now: funding costs are at an all-time low, and the home market – the world’s third largest economy – is growing at a decent clip; demand for exports has pushed the trade surplus to a record high, helping generate jobs and push unemployment to the lowest since reunification; consumers are spending again, and the property market in many of the country’s biggest cities is booming.

But, despite the strong macroeconomic backdrop, and almost eight years on since the global financial crisis, much of the German banking system is struggling. Consolidation, predicted for many years, has been underwhelming. Almost 1,800 banks – more than double the number in any other eurozone country – are still locked in competition for a slice of the same lending, advisory or underwriting business.

The result has been thin margins and disappointing profitability: return-on-equity at German banks has averaged around 6% over the past few years, according to Bundesbank figures, even as the country’s economic engine has hummed along nicely. The last few years in particular have been painful – current annual profits of around €35bn are down almost a fifth since 2010, and are now down to levels seen in the late 1990s.

“This is the strongest economy in Europe, yet its banking system has an antiquated look,” said Sam Theodore, a managing director and team leader for financial institutions coverage at ratings upstart Scope. “The country still has too many banks and profitability is very low, a problem that is more acute that ever before because of the low-rate environment.”

According to Theodore, the German banking system’s resilience has in some ways been its biggest enemy.

“Other banking systems have been through consolidation and reform – normally as a result of crises – but Germany’s banks did not experience a major crisis, therefore there has been no real incentive to reform,” he said. “Added to that, there is a lot of political interest in maintaining the status quo, especially on the public banking side.”

Low demand

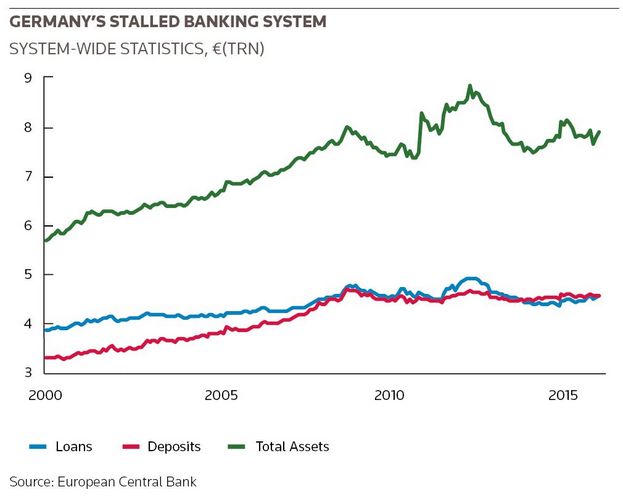

But poor returns are not only due to overcapacity; demand for banks’ products – and in particular loans – has also been weak over the past few years. The German economy has grown by 23% in absolute terms since the 2009 post-crisis nadir. By contrast, the amount of credit extended by German banks has flat-lined at around €4.6trn for much of those six years. Economic growth has just not translated into increased credit demand.

Subdued appetite for loans during times of economic growth is all the more surprising given the fact that the cost of borrowing has plummeted during that time. The European Central Bank has cut interest rates to zero and deposit rates into negative territory, while also launching numerous liquidity injections that have flooded banks with cheap funding. Rates charged on loans have come down to record lows.

“Germany is a mature market, but it is a very conservative and risk-averse market,” said Jan Schildbach, team head for banking, financial markets, regulation at Deutsche Bank in Frankfurt. “Even with the most favourable conditions you could ever get, companies are reluctant to borrow and invest. And on the retail side, conservatism prevails too: loan-to-value ratios are usually low, and most mortgages are fixed-rate.”

In bond markets, while other eurozone corporates have been enjoying the party, issuing heavily into a market where demand has been high and yields low, German corporates have been more cautious. Outstanding eurozone corporate bonds stocks have grown by around 40% to €1.1trn since 2010, but the German component has remained relatively flat during that time, rising only marginally to €258bn from €251bn.

“Corporates have been using up their cash buffers rather than borrow, and that’s a trend that is only likely to intensify as the impact of negative rates feeds through,” said Roman Schmidt, head of corporate finance at Commerzbank, Germany’s second largest bank. “There is also the general attitude that the bond market will always be there for established companies; there is no real urgency to tap markets now.”

Cutting back

Low returns have forced the German banking system to respond. Though consolidation has underwhelmed, the number of banks operating in the country has dropped by 200 since the financial crisis. Others are taking more drastic measures: Deutsche Bank, which completed the takeover of retail lender Postbank only in 2010, has said it now wants to sell the franchise; UniCredit-owned Hypovereinsbank, meanwhile, is cutting back.

“The only real response has been to cut costs, it’s the quasi-automatic management reaction to a decline in revenues in order to maintain margins and returns,” said Theodore, who cautioned that might not be enough. “There is only so far you can go unless you reduce capacity too, and with that you risk losing market share. There is much more inertia in the public sector – for them, breakeven is more than enough.”

Still, despite the overcapacity, low returns and subdued demand for credit, foreign banks are eyeing the German market as an area of expansion. Bundesbank statistics show the number of foreign banks operating in the country has grown by 15 to 107 since the crisis. Some of Europe’s biggest banks such as BNP Paribas, Societe Generale and HSBC point to Germany as a key country where they want to expand over coming years.

