The process of restructuring Greece’s sovereign debt was, for the banking professionals involved, one of the most complicated they had ever experienced. The fact that it was accomplished in nine months was, perhaps, a minor miracle. Here, IFR examines how the deal made it over the line.

To see the full digital edition of the IFR Review of the Year, please <a onclick="window.open(this.href);return false;" onkeypress="window.open(this.href);return false;" href="http://edition.pagesuite-professional.co.uk//launch.aspx?eid=24f9e7f4-9d79-4e69-a475-1a3b43fb8580">click here</a>.

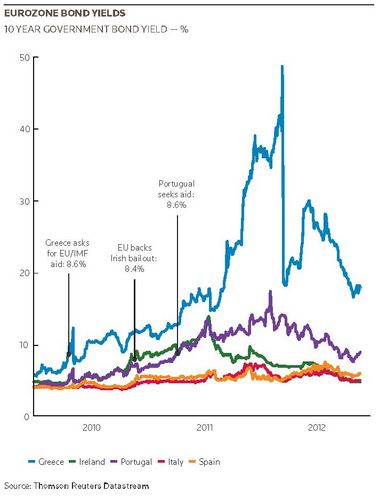

The restructuring of Greece’s €206bn of private sector debt in March – the first by a Western European nation for over 60 years – was a landmark without parallel.

In one respect the deal was an outstanding success – with 96% of the eligible bonds exchanged for a range of new instruments with a face value of 46.5% of the old notes. That made the deal the largest ever sovereign restructuring, and with one of the highest ever take-ups by investors.

The steep haircut, around 75% on a net present value basis, was astounding, particularly as restructuring had been entirely ruled out when Greece first sought assistance after losing market access two years earlier.

As Greece was also a member of Europe’s single currency this aversion to a haircut was understandable. A default would hit the 16 other members of the bloc as well. Would Greece have to leave the euro? Or could it manage its financial predicament within the eurozone? The answers to those questions would set a precedent for other ailing countries.

A default also seemed unthinkable for Greece’s largest creditors, principally eurozone financial institutions led by France’s BNP Paribas and Germany’s Deutsche Bank. Banks were, after all, still fragile after the financial storm that followed the failure of Lehman Brothers in September 2008.

So the fact that two years after it lost market access, Greece had managed to get its private sector creditors to accept an estimated 75% reduction in the accounting value of their €206bn holdings, without bringing them or the euro down at the same time, was a major achievement.

“Before PSI [the private sector involvement deal], Greece on one hand and the European financial system on the other were in intensive care with tubes and wires linking each other,” said Andres de la Cruz, partner at law firm Cleary Gottlieb, which advised Greece on the situation.

“Afterwards Greece and the financial system have been moved into two separate intensive care units. They are no longer connected. PSI did not solve the problems but now each problem can be tackled separately.”

Franco-German axis

Initially, Europe’s diagnosis was that Greece’s predicament was a temporary loss of liquidity rather than a permanent lack of solvency. Banks, led by BNP and Deutsche argued that to admit the possibility of the latter would throw into doubt the whole basis of European finance.

Up to that point, eurozone government bonds had been considered essentially risk-free. Undermine that assumption, the banks said, and questions might be asked about other European sovereign bonds and the health of banks as major holders of such instruments.

Both BNP and Deutsche, with their significant exposure to Greece, lobbied their respective governments to ensure this point was not lost on them. And initially at least the politicians accepted that argument, leading to a €110bn bailout loan provided to Greece in May 2010.

By the spring of 2011, however, it had become obvious to all that the bailout would have to be reworked. BNP remained keen to preserve at least the illusion that European sovereign bonds were risk-free and proposed a plan to extend the maturity of all Greek bonds for between 30 and 50 years.

“In return Greece would agree to spend €30bn buying Triple A zero coupon bonds such as OATs or Bunds to enhance the credit quality of the lengthened bonds and ensure the risk-free status would be retained,” said Christopher Drennen, a public debt expert at BNP who worked on the plan.

