A species of accurate data once feared extinct has returned to Argentina, generating hopes that pragmatic policies will follow in its wake.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

Like bird watchers, observers scouring Argentina’s landscape for the return of a species that appeared extinct – transparent data – remain wary of flights of fancy as the chickens of economic populism come home to roost.

Recent government revisions to inflation figures smoothed feathers among analysts twitchily seeking to ascertain whether they signal a grudging return to orthodox policymaking against the backdrop of forex turbulence, spiralling inflation and soaring interest rates.

The next bird to land will be a revised GDP index to be published this month as observers seek signs of an irreversible return to pragmatism by policymakers who have little choice but to court financial markets they abandoned in a US$100bn default 12 years ago.

“They are getting back on track, slowly. The message is one that they are going towards a more orthodox approach and are going to stop intervening so much in the economy – currency manipulation, the manipulation of data – and are slowly taking steps to become much more accommodating to international investors,” said Walter Molano, chief economist at BCP Securities and author of In the Land of Silver.

There are now hopes that improving relations with the IMF could begin to pave the way for an Article 4 consultation that enables Argentina to address its burdensome debts. The country remains in default on about US$10bn owed to the Paris Club of creditor nations.

“We already had believed in Argentina’s commitment to normalising relations with the international financial community so the inflation data were a reaffirmation of that for us. It was an even better number than we expected, more credible, but in line with our expectations that Argentina really has been working on trying to improve the data and could eventually even enter into an Article 4 consultation agreement with the IMF,” said Casey Reckman, Latin America economist at Credit Suisse Securities.

It’s the inflation

Inflation is at the heart of Argentina’s problems, with the government of President Cristina Fernandez locked in a lengthy wrestling match with the IMF over its data.

In mid-February, the administration unveiled a new consumer price index indicating that prices rose by 3.7% in January – suggesting an annualised rate of over 50% – in a tacit admission that it had long been under-reporting.

Price pressures continue to grow but curbing inflation will be difficult for the left-of-centre administration and, unable to borrow abroad, Argentina has been printing money.

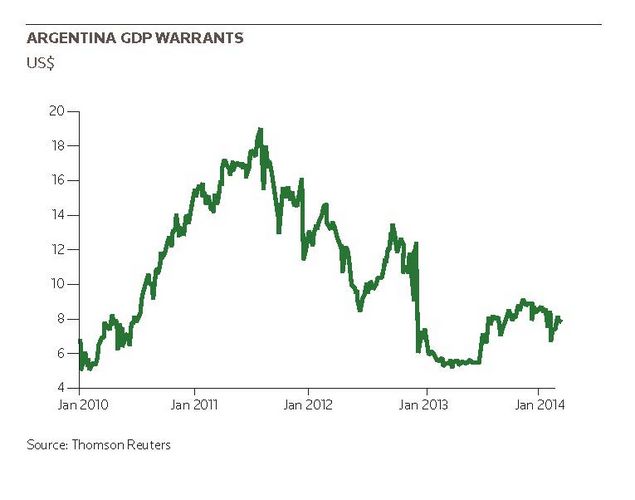

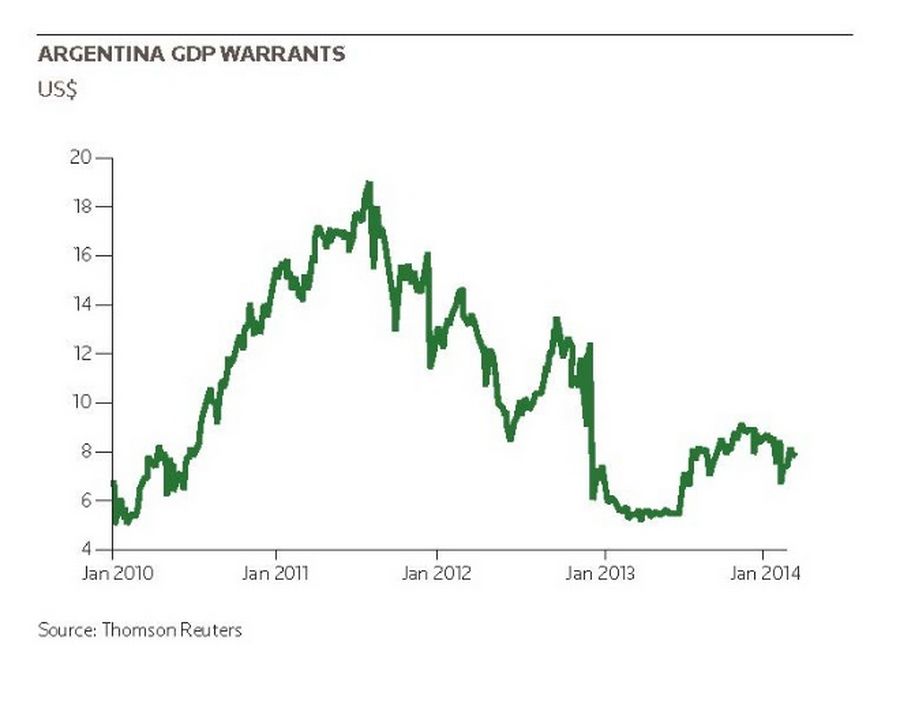

All eyes are now turning to GDP. According to frontier market investment banking boutique Exotix official data released in December showed that real non-seasonally adjusted GDP grew by 5.5% year on year in the third quarter after first-half growth of 5.7% – a slowdown, but better than expected.

