A reduction in withholding tax rates has opened the door for more Indian companies to sell international bonds. After a promising first wave of financings from lower-rated private sector issuers, will the party continue?

The general election victory of Narendra Modi and his BJP party in May delivered the promise of reform in Indian politics and the lifting of the policy gridlock that had stymied growth over the final years of the Manmohan Singh administration. Offshore Indian debt issuance has picked up, as a result, and the hope is that a new era for Indian bond markets has begun.

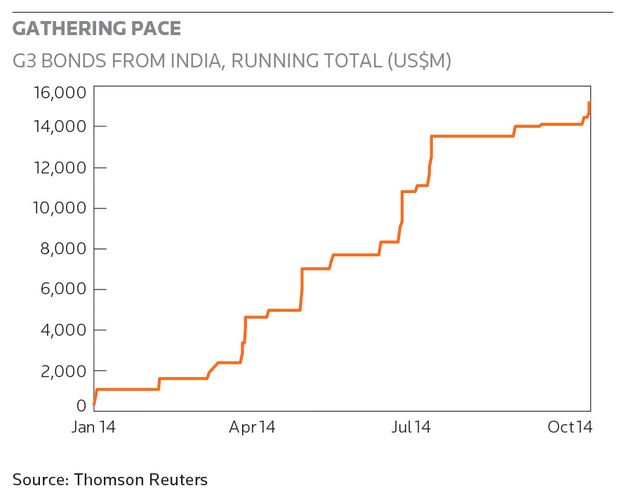

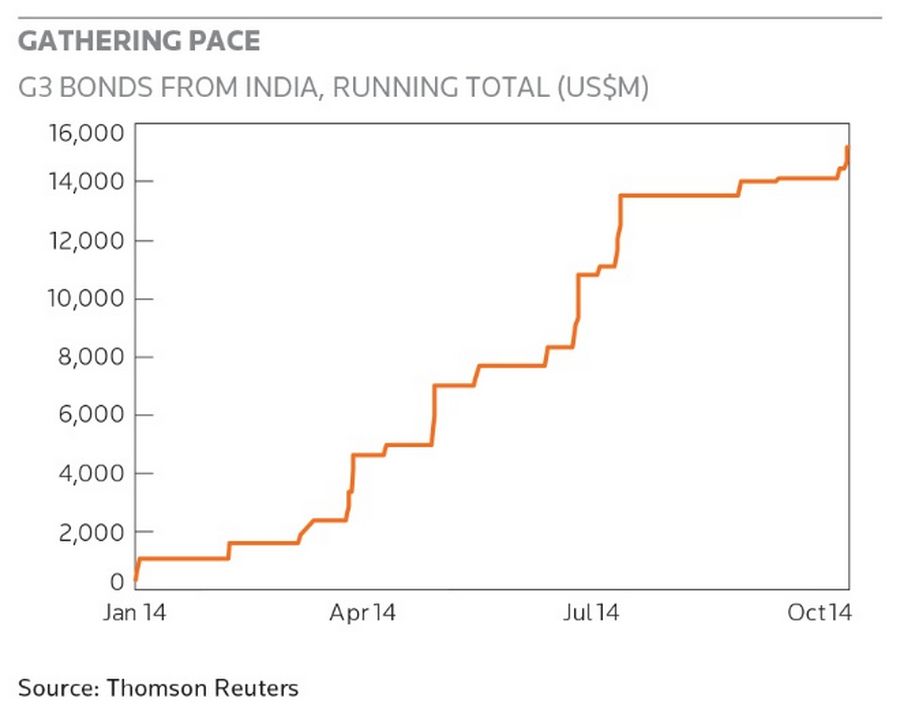

An impressive US$6.8bn has printed in the offshore India market since Modi’s victory, according to data from Thomson Reuters, with a signal achievement arriving in the form of Tata Steel’s jumbo US$1.5bn offering of 5.5-year and 10-year bonds in July and Bharti Airtel’s US$2bn-equivalent Global that printed in May just after the BJP’s victory was flagged in election exit polls.

It is not all about the political tailwind, however. The reduction of withholding tax on offshore issuance in the infrastructure sector, as well as the lowering to 5% from 20% of tax paid on bonds issued to fund infrastructure, promise to add spice to the Indian G3 debt market, even though, as this report went to press, it had yet to be formally signed.

“To have gotten a majority government, with the stability that implies, was a very important result, and the S&P ratings outlook upgrade to stable from negative also underlined the change in perception. These developments opened the door for potentially a major pick-up in offshore issuance from India going forward.”

“There was much anticipation among investors ahead of the election, with the entire India credit complex looking undervalued versus the broader Asia credit curve. To have gotten a majority government, with the stability that implies, was a very important result, and the S&P ratings outlook upgrade to stable from negative also underlined the change in perception. These developments opened the door for potentially a major pick-up in offshore issuance from India going forward,” said Alexi Chan, head of DCM, Asia Pacific at HSBC in Hong Kong.

Gathering pace

Standard & Poor’s was the only large credit agency to retain India on negative outlook and its decision in September to bump up the country after Modi’s victory added momentum to the India credit turnaround story.

“Our outlook revision reflects our view that India’s improved political setting offers a conducive environment for reforms, which could boost growth prospects and improve fiscal management,” the agency said soon after publishing the ratings move.

Prior to Modi’s victory, Indian credit had progressively widened versus the Asia credit complex, with the country’s credit perception among international investors stung by sluggish growth versus the previous three years prior to the global financial crisis, when India basked in the BRICS miracle growth story.

