Sustainable infrastructure agenda moves centre-stage

Climate change has risen towards the top of the global policy agenda as the impact of rising temperatures is felt around the world. Greenhouse gas emissions are driving changes in weather cycles, polluting cities and putting at risk long-term global economic growth. This is providing a strong impetus towards transitioning the world towards a low-carbon economy. Nick Herbert reports.

That transition, however, cannot come at the expense of the wealth generation that is needed in order to meet the United Nations’ sustainable development goals. The world cannot grow without sufficient infrastructure, but only by building sustainability into infrastructure requirements will there be a chance to reach the 2030 aims of reducing poverty and limiting temperature rises to below 2oC above pre-industrial levels.

Political commitment to tackle the effects of global climate change was reinforced in New York in April, when representatives from 175 countries congregated at the UN for the signing of the landmark agreement, reached in Paris at the end of 2015, to limit greenhouse gas emissions. The Paris agreement, adopted by over 190 countries, is an attempt to bring down greenhouse gas emissions such that by the second half of this century, any residue pollution in the air can be safely absorbed by natural systems.

It is a laudable aim but achieving that aim is no simple matter. And building the kind of sustainable infrastructure that will take us to that end game is going to be expensive. At least there is general consensus as to the value of the exercise and there are hopes that changes will come sooner rather than later, now that the world’s two major polluters – the US and China – have both agreed to ratify the deal.

With the political will firmly in place, the conversation is increasingly turning to address the sticky problem of financing the whole thing. “Pre-COP 21, very few people talked of the financing being critical to the climate solution,” said Ulrik Ross, global head of public sector and sustainable financing at HSBC. “But it’s definitely talked about now. It’s a game changer.”

To reach proposed targets, infrastructure investment requirements between 2015 and 2030 could reach as high as US$90trn, according to New Climate Economy estimates, equivalent to US$6trn a year. McKinsey points out that the value of existing infrastructure currently stands at US$50trn, which highlights the scope of the task ahead. The consultancy firm also estimates the current annual spend on infrastructure at US$2.5trn to US$3trn so there’s a considerable gap to be filled.

Not only does the yearly run-rate on infrastructure investment need to double, the infrastructure it builds needs to be economically, socially and environmentally sustainable, which will add more costs to the bill. In fact, building sustainability into infrastructure requirements could increase the up-front capital costs by up to 6%, although that cost could be clawed back from potential long-run cost savings from a reduction in the use of fossil fuels.

Energy generation is the sector most needing reform. It accounts for roughly two-thirds of all greenhouse gas emissions, according to the International Energy Association (IEA). It is also one of the areas where technology is changing fast to address the problems of relying on fossil fuels.

Indeed, there have been early signs of success in moderating emissions. In 2015, global energy-related carbon dioxide emissions stayed flat for the second year in a row. This is in stark contrast to the previous 40 years where a decrease in emissions had been tied to an economic crisis. Perhaps more reassuringly, there was a decline in energy-related emissions from China and the US. The decline in China was due to a decline in coal usage and the switch to low-carbon sources for electricity generation, while the drop in the US was put down to the increased use of natural gas in its generation capacity.

The switch to renewable sources of energy will play a key role in the reduction of emissions. The IEA reckons that renewables represented some 90% of new electricity generation in 2015, with wind representing over 50% of that new capacity. The numbers can be cautiously interpreted as suggesting that the link between emissions and growth has started to decouple.

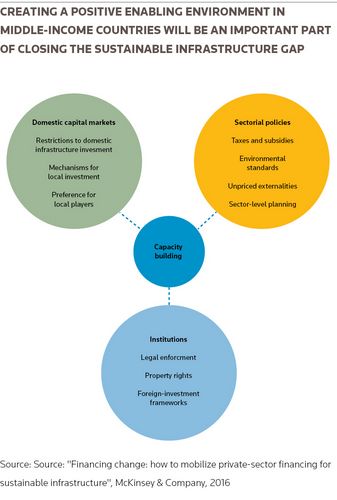

Nevertheless, an increase in emissions was still a feature in most of the rest of the developing world, the Middle East and Europe. It shows where much of the infrastructure build is most required. McKinsey estimates that over 60% of the financing gap for infrastructure lies in middle-income countries, where future demand is more than 2.5 times projected spending. “These countries not only need more capital but also more affordable capital,” it said in its report, “Financing change: How to mobilize private-sector financing for sustainable infrastructure”.