Such an initiative would be massively destructive of a bond’s net present value. But the bank argued that most investors had bought the bonds at issue to hold a risk-free asset to maturity as part of their regulatory capital requirements. They would have rolled over the bonds normally in any case and simply wanted to ensure they did not take a loss in face value terms.

But with Deutsche taking a slightly different view (it had inherited most of its holdings of Greek paper from its purchase of Deutsche Postbank and accounted for them differently as a result), the German position began to change. In early June the country’s veteran finance minister Wolfgang Schaeuble urged his peers to accept that “any additional financial support for Greece has to involve a fair burden-sharing between taxpayers and private investors”.

That tacit call for restructuring upset the French in particular and sparked a wave of frantic negotiations over the next month. “There was a different assessment by the banks and governments of Germany and France,” said one public sector official.

Another round of negotiations, mainly in Brussels, Paris and Rome now took place in late June and early July.

Rome had cropped up as a key venue because the director general of the Italian Treasury, Vittorio Grilli, was chairing the economic and financial committee of the Eurogroup of finance ministers from the eurozone countries. This taskforce had emerged as the key place to discuss the Greek question ahead of Eurogroup summits that would finalise the plans.

At the third meeting at the Italian treasury in Rome ending on Friday, July 15, six days before a full summit of Eurogroup leaders on July 20, late in the evening Grilli told the group he had reached an impasse.

As well as delegates from the ECB, IMF, EFSF, European Commission and French treasury a number of key creditors were also present: Chris Drennen together with Jean Lemierre, a senior BNP adviser; Hakan Wohlin, global head of debt origination at Deutsche, and Charlotte Jones, Deutsche’s chief financial officer for EMEA; Allianz’s finance director Paul Achleitner and the IIF’s chief executive Charles Dallara.

HSBC was involved in the background too: liability management specialist Andrew Montgomery was running spreadsheets on the various options proposed.

“Grilli clearly could not go any further without political say-so from a very senior level,” said one person who was in the room. “He said he would come back the next day with a plan.” After some late night calls to Berlin, initiated by creditors, Merkel gave her support to a fresh proposal which ended up being adopted the following week at the Eurogroup summit on July 21.

“The deal was brokered in Rome,” said Petros Christodoulou, head of Greece’s public debt management agency att he time, who was also present. “Grilli had taken a lead role. There were insurance companies there and banks but two or three banks were leading discussions.”

However, the final deal was agreed, after a series of shuttle diplomacy over the following week in Brussels. “The agreement was made between Merkel, Sarkozy and Trichet in the middle of the night,” said one adviser.

“This was a crisis summit,” said Gerassimos Thomas, a senior official of the European Commission involed in the Greek bailout.

He pointed out that EU leaders normally meet twice a year in June and December. “We went from there being no restructuring tolerated whatsoever in the eurozone to Greece being the unique and exceptional example.”

As part of a second €130bn bailout, Greece would be the first Western European country for over 60 years to restructure its debt – and would do it via a “voluntary” negotiation with its creditors.

“We came into the room with the menu on the table and simply had to go and cook”

Most involved agreed that the agreement was far from consensual. “It was an agreement imposed to protect Europe from the contagion which had started to crop up. The idea was that if we do this it will protect against other problems,” said one creditor.

Implementing the deal

Once that historic step had been taken, the focus moved to implementing the deal. Private sector creditors, under huge pressure from European governments, had conceded an effective 21% haircut on their holdings.

At first, it seemed Greece had very little influence on events. The creditors, under the aegis of the Institute of International Finance, chaired by Deutsche’s chief executive Josef Ackermann, had even outlined four options that its members could choose between.

“We came into the room with the menu on the table and simply had to go and cook,” said de la Cruz at Cleary Gottlieb, whom Greece engaged to advise on the restructuring.

However, the next month proved particularly fragile for the markets. On July 26, Deutsche became the first bank to publicly mark down its Greek bonds by 21%. Yields on Italian and Spanish bonds started to rise significantly as investors realised risks had been heightened. The European Central Bank intervened, buying bonds in an effort to quell the growing nervousness.

Against this backdrop the first PSI plan started to come unstuck.

