HDFC’s landmark offshore rupee issue finally unlocked the Masala bond market in July, but familiar concerns over pricing, liquidity and regulation threaten to cast a shadow over its long-term development.

After years of growing pains, efforts to globalise India’s bond markets are finally bearing fruit.

The Masala bond market, where borrowers issue bonds in offshore rupees and settle them in US dollars, received a shot in the arm in July from a landmark debut Rs30bn (US$448m) three-year and one month offering from Housing Development Finance Corporation.

HDFC, the country’s leading provider of finance for housing, ended more than a year of anticipation when it priced the first corporate Masala bond.

The result proved that an offshore market exists for homegrown rupee issues, assuaging doubts that Masalas would struggle to develop beyond issues from supranationals such as the International Finance Corporation and the Asian Development Bank.

The hope is that this new funding channel will provide Indian companies with greater access to funds, especially as mounting debt at state banks and lack of depth in onshore bond markets hobble funding for the infrastructure and energy projects needed to fuel economic growth.

Furthermore, Masalas could potentially lower the cost of capital in India, which is among Asia’s highest.

The development is also as a small step towards full convertibility of the Indian rupee, one of the objectives that former Reserve Bank of India Governor Raghuram Rajan set during his tenure from 2013 to 2016.

“The Masala market has gotten off to a promising start, spanning transactions in the investment grade as well as sub-IG space, across public deals and private placements. That said, for the market to deepen into a more permanent and stable source of funding for Indian issuers, we need to see a wider base of investors”

However, these benefits, which would further integrate India’s financial markets into the global economy, are still distant due to a host of problems that the Masala market needs to address.

Issues range from a lack of liquidity, which has dogged investors who bought HDFC’s offshore rupee debut, to complex regulations. Unless they are resolved, Indian issuers that can access the far larger global US dollar market are unlikely to find the Masala format an attractive alternative.

Testing the waters

Masala issuance drastically picked up after HDFC’s debut, following a loosening of rules announced by the Reserve Bank of India in April that included a reduction in the minimum tenor to three years, as opposed to the five years previously.

The changes brought Masalas in line with regulations on the maturities of corporate bonds in which foreigners can invest under the Foreign Portfolio Investment route.

The maximum amount an issuer can sell in a single financial year under the automatic approval route now stands at Rs50bn (US$749m). Previously, the limit was set at US$750m and was expressed in US dollars.

One of the biggest issues with the Masala bond market is the mismatch in the yields that issuers are willing to pay and investors willing to accept.

Masalas are subject to a 5% withholding tax, which the issuer, typically, absorbs in international offerings.

The tax adds to the cost for Indian Masala issuers and makes the bonds more expensive relative to the domestic market. As a result, some potential corporate issuers are waiting for clarification of the applicable tax rules.

The Finance Ministry is looking at easing the withholding tax rules, but has not issued a ruling yet.

Despite the challenges, some Indian companies see the format as a way of lifting their international profile.

“There is a lot of buzz. It has not created fantastic interest,” Ajit Mittal, executive director for Indiabulls Housing Finance, told IFR during a recent Masala bond conference.

“The chief motivation was to tap a global pool of capital and take recourse to diversified funds. It is not the most cost efficient, but [it helps] establish at least our footprint.”

A handful of previous Masala issues have been able to circumvent this problem.

The prospect of buying a Green Masala from India’s largest power company NTPC prompted environmentally conscious European investors to flock to the offering in August, allowing it to price at the tight end of guidance, or inside NTPC’s onshore curve and 20bp inside the Reuters AAA five-year benchmark for Indian government bonds.

However, this kind of pricing competitiveness will only be available to quasi-sovereign names that are highly sought after by international investors, or issuers that able to access a specific type of investor base by using bond proceeds for special situations like green funding.

Sweetening the deal

If issuers are able to bring down pricing in Masalas, another problem they face is that investors who are able to buy Indian domestic bonds have little incentive to buy these offshore rupee notes.

On the face of it, there is no reason for Masala bonds to work. Any foreign investor who wants to buy rupee bonds can obtain a quota and pick from a much larger, more liquid universe of credits onshore.