Mind the gap

The cost of transitioning the world to a low-carbon economy has been calculated and the political will to achieve such a transition cast in stone. But it needs more than political will for the project to be successful. The bill still needs to be paid. Given the long-term nature of infrastructure development, government funding will play a major part in realising the targets. Yet, with the many and varied demands on government spending and budgets already squeezed, encouraging private sector funds towards the sustainability goals will be essential.

Even China, with all of its resources, has recognised it does not have the public funds at hand to finance the level of green investment it needs. “Now we need to focus on practical solutions to mobilise the private sector,” said Mike Kerlin of McKinsey. “We have a significant chance of closing the gap. But to succeed, it will need a lot of co-ordination, a lot of focus on early-stage planning and a lot more blended financial solutions.”

There is more than enough cash in the system to fund the infrastructure requirements. Creating the kind of environment that will mobilise private sector funds into sustainable infrastructure, however, will need commitment: from governments with respect to policy and legal framework, from multilateral development banks, and from private sector banks, investors and corporates.

What everyone calls for is greater transparency and measurability so that funds can confidently be directed towards sustainability. In essence, we need a sustainable financial system that aligns long-term returns with long-term sustainable growth.

Overcoming barriers

Banks already play a critical role in the financing of infrastructure projects and will continue to do so. They have the balance sheet, the experience and the contacts needed to bring other players into financing projects that are both sustainable and commercially viable.

They have the capacity to arrange and syndicate loan financing. They also have the ability to recycle debt into the bond market and have access to the range of financial instruments that allow them to hedge against interest-rate, credit and foreign-exchange risk. Local banks have the added advantage of local knowledge and access to local currency financing.

Banks will continue to play an important role but since the financial crisis, the banking sector has been and continues to go through difficult times. Profits have taken a hit in the low interest-rate scenario and demands on capital requirements as a result of Basel III have reduced the appetite for lending, particularly in the all-important long-dated maturities that are essential for infrastructure projects.

Banks can, however, use their experience and reach to add value to discussions on structuring any form of financing but it requires a change in approach when it comes to sustainability. “Banks vary as to what they can bring to the environmental question,” said Magnus Borelius, head of group treasury for the City of Gothenburg. “They need to add that knowledge to the process.”

If banks are finding it more difficult to commit long-term funds, new sources of finance will need to be discovered, and there are signs that the institutional investment community is increasingly being wooed into participating. Investors are aware of the benefits of investing in assets that are secure and sustainable, which produce long-term returns and respond to stakeholder and social pressure. Many have already adopted environmental, social and governance criteria into their investment decisions and are intent on directing more assets in that direction.

According to Allianz, which developed its ESG screening in 2013, “we do want to keep growing [funds] assuming we can continue to find good investments. We do not have specific investment targets but we are planning to double our investments in infrastructure and renewable energy in mid-term.” Allianz is not alone in expressing a commitment to the cause. The Institutional Investor Group on Climate Change (IIGCC), which represents over 400 investors with US$24trn in assets under management, is urging governments to maintain the momentum evident from the Paris agreement.

“Countries that accede early to the Paris Agreement will benefit from increased regulatory certainty, which will help attract the trillions of investments to support the low-carbon transition,” the IIGCC wrote in a letter in April to the heads of state of the world’s largest economies. Insurance companies and pensions funds have the fiduciary responsibility to match assets with liabilities and so are natural candidates to take on long-term investments.

“By scrutinising investments and insurance projects from an ESG perspective, we can identify risks and opportunities that may not be reflected in current market prices, and capitalise on them for the benefit of our shareholders, customers and other stakeholders,” a spokesperson at Allianz said. “This is especially relevant to Allianz, because as an insurance company we manage and carry risks that range from one year to decades.”

Safe returns have traditionally been available in the bond market, but with interest rates having been so low for so long, strategies have been changing.”Investors are looking more seriously at debt and equity in project finance,” said Allan Baker, global head of advisory and project finance for the energy group at Societe Generale CIB. “Here they can find steady, long-term returns that beat the bond market and are uncorrelated to financial markets.”

That has been very evident in renewable energy, where technology improvements have been matched by the building of a successful track record so as to make parts of that industry a relatively safe bet. They are quick to build, and projects move swiftly onto generating predictable cashflows, at least in some regions.

“Renewable energy – by and large – is a well established and investable asset class in the EU, where obstacles mainly exist in the sense that it is a fairly heated market with lots of demand from investors and comparatively little supply of attractive projects,” Allianz noted. “In emerging markets, you might have much less competition from other investors, but the risks which might potentially impact long-term return-potentials are obviously also higher.”