Exotix believes this shows growth well above the 2013 GDP trigger of 3.22% for a payment on the warrants this year, and is assuming 4% growth, suggesting payments in December this year [2014] of US$5.9 on the dollar warrants, €5.4 on the euros and US$1.42 on the ARS warrants at the blue-chip rate.

But there is uncertainty over whether these payments will be made – and the government may be tempted to revise it to avoid making a payment. Exotix says the risks seem skewed to the downside, and in January changed its recommendation to hold from buy.

“We know GDP growth has tended to be overstated by 1 to 2 percentage points per annum every year over the last few years, and on that basis the growth last year that is tracking at around 5% could easily then be revised down to 3% and so below the trigger – and therefore there would not be a payment. Clearly the suspicion will be that it’s an opportunistic revision so they don’t have to pay US$4bn later this year at a time when their reserves are under pressure with an election looming. But equally, it is not so obvious to me that growth will be revised significantly down, or even whether growth could be revised up,” said Stuart Culverhouse, chief economist at Exotix.

‘High stakes game’

“I certainly think the bias is to be down, but whether they will revise it so far that it means no payment will again test their international credibility, because people will see it as politically motivated. The IMF is breathing over them on inflation and if the GDP isn’t credible either that puts them even more at odds with the international financial community. It’s a high stakes game.”

Culverhouse said that if growth above the 2013 GDP trigger is validated, any payment on the warrants this year will be about US$6.

Buenos Aires is also changing the GDP methodology, injecting further uncertainty, and in emerging markets GDP can inspire even greater defensiveness than inflation.

“The fact that they are being almost transparent on inflation – and I qualify the almost – leads me to believe that they are likely to be almost transparent with GDP, but again a lot of data go into that calculation and they can always play games. Traditionally their communications and their source of pride have been more focused on huge growth than anything else, so I can imagine they will be even more tempted to manipulate it than inflation,” said Diego Ferro, co-chief investment officer at Greylock Capital.

Observers have mostly read into the government’s response to pressure on the peso in January another sign of a pragmatic turn. The biggest year-to-date fall in the currency pushed the peso down 20% to eight to the dollar before central bank measures stabilised it.

What caught their attention was the government’s hands-off response, as it permitted the slide rather than spend plummeting reserves – now standing at US$29bn from US$53bn in 2011 – caused by a flight to dollars. Cut off from financial markets, Argentina desperately needs to safeguard its reserves for payments on its restructured bonds.

Culverhouse said that although allowing the currency to fall was the right thing to do, it provided further evidence of inconsistency.

Haphazard policies

“Of itself it’s alleviated some of the pressure on reserves, but absent a wider change in the economic approach – and basically orthodox policies – it just smacks of opportunistic policymaking.”

Argentines are bracing for more FX volatility and many analysts expect the peso to be at 10 to the dollar by the end of the year.

“We would have preferred to see a devaluation accompanied by a credible and comprehensive fiscal and monetary tightening plan. Our concern is that although the measures they have taken to help stabilise the situation since the devaluation are positive and buy them some time, some of the same pressures that were on the currency and on reserves before the devaluation could resurface by the third quarter of this year,” said Casey Reckman of Credit Suisse.

The FX turmoil coincided with currency falls in Turkey, Brazil, South Africa, India and Russia, but analysts dismiss any systemic risk of contagion and blame haphazard policymaking for Argentina’s woes.

The government’s defence of reserves has underlined how it has limited its own room for manoeuvre on debt. Buenos Aires has, in effect, signalled that it cannot go on paying debt out of reserves and must start issuing it again.

It should be an appropriate moment for Argentina to return to the capital markets. The key to doing so lies in the resolution of its lengthy US court battle with bondholders who refused to participate in restructuring after the 2001 default.

The latest development came in February when Argentina filed a petition seeking a supreme court review of a lower court order that it cough up US$1.33bn to the “holdouts” when it pays creditors who exchanged bonds under offers in 2005 and 2010.

All bets are off as to what happens next. If the supreme court rejects the petition it could trigger default, but the most popular scenario is that it will ask the US Solicitor General to consider the petition – prolonging deliberations until late next year when the Fernandez government bows out. This would leave the incoming administration with a headache.

Some form of rapprochement is certainly in Argentina’s interests and would open the door to the markets again.

“I don’t think the issue is so much about technical default; it is that the government realises that the lowest hanging fruit they have in order to raise international funds is for them to fix the holdout issue and, with that, being able to access international capital markets,” said Ferro of Greylock Capital.

Fernandez has certainly provided plenty of ammunition to those who say she lacks a clear picture of how to manage the country’s problems.

But as sovereign debt ratings improve, weary investors may now simply be focusing on the candidates most likely to succeed her, Sergio Massa and Daniel Scioli.

“Whether it’s going to be Massa or Scioli, the market is definitely anticipating a change – which is going to be a positive thing,” said Molano.

Argentina GDP warrants

Argentina GDP warrants

| Estimated GDP warrant payments in December 2014 (based on assumed 2103 growth) | |||||

|---|---|---|---|---|---|

| Currency | Scenario 1 (3.5% growth) | Scenario 2 (4% growth) | Scenario 3 (4.5% growth) | Scenario 4 (5% growth) | Scenario 5 (5.5% growth) |

| US$ | 5.77 | 5.89 | 6.01 | 6.13 | 6.25 |

| € | 5.33 | 5.44 | 5.56 | 5.67 | 5.78 |

| ARS (in US$) | 1.39 | 1.42 | 1.45 | 1.48 | 1.51 |

| Source: Exotix | |||||