To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

IFR: Are there hurdles to overcome when that capital account is liberalised? What sort of dangers do we need to be aware of for offshore RMB?

Tom Byrne, Moody’s: If I could take a step back, the offshore RMB is becoming a potential common currency platform for East Asia, and this is interesting because the Eurobond format really took off after the introduction of the euro. Given East Asia’s historical circumstances and the current politics in the region, there’s no prospect of a common currency or a regional central bank. So this is a very interesting question, whether the RMB will become the common currency for funding in the region.

I don’t think the Chinese government debt situation will deter the liberalising of the economy, in fact this will probably spur efforts to further liberalise – as the Third Plenum outlined, the Communist Party is well aware of the financial challenge facing the Chinese system. So I see these changes that fellow panellists have named, but you’ll bump into a wall eventually until there’s a fully convertible capital account, internal regulations are improved, internal disclosures improve, so that we can have a deep and liquid market as we do in the US, where US Treasuries underpin the US dollar as a global reserve currency. There you have a deep market, a liquid market and investors have the full-faith backing of the US government.

IFR: Thank you, Tom. Let’s open the discussion to the floor at this point.

Audience: What advice do you have for a country like mine that is at the very early stage of developing a bond market?

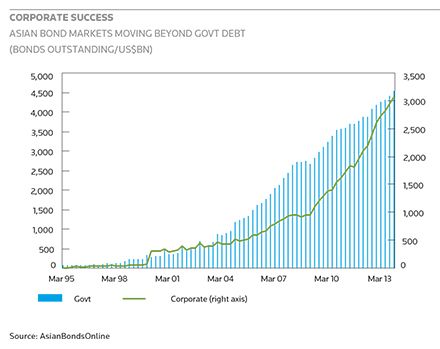

Reza Siregar, AMRO Asia: What we have seen, if anything needs to be done to boost the bond markets, it’s really to get the corporate market going. Sovereign bonds really have to be the starting point, but I think beyond treasury and central bank securities we need to have corporate bonds. There are two sides to that equation – one coming from the condition of the market itself, and the other from the investor. Countries that have managed to find stability in terms of inflation and banking system liquidity, countries that have continually managed their balance of payments, those countries are usually able to jump start their corporate bond markets – in Korea, for instance, as well as Malaysia and Thailand. We start to see some corporate activity in Indonesia but it’s slow, because there is a lot of volatility in terms of the current account position and also inflation. It’s the same story with the Philippines. The political and macro stability part has to be there, that’s clear.

From the investor side, as our colleagues here have also highlighted, they have been very conservative in moving into the bond market. This is where a lot of initiatives from governments, central banks and the ADB are focusing, to support the smaller issuers and allow them to tap into the bond market. They don’t have the stability, the rating, or the name, but a credit guarantee mechanism at least helps create some kind of way for these companies to tap into the market.

If you look at the financing needs of our economies, clearly we need to go beyond the banking system. Infrastructure needs 15–30 year financing, and that is a different class of maturity for the banking sector. Bond markets in this part of the world are 5–10 years, so to go beyond that will pose a challenge in terms of how do you price them. If you go back into the recent crisis when the European banks pulled out, the issue there is not liquidity, because the East Asian banking system is quite liquid. The problem is that we have been focusing more on retail activities. For wholesale, long-term infrastructure financing, we are still relying essentially on European banks, and this is something where the bond markets can fit in quite nicely.

Audience: I have a question about yield curves and liquid bond markets. Suppose infrastructure bonds are issued, do we need a yield curve for that? Probably Asia can start with project bonds without constructing the entire maturity curve. Second question: the purpose of the development of the local bond market comes from 1997, as you said, but if we are developing the international bond markets then aren’t we going back to the same problem?

Thierry de Longuemar, ADB: Project bonds, yes. You need a benchmark and you need a yield curve, because you need to price the bond. The base price would be based on the benchmark and the yield curve, and you add on to that the risk of the given project that you are financing. So my answer is that you still need a benchmark and a yield curve.