Of course, the German banking sector is no stranger to foreign banks seeking to grab a piece of the market. In the years leading up to the crisis, banks such as RBS and Citigroup made big inroads. When the global financial crisis hit, they and many other foreign banks retreated, cutting staff and balance sheet in Germany in order to concentrate on their home markets.

Ironically, one of the elements of the German banking system that made operating there so difficult – the excess of deposits over credit demand – is one of the elements that has made the market so attractive to some foreign banks. For European banks that found it difficult to fund themselves in capital markets as the European sovereign debt crisis took hold in 2010 and 2011, German deposits suddenly looked like an alternative source of funds.

“Many foreign banks started to retreat out of Germany as a result of the global financial crisis, as they sought to refocus on their core markets,” said Schildbach. “But the euro sovereign debt crisis reversed that trend, and many European banks started to see Germany as a source of deposit funding.”

Spanish bank Santander and the two French banks BNP Paribas and Societe Generale all expanded in Germany as the crisis took hold.

Grabbing fees

But deposit-taking alone is not a valid business model, and foreign banks since then have been picking their spots. One particular area of focus has been the investment banking market: BNP Paribas announced plans hire more than 500 people in its corporate and institutional banking business in a bid to boost revenues by winning more business from the country’s huge corporate base. Societe Generale, likewise, is targeting similar clients and is hoping for annual growth rates there of up to 10%.

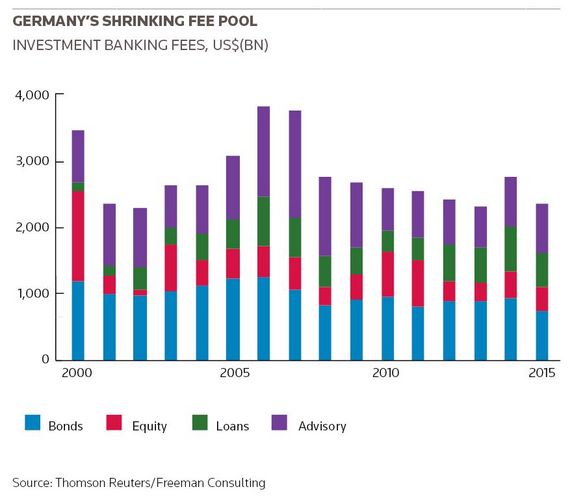

The allure of grabbing more fees from bond, equity and loan underwriting, as well as advisory work, is clear: German companies pay out around US$2.4bn in fees every year. And European banks in particular see potential to earn more of the fee pool in a country where they have traditionally punched below their weight. US and German investment banks typically dominate. Last year, they took the top six spots in terms of fees earned.

According to BNP Paribas, its strategy is already paying off. Ambitious plans for cumulative annual growth rates of 8% in the first three years of its push, which began in 2013, are set to be achieved. What is more, it sees further upside.

“This economy still offers ample opportunities to further growth,” said Camille Fohl, chairman of the group management board for Germany at the French bank. “Despite our good development in Germany, we still have upward potential in all areas – and we work hard. We have strongly increased our corporate franchise, now at 450 corporate clients in Germany and also more than 2,500 affiliates of international groups operating in Germany.”

German incumbents caution that foreign firms will have their work cut out in grabbing more market share.

“Germany is, on paper, a very good market to be in: it is the highest fee-paying market in Europe, there’s a huge number of Mittelstand firms looking for capital market products, the economy is strong,” said Commerzbank’s Schmidt. “But it is a difficult market to crack: it is a competitive market, and existing relationships are very strong.”

What is more, investment banking fees – much like lending – have been in a funk over the past few years. According to Thomson Reuters data, the total fee pool has been coming down ever since the crisis as debt underwriting and equity underwriting activity in particular have dried up. Although corporate lending fees and advisory income have held up during that time, the shrunken overall fee pool means competition is more intense – and the home names are putting up a fight.

Fight-back

Indeed, Commerzbank’s Schmidt believes that domestic players, many of which have been operating in the market and servicing corporate clients there for many decades, are best placed to pick up market share because of their long-standing relationships. After years of cutting back, Commerzbank is once again in growth mode and keen to recapture some of the market share it lost to rivals in recent years. According to Thomson Reuters data, last year it ranked sixth in the fee league tables with a 4.8% market share – behind Deutsche Bank, JP Morgan, Goldman Sachs, Bank of America Merrill Lynch and Citigroup.

Schmidt now runs a merged corporate finance and client relationship business that aims to pursue growth under the umbrella of eight industry verticals. The idea within those verticals is to capture investment banking business through the entire supply chain

“There are number of banks all competing for the same business. But having been part of the market for a long time has huge advantages – we have good long-standing relationships,” said Schmidt. “Those kinds of relationships are difficult to build, not everyone has the patience.”

Foreign banks will put up a fight. Many are hoping to bring new products to a deeply conservative corporate base. That should in turn increase the total fee pool.

“One important pillar of our presence in Germany, and of the business model of BNP Paribas, is to broaden the scope of products and services offered to our targeted customer groups by making our various business lines work together … with the customer,” said Fohl. “I think that in this approach, we can definitely set ourselves apart from other competitors. We don’t pursue a ‘me too’ strategy.

To see the digital version of this special report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com