“[The initial plan] was based on the Brady idea of persuading creditors by giving them collateral. Greece would have had to buy it from the EFSF in the form of a 30-year zero [coupon bond],” said Philip Wood, partner at Allen & Overy, who had been engaged by the private sector creditors grouped under the IIF.

But unlike in the 1980s and 1990s when Brady bonds were used to ease the Latin American debt crisis, buying such 30-year paper was prohibitively expensive.

“Using zero coupon instruments as collateral for the principal due at maturity on new Greek bonds would, at today’s low interest rates, have cost north of 40 cents for each €1 face amount of the secured bond,” said Lee Buchheit, sovereign debt adviser at Cleary.

He added: “The drafters of the July 21 term sheet, in their effort to replicate a 1990s-style Brady bond, seem to have forgotten that the much higher interest rates prevailing in the early 1990s allowed the zero coupon collateral of Bradys to be purchased for 15%–20% of the face value of the bond being secured.”

The deal also came apart because, rather than being split equally between the four options on offer as was the plan, Greece’s dealer managers BNP, Deutsche and HSBC, found that most creditors opted for just one – the extended par bonds. Nobody wanted to be priced down.

At the same time the country’s economy continued to shrink, widening the financing gap that need to be filled. “We needed more debt relief,” said Christodoulou.

Trying again

Once this was appreciated by the eurozone’s political leaders, work began on revising the PSI deal. A further intervention by Schaeuble calling for a 50% haircut of Greek bonds was critical in swinging support behind a deeper restructuring.

Paris’ institutions, which had initially held out against any haircut, were aghast.

In September, at its annual meeting, the IMF, which was providing €30bn of the first bailout, set out the target of reducing Greece’s debt to 120% of GDP by 2020. “It was obvious that a 21% haircut was not enough,” said Robert Gray, chairman debt finance and advisory at HSBC.

“At the IMF meetings the position changed,” said Wood. “The IMF said ‘let’s just do it the usual way’ and get the banks to take a bigger haircut but give them some incentive to accept the deal, ie, 15% cash upfront. There was not a lot of negotiation. It was essentially an imposed solution.”

Shortly after the G20 Paris meeting that October, European officials met the co-chairmen of the creditors’ committee, IIF chief executive Charles Dallara and BNP special adviser Jean Lemierre. By then it was clear that opinion had swung behind the IMF proposal to give Greece greater debt relief through a 50% reduction in its private sector liabilities.

“At one stage Lagarde, Sarkozy and Merkel asked for a calculator and were trying to work out the implications of a simple 50% haircut on all Greek bonds for the planned 2020 debt target and what coupons there should be”

When the French party realised that week that the game was up, French president Nicolas Sarkozy blamed Lemierre openly at a meeting that took place on October 20. “He shouted at Lemierre, saying it was all the banks’ fault when he realised a 50% haircut was to be done,” said one adviser present.

The final decision was to be taken by IMF managing director Christine Lagarde, Germany’s Chancellor Angela Merkel and Sarkozy at a meeting with Dallara and Lemierre in Brussels on October 26. The session ran into the following morning.

“At one stage Lagarde, Sarkozy and Merkel asked for a calculator and were trying to work out the implications of a simple 50% haircut on all Greek bonds for the planned 2020 debt target and what coupons there should be,” said one adviser involved in the talks.

At 5am on October 27 a simple press release was issued outlining the revised agreement leaving the exact details of “PSI 2” to be determined later.

Thornier elements dissected

“The October 26 deal was a ‘heads of terms’ agreement but there was lots to be worked out,” said Andrew Shutter, a partner in the Cleary Gottlieb team advising Greece.

Cleary and Lazard, which was also advising Greece, spent the next two months focused on the thornier elements of the structure, such as the legal jurisdiction of the new Greek bonds to be offered; what precisely would be offered in addition to the new bonds, such as GDP warrants and EFSF notes; and the coupon of the new notes.

“We had offered to grant Greece debt relief by voluntarily taking a 50% haircut after all,” said one creditor. “This was meant to be a consensual deal and not one in which the debtor told creditors what they had to expect.”