On the second question, to my mind the problem is not onshore or offshore – the problem is currency. The Thai baht crisis of July 1997 was partly caused by an overreliance on non-Thai baht debt, both by the government and by Thai companies. It was a currency mismatch. It doesn’t matter if you issue offshore or onshore; what matters is the currency you issue and how it fits into your asset and liability management. One of the main drivers is the currency of your revenues, and most likely if it is a domestic-led operation you will need to fund in local currency.

Tom Byrne, Moody’s: I take issue with this notion that if Asia could depend on regional funds it would automatically ensure stability in the financial markets. This was proven to be false in the eurozone crisis. Basically you had weak governments and a weak banking system, with balance sheets that were vulnerable to economic shocks. There, all the governments finance themselves through euros, and yet they still suffered the same crisis. I think it’s too simplistic to say stability is imparted by this dependence on regional funding in the same currency: there are other factors at play.

Reza Siregar, AMRO Asia: Increasingly we need to understand the investors. While certain things like currency and so on continue to be important, we also need to look at the participation of foreign investors in our bond markets. What type of foreign investor can influence volatility in these bond markets, and how much. We need to do more studies on this.

Audience: When you’re talking about pan-Asian corporate bond markets, companies in another country might not have the same accounting practices and transparency, which raises a whole set of questions about how you would price the risk. In China, only now the government is sending the signal that you need to price risk correctly. How is HSBC or Moody’s dealing with the challenge of accounting practices?

Alexi Chan, HSBC: I think it’s a great question. We do operate in a global bond market where standardised accounting practices and detailed disclosure is at the core of investors’ decisions when they come to purchasing a credit. When we bring Asian issuers to the global market, there is typically a requirement for one of the major international accounting firms to be the auditor for the financials in the prospectus. The interesting question is how that relates to the Asian local markets. If you have a local company trying to fund in a local bond market, a requirement for a major international auditor may not be appropriate, or may even be an impediment to the development of the local market.

Clearly if we want international investors to buy into an Asian local currency market, they will want to have some comfort around the standard to which the accounts have been prepared, and if we’re looking at an Asian corporate going into another Asian currency bond market, those sorts of issues are going to be important as well. Ultimately we would like to see the Asian bond markets move towards a goal of higher standards and uniform practices. But we have a long journey to get there, and clearly we want to avoid using a sledgehammer to crack a nut in cases which may impede the development of the markets. As we’ve discussed throughout this panel, it can also be useful to have certain supportive mechanisms to help the market grow: credit enhancement can clearly mitigate some of the issues you’ve talked about, as investors will be looking predominantly at the quality of the guarantee rather than the underlying business.

Yoshihiro Inoue, Daiwa Securities: I totally agree with your point. In the Japanese Samurai market, if non-Japanese companies want to come, the accounting standard is one of the key hurdles. For example, Thai companies cannot issue Samurai bonds because the Japanese government does not accept Thai accounting standards. It’s the same for India and the Philippines as well. This is a very basic thing: we need a simplified standard for disclosure in ASEAN and Japan in order to facilitate issuers to come to market.

Audience: My question is in regards to the currency mismatch. Mongolia has successfully issued international sovereign bonds in 2012, and HSBC was in fact an underwriter on both issuances, but the problem is when it comes to the local currency bonds. When you have an illiquid currency – and I don’t know how many people here know about Mongolian tugrik – how do you actually resolve that issue? And I think that question goes primarily to ADB. What would be the advice for countries such as Mongolia who are looking to attract overseas issuers?

Thierry de Longuemar, ADB: This is exactly what we aim at – helping countries to develop their infrastructure to allow issuers to access the local currency and manage that exposure. Mongolia is a case where we are considering an issue, but we haven’t done anything for the time being. There are other ways to fund ourselves in the local currency when there is no bond market. One is the cross-currency swap market, which we have been using in currencies like Kazakh tenge, for example, for a significant loan we agreed in tenge. That would be with a commercial or investment bank. There is another option which would be to do the same with the central bank. It would be a bit unusual, and I know that we have considered it here in Kazakhstan four years ago. It didn’t work then, but I know that it would work today – the reason being that the central bank is eager to get more dollars, while we are interested in getting more tenge. This is an option that we have also considered in the case of Mongolia. So there are options, but those are temporary options. The best is to be able to contribute to developing the local market ourselves, and to then on-lend in the local currency.