That, and a precipitous fall in the rupee last year, which created fears that the country’s companies saddled with offshore debt would run into default, explains the drift north of Indian credit over the previous year prior to Modi’s victory. State Bank of India five year CDS traded at around 250bp at the wides, when the rupee was in the middle of its around 20% decline last year. Last week, it was at around the 125bp mark. In the aftermath of the Modi win, Indian credit spreads snapped in as much as 40%.

“One good example was the Bank of Baroda 5.5-year deal that came back in January at Treasuries plus 325bp and which we tapped in July post election at plus 203bp for something like a 40% spread compression, highlighting the re-rating of India as a credit proposition,” said HSBC’s Chan.

“This was reinforced by the Tata Steel bond, which, at US$1.5bn, represented the biggest high-yield debut issuance out of Asia, and the earlier Bharti Airtel dual-tranche issue on which the euro tranche successfully priced through the issuer’s dollar curve.”

The Tata and Bharti (a dollar/euro combination of US$2bn-equivalent) deals take up a large lump of the Indian offshore debt issued since May, although the pipeline is rumoured to be building, with deals for Dehli International Airport, Mytrah Energy and Jindal Steel and Power waiting in the wings. These emanate from the infrastructure sector, a crucial element of the Indian economy. There has long been hope that the offshore bond market will provide the necessary massive funding requirement for India’s much-needed infrastructure.

The Tata deal printed alongside Greenko Group’s US$550m five non-call three trade, as well as Global Cloud Exchange’s US$350m five-year non-call two print. A US$2.4bn total was brought to market for the biggest single high-yield issuance day in the history of the Indian offshore primary public debt market. This issuance came on the heels of India’s largest offshore public bond offering, which marked July out as extraordinary, when ONGC Videsh printed a US$2.2bn three-tranche bond.

Perhaps, more extraordinary is the fact that each issuer was making its public market debut, in a clear sign that investors were willing to embrace fully the apparent new credentials of Indian debt under the Modi administration.

Modi’s government has signalled its clear intent to rev up the country’s infrastructure sector. Soon after assuming office, Modi fast-tracked approval for some infrastructure projects where there had been disagreement over land titles. The reduction of withholding tax on infrastructure project finance bonds is also one of clearest policy moves India has seen in the sector in years. Modi has set out a plan to introduce affordable housing for all Indians by 2022, with the price tag for the scheme somewhere in the region of US$2trn-equivalent.

“As far as the withholding tax issue is concerned, it may have an impact in that onshore entities can now issue efficiently directly in the offshore markets, rather than via subsidiaries, but issuance will, for the moment, still largely come from entities with a requirement for dollars on the balance sheet, as the hedging cost of issuing in dollars and swapping back to rupees is currently high,” said HSBC’s Chan.

An impediment to the smooth execution of the infrastructure bond policy is the Reserve Bank of India’s ban on Indian banks from purchasing infrastructure bonds. This flew in the face of a government initiative from July, which encouraged Indian banks to issue bonds to fund infrastructure, which would, in turn, be exempt from reserve requirements in an effort to encourage banks to lend to infra projects.

The hope at the RBI is that real onshore money, such as pension funds and insurance cash, will be the main buyers of onshore infra bonds, but without bank participation, liquidity in the products is likely to be low and a major disincentive to investing in them.

Despite the hopes that players in Indian debt have as to the impact of the Modi administration on issuance and future market direction, the obstreperousness of the RBI remains a major sticking point.

The same is true of the securitisation sector, where India’s banks could benefit from repackaging loans in order to free up balance sheet for future lending. In 2012, the RBI issued securitisation guidelines, including stringent requirements for the seasoning of asset pools and loan portfolio sales, which effectively shut what had been a nascent market, with CDOs issued in the local market over the previous few years and the promise of an issuance bonanza looming.

Indian banks must raise around US$200bn to comply with the March 2019 deadline for Basel III standards, with Rs52.8bn of Additional Tier 1 and Rs118bn of Tier 2 securities having been raised so far. The AT1 sector in India involving loss-absorption features, such as a temporary write-down in the event of stress, was boosted in September when the RBI granted approval for domestic pension funds to invest in the instruments. Some US$90bn of Indian bank ATIs are expected to price come 2019, of which around 70% is likely to come from state-owned banks.

Meanwhile, the Indian domestic bond market has benefited tremendously from the Modi victory, with India’s National Securities Depository reporting in August that offshore holdings of Indian debt had hit US$16.7bn-equivalent in 2014. In the June-August period, foreign investors had sucked up a chunky US$9.1bn-equivalent.

As well as the impact on domestic segment, bankers operating in the offshore debt markets remain confident that the early “Modi bounce” has not run out of steam and that deal flow is set to remain buoyant in the short to medium term. One reason is that the hedging cost for bringing dollar debt and swapping back to rupee is moving in the right direction.

“The basis swap has moved in favour of dollar issuance over the past 10 days and I would expect it to continue in the right direction such that Indian issuers, with no natural hedge into dollars, will come to view issuance in the US unit as a viable alternative to issuing onshore,’ said Rakesh Garg, head of high-yield at Barclays in Mumbai.

“It’s around negative 40bp right now at five years and there’s probably an informal target in the 50bp to 60bp region. Add to this the fact that US Treasury yields have been declining and you have the opportunity to print very low coupons in dollars and swap back. It looks very good.”

The rally in US Treasuries from the 2.65% mark at 10 years earlier in the year to the 2.20% mark with an ongoing curve flattening – the 5s/30s spread was around 200bp earlier in the year and last stood at around 150bp – has also produced buying interest at longer maturities from real money accounts. This, combined with the natural interest in Indian credit attributable to the Modi victory, the S&P action and a backdrop of benign policy should allow Indian issuers to tap long duration should they wish.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.