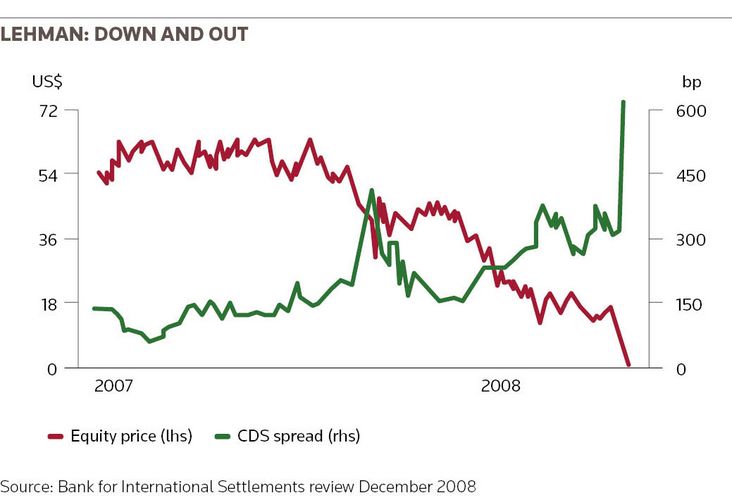

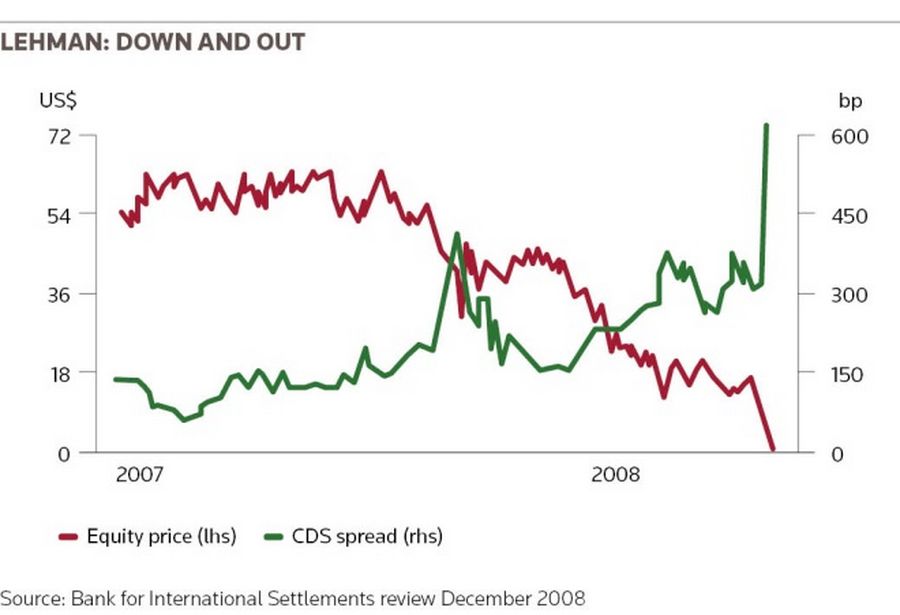

At 7:56am on September 15, 2008 - four minutes before the market opened on a Monday morning - a judge sitting in a makeshift courtroom in a law office in London’s Silk Street signed a document putting Lehman Brothers’ European operation into administration.

A few hours earlier, last-ditch efforts in New York to find a saviour had failed. US politicians and regulators decided not to bail Lehman out. Lehman was bankrupt.

The collapse of the world’s fifth biggest investment bank sent shockwaves across global markets and started the largest and most complex bankruptcy in history.

The workout turned out to be many times more difficult than the bankruptcy of Enron, according to several people who worked on both.

Lehman had more than 7,000 legal entities across 40 countries, resulting in at least 75 separate and distinct bankruptcy proceedings. It has required several landmark court rulings to resolve disputes about who had priority claims over the carcass.

“That’s because the sums involved are so eye-watering,” said Euan Clarke, a partner at law firm Linklaters who has worked on the Lehman administration from the start.

BIG WINNERS

Ten years on, more than US$150bn has been paid to creditors from bankruptcy proceedings.

Many investors have done very well.

One of the big winners is CarVal, a distressed debt hedge fund ultimately owned by agricultural giant Cargill.

CarVal got involved almost immediately, providing a US$100m debtor-in-possession loan to PwC, which had been appointed as administrator for Lehman’s London arm, Lehman Brothers International Europe. That DIP loan allowed PwC to pay key LBIE staff and run operations.

It also gave CarVal insight into the complexity of the Lehman operations, and the hedge fund ended up investing more than US$4bn in buying various classes of creditor claims in the US and Europe.

CarVal has not revealed its profit on the trade, but is estimated to have achieved an annual internal rate of return of around 30% across its exposures.

Lehman had assets with a face value of US$639bn and liabilities of US$613bn, according to its US bankruptcy filing. The role of the administrators or trustees for each entity was to realise assets, agree claims and then pay them to the fullest extent possible. LBIE ended up holding surplus assets partly because it was a well-capitalised entity at the time of collapse, and held a large pool of collateral.