Fortunately, bankers were able to find ways around this. They were able to structure the overseas rupee-denominated debt into derivatives, and then sweeten the deal with leveraged returns of 12%–13% after fees and hedging.

For example, banks like Credit Suisse and Nomura were able to turn debt from HDFC and Adani Transmission into credit-linked notes, according to several sources involved in the sales. A bank would provide about 80% of the funding, leaving the investor to pay for the rest to buy the derivative. After paying for the dollar funding rate of about 1.5%, a bank fee of 50bp, and short-term rupee hedging, the eventual landed return for the investor comes to 12%–13%, thanks to the heavy leverage ratio.

The return is much higher than the nominal 8% or so offered by unleveraged Masala bonds and the highest for similarly-rated debt, bankers say.

The problem is that the derivatives will not suit all investors, particularly those that are more risk-averse.

Any sudden plunge in the rupee, or a sudden fall in value of the Masala bonds underlying the derivatives, could wipe out returns.

Liquidity

It is understandable that liquidity would be an issue for this nascent market, but market participants are expressing concerns, as was the case after HDFC’s offering.

HDFC’s bonds were trading 20bp tighter the day after pricing, but the initial activity had dried up since. One investor complained that there were no meaningful two-way quotes available for HDFC, a big contrast to the liquidity available from US dollar bonds issued by Indian borrowers.

A large part of HDFC’s Masala bonds went to private-banking clients, mostly high-net-worth individuals, who, typically, hold bonds to maturity.

At a time when global volatility has prompted investors to flock to the most liquid credits, the lack of liquidity could continue to weigh on the Masala market’s ability to attract foreign buyers.

For now, foreign investors have resorted to ask for higher premiums to compensate for this.

“Onshore, there is better liquidity and better pricing,” said Gregor Carle, managing director at BlackRock. “[In the] longer term we want to see strategic initiatives to grow this market.”

A better future

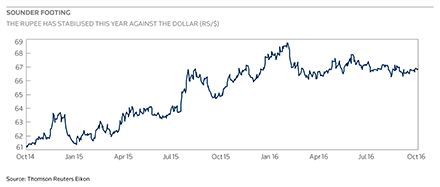

The timing of the development of the offshore rupee bond market coincides with strong global demand for Indian paper, as the rupee offers higher yields than assets in many other regional emerging markets.

There’s also a major pool of money that could easily find a home in Masalas – some US$32bn in foreign currency non-residential deposits are due to mature by this autumn.

“The Masala market has gotten off to a promising start, spanning transactions in the investment grade as well as sub-IG space, across public deals and private placements. That said, for the market to deepen into a more permanent and stable source of funding for Indian issuers, we need to see a wider base of investors participating in the secondary market. Any change in allowing offshore branches of Indian banks to engage in the market, will certainly help in achieving this,” said Chetan Joshi, head of debt capital markets at HSBC India.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@tr.com

| MAIDEN MASALAS | |||||

|---|---|---|---|---|---|

| Offshore rupee bond issues from India’s corporate sector | |||||

| Issue date | Issuer | Coupon (%) | Proceeds (Rs bn) | Maturity | All Managers |

| 19/07/2016 | Housing Development Finance | 7.875 | 29.8 | 21/08/2019 | Credit Suisse, Axis, Nomura |

| 03/08/2016 | NTPC | 7.375 | 19.9 | 10/08/2021 | HSBC, Axis, Mitsubishi UFJ, Standard Chartered |

| 01/09/2016 | Housing Development Finance | 7 | 5 | 09/01/2020 | HSBC |

| 02/09/2016 | Housing Development Finance | 7 | 10 | 09/01/2020 | HSBC, Standard Chartered |

| 15/09/2016 | Indiabulls Housing Finance | 8.567 | 13.3 | 15/10/2019 | Yes Bank, Axis, Bank of America Merrill Lynch, |

| Citigroup, Credit Suisse, Nomura | |||||

| 17/10/2016 | Housing Development Finance | 7 | 5 | 09/01/2020 | HSBC, Standard Chartered |

| 18/10/2016 | Fullerton India Credit Company | 8.125 | 5 | 18/11/2019 | Credit Suisse |

| Source: Thomson Reuters | |||||