The German Pfandbrief market, long the largest and most established of Europe’s covered bond markets, has consolidated its position through the sovereign crisis, when peripheral markets have closed down. But challenges remain, and it remains to be seen what form the post-crisis market will take, especially once regulatory changes have been finalised. David Rothnie reports.

Talk to a German banker about Pfandbriefe and it will soon be remarked that the market has failed to produce a single default in 200 years. It is a record of which the country is justifiably proud. And as the statistic hints, the benchmark of the covered bond market has suffered little in the way of controversy. When something does disturb the usually still waters of the Pfandbrief market, therefore, it is not surprising that it causes quite a stir.

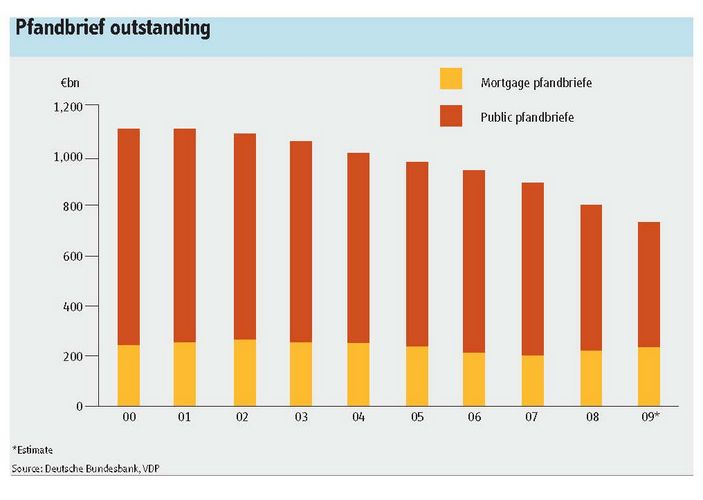

So it was when the Pfandbrief market’s supremacy was challenged by the rise of government guaranteed bonds and a general aversion to bank risk in the aftermath of the financial crisis. It survived in part due to its structural advantage. But it is a declining market in terms of outstanding issuance. From a high of more than €1trn in 2000, outstanding volumes have been dropping steadily, falling by 10.7% in 2009 to €719bn. They hit €730bn last year, and are projected to fall below €700bn by the end of the year. This was mainly attributable to net redemptions of Public Pfandbriefe, totalling approximately €93bn.

Primary sales do not compensate for large maturities in jumbo Pfandbriefe. Last year new issues totalled €52bn, compared to maturities of €145bn. The volume of Public Pfandbriefe outstanding fell as a result in 2009, from €579bn to €486bn. Maturities (€2.6bn) also exceeded new issues (€1.3bn) of Ship Pfandbriefe. Mortgage Pfandbriefe was the only class of the asset where new issues, which totalled €56.9bn, outweighed maturities, of €49.2bn.

Bernd Volk, European head of covered bond and agency research at Deutsche Bank, said: “Pfandbriefe are holding up incredibly well because a strong domestic demand and a decline in outstanding volumes mean the Pfandbrief market will continue to be strong.”

The sovereign debt crisis has hit new issuance hard. In January, Henning Rasche, president of the association of German Pfandbriefbanks (vdp) said in a speech that issuance would reach between €8bn and €10bn per month, resulting in an expected gross issuance total of €100bn in 2010. In the five months to the end of May, German corporate bond issuance had reached €16bn, well below the required run-rate to hit the vdp’s target, according to data from Thomson Reuters.

This continues a downward trend in the market. According to official Vdp data,

investment activity fell in all four areas of the Pfandbrief Banks’ lending operations that qualify as Pfandbrief cover. The volume of new loan commitments in 2009 came to € 139bn, 30% below the previous year’s level. By contrast, total real estate, public-sector, ship and aircraft loans showed very little change compared with end- 2008, rising 0.4% to €1.4trn.

Pfandbriefe with an aggregate volume of nearly €110bn were placed with investors, compared with €153bn in 2008.

New kid on the block

The biggest perceived threat to Pfandbriefe – as to all covered bonds – was the introduction of government-guaranteed bonds (GGBs), which flooded the market with low-risk liquidity. According to the Vdp, in its annual report, “the costs for government guarantees bonds and the positive development of spreads on the Pfandbrief market soon proved such fears to be unfounded. At no time did SoFFin (Federal Agency for Financial Market Stabilisation) bonds pose a serious threat to the Pfandbrief.”