There’s no global insolvency process, so every entity had to be treated in isolation. The rules in each jurisdiction and the size and type of each business helped dictate how much creditors got back.

LBIE creditors, for example, have been fully repaid and also received an extra 40% due to a surplus in recoveries, a rare event in any bankruptcy. Investors that took punts early in the process - such as Elliott Management and King Street Capital, as well as CarVal - made handsome profits.

In the US, Lehman Brothers Holdings Inc, the parent company, has paid about 45 cents per dollar of allowed claims to the largest unsecured creditor class. Well below the LBIE payout, but double what was estimated in a 2012 plan of reorganisation - and creditors could get more if legal disputes go their way.

That is likely to have been lucrative for hedge funds including Paulson, which is reported to have started buying Lehman obligations on the day the bank filed for bankruptcy at as low as 7.5 cents on the dollar.

Lehman Brothers Inc, the US broker-dealer that was largely sold to Barclays, has paid about US$9bn to unsecured creditors, equivalent to 40% of claims. Barclays won a court battle with LBI that gave the UK bank US$4bn of disputed assets and limited LBI’s payout.

“GROUND ZERO”

The vast majority of original creditors fared far worse, however.

Many - including banks, other financial firms and everyday business customers such as photocopier suppliers - sold their claims to hedge funds because they needed cash, were not allowed to hold distressed credit, didn’t need the hassle, or didn’t fancy their chances of being paid back.

Only about 10% of LBIE creditors, for instance, are original creditors who stuck with their claim, said Russell Downs at PwC, one of LBIE’s joint administrators.

“If you were a creditor that sold out in the early stages because you didn’t like the look of the insolvency, I think you would have been kicking yourself,” Downs said.

“But if you were a creditor who sold out because you needed liquidity for your own survival, and you could sell out in a competitive process and get a price, then that’s a trade you have to stand behind.”

James Ganley, managing principal at CarVal, said lots of original investors were keen to sell as the complexity and uncertainty of the credit exposure was “extremely high”.

“Lehman was at ground zero. Expectations were very low and no one could have predicted the LBIE estate would go into surplus,” Ganley said.

Still, Downs said the original creditors remained an important group. “We were very mindful there were a group of stakeholders who put their faith in us for the duration and didn’t sell out their claims and therefore it’s important to respect that and find a solution that makes them think ‘that’s why we stayed in this process’,” he said.

HEAVILY DEBATED

Creditor claims changed hands actively, especially in the early years, as they traded below 20% and then ratcheted higher on the back of court decisions and improved recovery prospects.

After LBIE fully paid senior creditors in 2014, attention turned to who would get a £8bn surplus from the European entity, fuelling aggressive tactics by hedge funds who were fighting over which class of credit should get the spoils.

“You can imagine that when you put £8bn on the table and say ‘give me your reasons why you should have it’, it’s going to be heavily debated - and it was,” Downs said.

When the UK’s Supreme Court ruled in May 2017 that senior creditors should get interest on their claims before junior creditors were paid, it reversed earlier court decisions and marked a £1.5bn swing in the amounts that the separate creditor groups received.

The fight for the surplus has been settled by court decisions and a scheme of arrangement proposed by PwC to avoid years of squabbling. It saw a final £6bn paid out to senior creditors in July, taking their recovery to 140%, with any further excess - possibly another £2bn - to be paid to a small group of subordinated noteholders.

PwC expects it to take another 18 months to mostly finish the wind-down of LBIE, but other insolvencies could take longer.

LBHI, which emerged from bankruptcy in March 2012 under the US process, has distributed US$125bn to unsecured creditors and expects to distribute another US$3.9bn. More could be on the way, but possibly not for years as legal action drags on.

EX-LEHMANITES

Hundreds of former Lehman staff have been among those engaged in the workout, especially in London.

LBIE has been based in a 23rd floor office of Citigroup’s Canary Wharf tower, close enough to see the former Lehman tower where staff were turfed out onto the street in September 2008 carrying their belongings in boxes.

PwC drafted in ex-Lehman employees to accelerate the wind-down and maximise the assets that could be recovered. At its peak LBIE had 750 staff, including about 500 who previously worked at Lehman. Some stayed for years.

LBIE effectively had to disentangle IT systems and functions and then rebuild them.

“We were a fully operational investment bank but in a wind-down. We had receptionists, lots of IT people decommissioning and building new systems, some traders, valuation people, middle and back office, treasury people, lawyers,” Downs said.

Linklaters’ Clarke said the early challenge was getting on top of “the sheer mass of issues that were tremendously urgent”, including demands from customers, counterparties, creditors and staff.

Lehman had 900,000 derivatives contracts that needed closing out, for example, but there were simpler, more pressing headaches: claims were flooding in by fax and post. Blackberries seized up under the weight of traffic.

“It was a task to keep on top of what was happening,” said Clarke.

Administrators, lawyers and others have also done well from the lengthy bankruptcy process. LBIE has paid out about £2bn out in expenses and costs. Around £1bn has been paid to administrators, while another £651m has been paid to employees and there has been a further £417m of legal and professional costs.