It may have drawn criticism from those who view the growing commercialisation of microfinance as a threat to its true goal. But the wildly popular SKS Corp IPO clearly illustrates investors’ growing interest in microfinance. But the industry needs to mature in terms of governance, while investors need to get their heads around the challenge of conducting due diligence on small institutions, often operating in remote areas. Savita Iyer-Ahrestani reports.

The US$358m IPO issued in August by India’s SKS Corp attracted the biggest hitters in the financial world. Firms like Goldman Sachs and JP Morgan, as well as billionaires including George Soros and N.R. Narayanmurthy, founder of Indian IT giant Infosys, participated. It was one of the few microfinance-related IPOs to date, the last one being a US$400m deal issued four years ago by Mexico’s Banco Compartamos.

Priced at the top end of its range and 13 times oversubscribed, it illustrates how eager investors are for microfinance IPOs. “Everyone wants a little bit of microfinance and to be a part of the upside of the microfinance story,” Reille said.

More such deals are expected to follow, said Xavier Reille, independent policy and research center CGAP’s microfinance specialist, based in Paris. The deals will be marketed in coming months in those countries whose local markets are deep enough to support them.

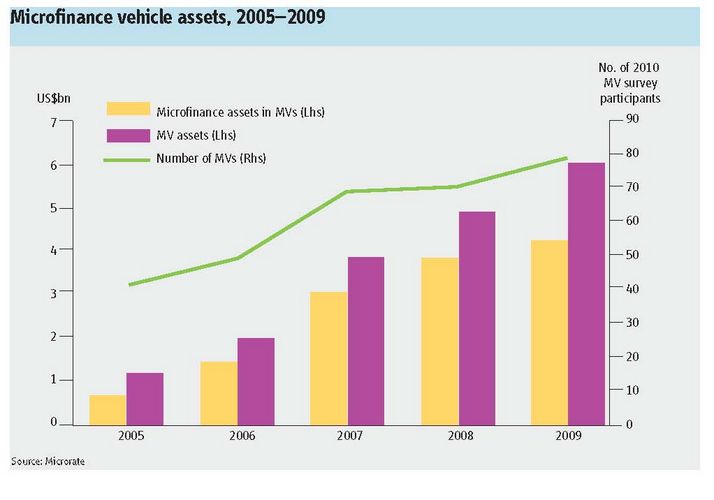

There’s no denying that microfinance is becoming a greater part of the mainstream financial world. The powerful impact microfinance has in improving the economic status of communities and individuals who are otherwise entirely detached from the financial markets and conventional banking has already been proven. The commercial viability of the sector continues to draw in a greater number of investors, many of them new to the business. The number of microfinance vehicles (MIVs) – hedge funds and mutual funds – has increased significantly, catering for the increasing number of institutional investors expressing an interest in the sector.

The appeal for institutional investors is simple enough. They are encouraged by the prospect of steadier returns with lower volatility in the aftermath of the financial crisis. Today, many microfinance institutions (MFI) around the world are sophisticated and profitable entities, capable of performing several functions beyond the extension of credit. In order to continue growing and expanding their services, and thereby reaching out to a greater number of customers, they need funding.

But while the attraction to and commercial viability of microfinance are no longer debated, challenges remain, with many coming to the fore now the industry is maturing.

Survival of the fittest

The MFIs that were not well managed, that had an unsustainable business model or were overleveraged have faced problems since the global financial crisis, said Ron Dadina, chief credit officer for Minlam Asset Management, a New York-based microfinance hedge fund. Overindetedness in certain pockets is a problem, he said. And fraud, governance and transparency issues have arisen at some MFIs, despite some steps being taken to encourage universal best practices.

Since the financial crisis, there has been a concerted effort by a range of institutions around the world to put in place global standards for best practices at MFIs. At the local level, most countries have taken steps to ensure proper governance within their jurisdictions. Now the move to put in universal codes of conduct for all MFIs has become a priority, and this will make it easier for investors to performance qualitative due diligence on MFIs.

The issue of proper governance in the microfinance sector has only really come to the fore after the crisis, in the same way it became more important for all investors. The extension of credit in the aftermath of the crisis has become more difficult for all market segments, and proper governance and due diligence has become a priority across the board.