This is a moot point, as Pfandbriefe have suffered at the hands of GGBs at the short end of the market. But the essence of the Pfandbrief is to provide longer-duration funding, noted one banker. In a tough market for covered bonds, Pfandbriefe have provided the sector’s only chink of light.

The Eurozone crisis shut the covered bond markets to issuers for almost a month. When dealflow resumed, it came from the Pfandbrief sector, albeit not in the jumbo space. In May, Deutsche Hypotheken tapped the market for a 5-year mortgage Pfandbrief, issued at mid swap +10bp, for €600m on May 17. Similarly, UniCredit sold a 7-year mortgage Pfandbrief (€500m) at mid swap +15bp.

“Some peripheral covered bonds were trading widely to Bunds as investors sought cover in high-grade German and French risk,” said Ted Lord, head of European covered bonds at Barclays Capital. “The likes of Heleba and Unicredit (HVB) took advantage of this need with successful Pfandbrief issues.”

These issues also underlined the status of Pfandbriefe as the benchmark for the covered bond market. It was the last covered bond market to suffer from the effects of crisis, and the quickest to recover.

“We see these transactions as a first step towards the reopening of the covered bond market,” said Jose Sarafana, head of European covered bond research at SG. “However, we will not see more widespread new issuance activity in the covered bond market until sovereign spreads and covered bond spreads stabilise.”

Pfandbriefe have benefited from this new wave of volatility sweeping through the sovereign bond markets, of which covered bonds are a surrogate. Prior to the financial crisis of 2008, spreads had tightened on covered bonds to the extent that qualitative differences were no longer visible. That is no longer the case. The divergence between covered bonds now reflects the risk perception in their country of provenance.

Until the beginning of the crisis, qualitative differences between covered bonds were barely visible. Spreads were generally tight spreads at that time, with virtually no credit differentiation. As a result of the crisis, and the widening of the spreads in its wake, investors’ perception of risk toward various covered bond products has be transformed.

A little help from its friends

Pfandbriefe have been a clear beneficiary of the European central bank’s Covered Bond Purchase Programme. The same has not helped peripheral markets because it handed responsibility for the purchase of covered bonds to a powerful group of central banks. The €60bn programme was allocated between the ECB itself (8%) and the national banks of the euro area in proportion of their participation in the ECB’s paid-up capital. The Deutsche Bundesbank had by far the biggest slug of capital, with 25% of the total.

“The political impetus from the covered bond programme came from the powerful central banks such as the Bundesbank,” one banker said. “This was a case of the strong becoming stronger.”

Shortly after the ECB’s programme was launched, the spread narrowing, which had already started, accelerated. By year-end 2009, Jumbo Public Pfandbriefe were yielding 9bp over swaps. Mortgage Pfandbriefe were yielding 12bp over swaps.

Some believe it was inappropriate to include such safe assets which did not need support in a guarantee scheme. However, as one of the safest funding avenues available to banks, covered bonds were identified as crucial to stabilising the banking systems and encouraging financial institutions to start lending again. Moreover, the Pfandbrief is the poster-child for the new era of securitisation. The strict requirements of the Pfandbrief Act demand first-class security and comprehensive protection for investors. Investors have a claim against the issuing bank, and in case of bankruptcy they have a priority claim to the collateral listed in the cover funds.

Aside from their inclusion in the ECB programme, the asset class was given extra protection from a German federal ruling that gave Pfandbrief investors recourse to the courts in the event of a default. Furthermore, the amendment of Germany’s Mortgage Bond Act takes into account the higher level of investment safety demanded by holders of such bonds.

Now the spectre of regulation has become the biggest threat to the Pfandbrief segment. Particularly worrisome for the market is what form the Basel 3 recommendations that are due later this year will take. The possible introduction of a hard leverage ratio under Basel 3 threatens to allow alien (non-risk-sensitive) elements into the supervisory framework for banks. As a binding ratio to be observed under supervisory requirements, it would hit Pfandbrief Banks especially hard, due to their extensive, safe and therefore low risk-weighted assets, deriving from property finance and public-sector loans.

“The imposition of a uniform hard leverage limit under Basel 3 would be disastrous for the business model of public Pfandbrief issuers,” concluded Volk. “However, we expect some exemption for public Pfandbrief issuers, either in Basel 3 directly or in the national implementation of Basel 3.”