Germany’s equity capital markets dominated Europe in 2011 with proceeds more than twice that of runner-up Italy, even though the largest IPOs never happened. The pipeline remains bloated with multi-billion euro IPOs which will ensure this is repeated in 2012 – as long as further crises can be avoided.

(To view the digital version of this report, please click here.)

Those who lead the European ECM business are often knocked off course by both political and economic ill winds.Yet German skippers have enjoyed a relatively calmer sea amid the storm. The economy is benefiting from a depressed currency, the political climate is uniquely stable for the region, sentiment is positive and in 2012 valuations are on the up. For now the characteristically conservative and dependent nature of businesses and management is a massive benefit.

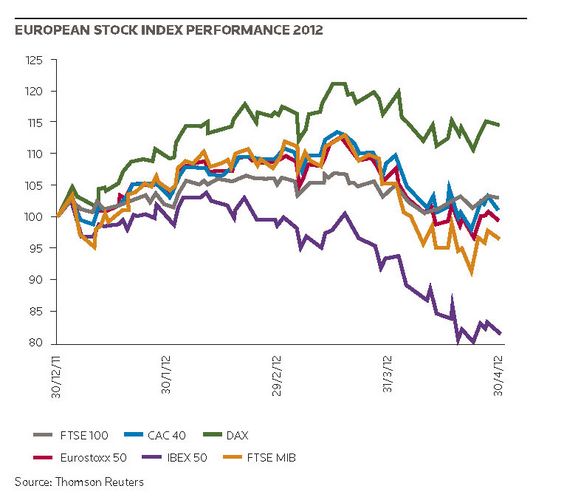

By the end of April, the main German index, the DAX, was up 15% for the year, having been up over 21% in mid-March. By contrast, the FTSE 100 and CAC 40 had delivered gains of just 3% and 1.7% respectively, while the Eurostoxx 50 had lost just under 0.5%. The Spanish IBEX 35 was off nearly 20%.

Yet despite these gains, analysts were still recommending Germany as the best place for equity investors to put their money. JP Morgan Cazenove research said the core of the eurozone remained the preference for investment.

“DAX [is the] top pick despite 15% year-to-date outperformance. Demand for credit is much more resilient in [the] core than in [the] periphery. We think [the] German domestic picture is worth highlighting: credit growth is outright positive, house prices are moving higher and wage growth is accelerating at double the inflation rate. ECB monetary policy is clearly too loose for Germany, and it is likely to remain so. These developments support German domestic plays,” the report said.

Bankers agree that the German economy is withstanding, and in some ways benefiting from, the troubles abroad.

“Despite the continuing uncertainties around sovereign debt in other parts of the eurozone, we still have relatively good news coming out from domestic companies,” said Ralf Darpe, co-head of German corporate finance at SG. “Germans are producing solid results. As an export-led economy companies are also less dependent on the home market.”

Those that have led deals in Germany in 2012 have found investors of the same mind.

“We have led several German issues this year and on each occasion the stock has, in a way, been ripped out of our hands,” said a senior German originator. “Germany is the strongest economy in Europe and we benefit from it thanks to good companies with history and management teams seen as appropriately cautious.”

The numbers back up the sentiment, even if every deal has not been such an easy sell. In the year to April 24 2012, total German equity and equity related volume totalled nearly US$27bn – impressive considering volumes collapsed Europe-wide in the second half of 2011. The volume principally came from a selection of jumbo issues including accelerated fundraisings for ThyssenKrupp of US$2.3bn and RWE at US$2.8bn, a sponsor exit in Kabel Deutschland (US$1.2bn), and of course Commerzbank’s blockbuster US$13.9bn recapitalisation.

Perfectly formed

Yet the flow of IPOs have been at the other end of the scale with largely unknown names such as RIB Software, Derby Cycle, Norma and GSW Immobilien coming to the market, with the latter by far the largest at €407m.

“The German companies coming to market have been market leaders, the transactions were of a decent size and the stock is liquid,” said Darpe. “Right now investors want that – a solid track record, mature profile, rising market share and experienced management. You see it with GSW, which has now returned [with a €201.8m rights issue] as quite the success story.”

Yet the IPOs everyone had been waiting for in 2011 did not arrive from speciality chemicals group Evonik and Siemens’ lighting unit Osram – though they are now tantalisingly close in 2012 and have been joined in the pipeline by Rheinmetall’s automotive subsidiary Kolbenschmidt Pierburg and insurer Talanx.

In fact, Kolbenschmidt Pierburg is already in the market, having launched a €500m IPO on Monday, May 7, with pricing due at the beginning of June. Rheinmetall wants to sell a stake just below 50%, which would value the company at close to €1bn. While this isn’t the largest company on the German IPO pipeline, it could prove a marker for investor appetite. Early in 2012, that appetite appeared voracious as accelerated trades flew off the blocks, but the DAX has softened since then and the political climate appears more uncertain.

The banks managing the deal remain confident that the macro-economic climate will only prove a peripheral issue. If they are proved right, the lead banks on the €5bn-plus IPO of Evonik could still target a pre-summer launch and debut, though they still need secondary markets to firm up. The senior originator highlighted that German equities currently display the highest beta, so while the world is in risk-on and growth mode all is good, but a switch to risk-off and contraction and Germany would “get whacked”, the syndicate manager said, pointing to August 2011 when the DAX lost a quarter of its value.

The frustration for bankers is that the IPOs of Ziggo and DKSH in the Netherlands and Switzerland earlier this year met very strong demand, but difficulties in completing full-year results quickly enough stemmed the flow of other issues to follow in their wake.

“Of course each transaction is being prepared as though it was the only IPO in the market – but one has to consider the potential impact of other deals as well as other market factors”

One head of European ECM also highlighted that while there was great enthusiasm for those two IPOs, the enthusiasm of the first quarter had quickly passed and the climate had become more difficult. The mantra of all participants in 2012 is preparation is key.

“Many IPOs could take place this year, but there won’t be much time to do them with short issuance windows caused by quarterly reporting and market volatility,” said Andreas Bernstorff, head of German ECM at Citigroup. “Banks won’t be able to wait for each deal to complete before launching so there will be some running side-by-side and competing.”

“Of course each transaction is being prepared as though it was the only IPO in the market – but one has to consider the potential impact of other deals as well as other market factors,” he said.

In some ways bankers remain slow to adapt preferring to wait for full-year results when launching an IPO in the new year, rather than use third-quarter numbers that still have an auditor’s blessing. As a result they failed to capitalise on the bullish sentiment in the first quarter. Instead they are planning even farther ahead to counter short issuance windows, which can become shorter if markets are not welcoming, they are planning ever farther ahead.

“In uncertain markets the level of preparation must be very high,” said Ute Gerbaulet, head of ECM at Commerzbank. “Part of this is a trend towards very early meetings with core investors. For example, we have already had early meetings with investors for a trade scheduled for 2013. It is not about putting a presentation in front of them, but an opportunity to meet management and talk about the company, sector and strategy – with management also benefiting from the investor feedback. That early dialogue could be crucial to ensure you have anchor orders when the deal comes to market.”

What is clear is that investors want cashflow, yield, cautious management and lengthy track records, and largely the German pipeline offers that – plus the large deal sizes that neutralise investor worries of aftermarket liquidity. But the qualities that ensure these dynamics make for a difficult ECM client.

“There is a big disadvantage with Germans,” said one German banker that unsurprisingly wished to remain anonymous. “In the US and UK people deal with likelihood. Not in Germany. A German car works in all circumstances. Germans want certainty.”

This is not the market in which bankers can offer it. Prepare for more postponements.