Despite the various sovereign crises that have taken place over the past years and that have underscored the dangers of foreign currency borrowing, the microfinance industry still has no real way to contend with currency risk, although agencies like the Overseas Private Investment Corporation are providing tools and support in this area. Many MFIs have pushed the burden of borrowing in hard currency onto their clients, according to Dadina.

Many MFIs have also decreased their demand for foreign capital in the wake of the crisis, said Reille. They favour local market borrowing, meaning fewer opportunities for MIVs. Funding from overseas offers an MFI better terms, deeper liquidity and longer maturities. Yet local market funding is increasingly becoming the norm for MFIs, he said. This has squeezed out much of the foreign capital.

Local markets are far more reliable in the longer term because they are not subject to the vagaries of international finance and the issues of currency risk do not arise. However, only certain emerging market countries with a vibrant MFI sector – for example India, Mexico and Peru – have a local market that’s developed enough to support MFIs, or deep enough to capitalise them in a meaningful way. The depth and development of local markets is also dependent on local regulation: some governments have more measures in place to support local market development, and thereby local market funding. Others have more work to do in this area.

“We’re in a time where it’s harder for investors to place money because there’s less MFI growth and so there’s more supply than demand,” Reille said. “We have seen that in many places, local currency funding is available and this is competing with foreign currency funding.”

Micro. But not too micro

At the same time, a significant portion of MIV assets are currently being held in cash, rather than being deployed as investments in microfinance institutions. This has attracted criticism from some quarters. “You have nearly three billion people worldwide with limited access to financial services, yet much of the investable capital is on the sidelines and isn’t always reaching smaller, Tier Two MFIs,” said Bryan Wagner, who focuses on microfinance as part of Morgan Stanley’s global sustainable finance group.

Tier Two microfinance institutions are struggling to find capital, as fund managers have generally declined to invest in them. The difficulty presented by conducting proper due diligence across the spectrum of MFIs has discouraged some fund managers, while many others, particularly after the crisis, have preferred to go with the better known, more high profile MFIs in countries with stable economic and political regimes, Dadina said.

Institutions like Compartamos in Mexico, Germany’s ProCredit and SKS Corp in India, are extremely strong and well managed entities. They are profitable and commercially viable, and therefore have far greater investor appeal. Some firms, like Minlam, conduct rigorous macro credit and due diligence on all potential investments, do unearth opportunities among the smaller and underfunded MFIs around the world. However, many others do not, blocking the path for smaller MFIs to establish themselves.

Getting cash to these institutions has become a challenge, but it is surmountable if certain players in the market make a concerted effort to develop these Tier Two MFIs. Wagner believes multilateral agencies can help in this regard: “They have always been critical partners for the microfinance industry and, by developing the next layer, can create more opportunities to engage commercial capital as Tier Two MFIs become Tier One over time,” he said.

Private sector capital can also play a big role in this process. Investment banks like Morgan Stanley, which leverage their expertise in the conventional capital markets to serve the microfinance sector, will increasingly act as important intermediaries, Wagner added. They can connect institutional investors with MFIs and underwriting deals that are ultimately good for investors, MFIs and low-income communities. Earlier this year, for instance, Morgan Stanley was joint bookrunner with Bank of America Merrill Lynch on the first international bond issuance by a Latin American MFI, a US$200m deal placed by Mexico ’s Financiera Independencia.

There are likely to be more such transactions in the future, helping to strengthen MFIs at the local level and enabling them to provide an increasing breadth of financial services. This is the ultimate goal of microfinance. Today, a number of MFIs can take deposits, greatly enhancing their liquidity positions and allows them to diversify their business. The next step, said Bob Annibale, managing director and global head of Citi Microfinance, is to encourage more MFIs to start taking deposits, issuing local currency debt, securitising microfinance receivables and performing other kinds of transactions.

“Over the last few years, we have seen MFIs move increasingly toward local funding and support from local markets,” Annibale said, “This results in the convergence of banking services and microfinance services, which is the end goal of the sector.”