When one demand too many came through from Greece’s negotiating team at Lazard, Sarkozy rang up Lazard’s chairman in Paris to remind the firm that France was a bigger client of Lazard than Greece and not to endanger that relationship.

That call prompted Lazard to adopt a softer approach. In December Michele Lamarche, a managing director at Lazard, set out proposals of a co-financing agreement between the EFSF and Greece to provide the credit enhancement for the deal.

“This was a major breakthrough that was accepted immediately by Jean Lemierre,” she said.

That led to great hopes that a deal could be signed before Christmas. But in a critical meeting in Paris a week before Christmas, negotiations faltered over the level of coupons on the new bonds.

Up to this point all maturing Greek bonds had been paid in full and on time and a €14.5bn issue set to mature on March 20 focused minds in the new year. “March 20 really was a ticking bomb,” said de la Cruz. The exchange offer was drafted and finally published on February 22 with a last-minute change increasing the haircut to 53.5%.

One surprise was that the ECB refused to allow its holdings of Greek bonds with a par value of €55bn that it had bought in the secondary market to be eligible for the exchange. “It looked very bad and politically not correct. It leaves the ECB looking like a holdout creditor. Equally importantly, it makes other lenders subordinated,” said Allen & Overy’s Wood.

Many non-Europeans involved failed to appreciate the delicate nature of the eurozone and the political context of the negotiations: that this was not just about Greece but the currency union of which it was a part. The ECB was a pivotal part of the process.

“The agreement was reached against a continuously changing Greek and European economic environment,” said the EC’s Thomas. “This was unlike a single country debt restructuring, for example in Belize, where there may be a fiscal crisis but there is a single government to negotiate with.”

On March 9 Greece announced that 83.5% of its bondholders had voted in favour of the proposed 53.5% nominal haircut on the country’s €206bn of outstanding bonds in private sector hands, thus triggering the biggest ever sovereign restructuring and the first in Western Europe for 64 years.

“It was a strong result and a high participation level, which was at the top end of expectations,” said Andrew Montgomery, head of liability management at HSBC.

That was enough to trigger a collective action clause to impose the deal on all the €177bn of bonds written under domestic Greek law. Additionally, Greece said that holders of €20bn of foreign law bonds, or 69% of that portion, had agreed to tender their bonds.

When added to the €177bn of Greek law bonds to be exchanged, voluntarily or otherwise, 95.7% of all the €206bn eligible bonds would ultimately be exchanged.

Failure deflected

So was the deal a success? Greece is still not able to fund itself in the market and is unlikely to do so without assistance for some considerable time. Given that this was the aim of Greece’s programme then it has yet to succeed.

However, in the two years since the sovereign first sought aid, it has managed to reduce its private sector debts by an estimated three-quarters on a net present value basis through a (in theory) voluntary negotiation with creditors.

Considering that at the moment when Greece lost access to the market such a move was regarded with absolute horror, that is a serious achievement. “For creditors of a developed country to be paid only a 25% dividend [of their claims] is quite something,” said Wood.

“Greece has endured a depression like that seen between 1930 and 1935,” said Lazard’s Lamarche. “The deal was a success given the size of the problem and the multiplicity of stakeholders. These were very complex negotiations resulting in the first time a sovereign in the eurozone was restructured.”

Being part of a currency union with three members of the G7 – the world’s economic powerhouses – “introduced a level of complication and political nuance into the discussions that distinguished Greece’s restructuring from all other sovereign restructuring that preceded it”, said Mark Walker, until recently a senior adviser for Lazard, but now at Rothschild. “That added considerably to the difficulty of bringing the deal together.”

No one should therefore be surprised that a comprehensive solution to Greece, the eurozone and its banks’ problems has yet to be found, particularly given the political context in which the deal had to be negotiated.

In the circumstances the fact that a deal was cut in nine months was miraculous.

But the outcome of the deal concocted, and agreed voluntarily, by the banks to save Greece and hence the euro has raised further questions about their own viability in the medium term. In restructuring eurozone sovereign debt, the cost of banks’ own funding has risen.

“What is a risk-free asset rate now in Europe? That is a very important question for financial institutions going forward,” said Drennen. For the moment it remains unanswered.