Audience: On the subject of infrastructure financing and credit enhancement, you’ve mentioned project bonds. As we all know those project bonds need initiatives to encourage them, and insurance-type schemes can be helpful. What is the status of those initiatives?

Alexi Chan, HSBC: Infrastructure bonds are one of the key themes we’re working on globally. We’ve talked in general about the disintermediation of banks, and how under the current regulatory regime that we are now operating in, it will often be more efficient for the capital markets to provide infrastructure financing. The natural effectiveness of the bond markets in providing long tenors is also well suited to infrastructure finance.

I’m pleased that in an Asian context we are seeing developments in the project bond market alongside the bank market, and the local market that has gone the furthest in developing that is in Malaysian ringgit, where large-scale infrastructure financings, often involving multi-tranche or staggered issuance, have become commonplace and are widely accepted by the investor base. That’s a real success story in Asia.

In a more general context, infrastructure financing clearly presents a different risk proposition to corporate credit, and the provision of credit support here can also be useful. That’s certainly very common in the loan market and we’re looking to a variety of credit enhancement providers to get involved in the Asian bond markets as well.

Yoshihiro Inoue, Daiwa Securities: These kinds of project bonds come with significantly higher risks to plain vanilla corporate bonds. It can actually be similar to a business trust or REIT, or other dividend-driven products. The investor base is different from the pure bond investor, so we can also think about listing on the Singapore Stock Exchange as a business trust to target equity investors as well. There’s a lot of room to develop new products.

Thierry de Longuemar, ADB: We have set up in 2012 with the ASEAN+3 the CGIF, which aims at providing an enhancement mechanism to allow corporates from the ASEAN countries to issue at the minimum investment grade. This is not a response to the need for more project bonds, but it’s a beginning. As a matter of fact we are also considering an infrastructure fund, which would be specifically targeted at infrastructure financing and providing the right vehicle to enable more of those in the ASEAN context.

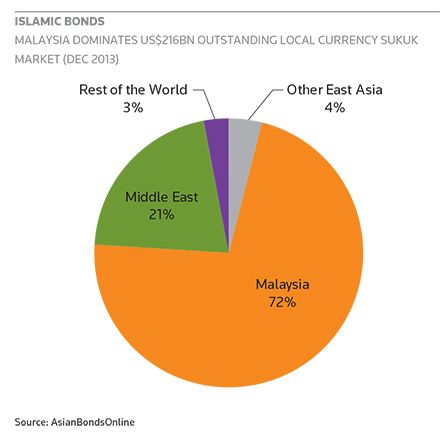

Audience: My question relates to the emergence of a new phenomenon in the Asian markets, that of Islamic securities or sukuk. Last year more than US$20bn of sukuk were issued in South-East Asian markets and in the GCC, one of the biggest markets at the moment. I was looking at a report this morning that HSBC has been the lead arranger for more than 70 sukuk issues last year. How do you see the emergence of this phenomenon in the Asian bond markets in terms of growth so far and prospects for the future?

Tom Byrne, Moody’s: We recognise the growing role of sukuk issuance, and we’ve had a very recent internal reorganisation where we actually have an analyst in charge of a task force on sukuk issuance. This will be based in Dubai but we’ll have analysts based in all the major regional offices. We’ve rated sukuk, both sovereign and others, and it’s an important upcoming phenomenon that we’re following and we want to be involved in.

Alexi Chan, HSBC: Islamic finance is an important part of the global capital markets, and one that HSBC has helped pioneer ever since the first global sukuk from Malaysia in 2002. We’ve seen specific markets, in particular Malaysia, where the prevalence of Islamic securities has become a key part of the local markets, and that’s been a big success story for Islamic finance in Asia.

From a bigger picture perspective, the Islamic finance market can help facilitate cross-border capital flows and help connect the Middle East and Asia in particular. Clearly that means involving a bespoke pool of investors, and we see considerable potential for those capital flows to benefit Asia and other regions.

IFR: Ladies and gentlemen, thank you all very much for your remarks.