Exposure to these assets is taken in a variety of ways. Shareholdings maybe take in private equity firms or specialist infrastructure funds, for instance. Or in some cases, assets will be taken onto the balance sheets. “[Investors] have been recruiting specialists into their own funds in order to take on different elements of risk,” said Baker. “They may team up with an experienced developer, for instance, and perhaps look to refinance before completion in order to get a better return.”

This change in approach is likely to continue as internal targets for infrastructure and sustainability become more dominant, resulting in large insurance companies and pension funds becoming more visible as partners with the firms that build and operate infrastructure projects.

DONG Energy, for instance, in its Gode Wind offshore wind farm engaged in a systematic debt and equity structuring exercise. Key elements of the financing strategy were to establish a 50/50 joint venture between DONG Energy and financial investors, to secure a significant participation of institutional investors from the German insurance industry, and to use a project bond as an alternative to both pure equity funding or bank debt.

Investors feel most comfortable in their home markets. So, while buying a wind farm in Europe may have become close to a commoditised option for private equity, infrastructure funds and even major institutional investors, the risks associated with investing in developing economies stack up. “There is a real need to mobilise more risk capacity to meet the 2oC target ,” said HSBC’s Ross.

Taking risks

International Financial Institutions (IFI) and export credit agencies will play a major role in mobilising private finance and facilitating risk transfer in emerging markets and will also play an important role in generating projects on the other side of the equation. The cry from the market is often more about the dearth in supply of bankable projects rather than the ability to finance them. “It’s hard to find renewable projects in the emerging markets,” said Annette Eberhard, CEO of Danish export credit agency EKF. “If projects were there, then IFIs and ECAs could find a solution.”

EKF is a member of Climate Innovation Lab, which strives to identify instruments that have potential to drive investment in developing countries at scale. One such innovation is the Climate Investor One fund, which provides finance at all stages of an emerging markets renewables scheme: development equity, construction equity/senior debt and debt refinancing.

The IFIs also play a consultancy role with governments. “One of the key bottlenecks is the lack of investible projects,” said Thomas Maier, managing director for infrastructure at the EBRD. “The IFIs can help in project preparation by working with governments to prepare the right legal and regulatory framework and to get landmark projects going.”

They are also influential in the encouragement and expansion of local currency capital markets. They are regularly in the vanguard of bond market development, either issuing bonds into local markets or acting as anchor investors in new issues. That is particularly significant for the emerging markets where the IFIs, even with the introduction of a new wave of green and infrastructure specific development banks, still only represent some 15% of the infrastructure gap.

One such new bank on the block is the Asia Infrastructure Investment Bank (AIIB), which has been set up with a strong commitment to governance, accountability, procurement and environmental and social issues – as testified by its motto: “lean, clean and green”.

The AIIB will complement and co-operate with the existing development banks to address Asia’s considerable infrastructure needs. Asia is home to three of the top five CO2 emitting economies and 11 of the 20 most polluted cities in the world, according to the Asian Development Bank. It estimates that the region needs about US$800bn a year in infrastructure investment, equivalent to 6% of GDP. Investments are currently running at 2%-3% in many countries in the region.

The ADB is committed to playing a central role in financing the Sustainable Development Goals and, as such, it announced that it would double its annual climate financing to US$6bn by 2020. It recently approved a US$175m direct loan facility to six SPVs of renewable energy company Mytrah Energy India (MEIL) to help finance the development of a portfolio of new wind and solar projects. In addition to the loan, domestic commercial banks such as Power Finance Corp and SBI Capital are expected to participate in the commercial debt portion.

City slickers

As well as the undoubted need for investment in renewables and infrastructure on a case-by-case basis, perhaps it is the development of the sustainable or ‘smart’ cities that provides the greatest opportunity for addressing a new approach to living in a sustainable world. “Massive urbanisation can drive growth and efficiency,” said Melissa Roberts at McKinsey.

Cities are the driving force behind economic activity, wealth generation and lifting people out of poverty. Over half the world’s population is already living in urban areas and by 2050, estimates suggest that the proportion of people residing in cities will rise to 66% (UN Department of Economic and Social Affairs). By 2030, the world is projected to have 41 mega-cities, each with over 10 million inhabitants.

Cities are major hubs of economic growth but also the main culprits when it comes to resource consumption, congestion, pollution, inadequate or aging infrastructure and crime. Cities consume over two-thirds of the world’s energy and emit over 70% of the planet’s carbon dioxide, according to C40, the network of major cities committed to addressing climate change.

Designing a modern city to accommodate this expected migration sustainably requires an integrated approach to infrastructure; one that supports economic growth, conserves resources and reduces pollution. They are laboratories for a sustainable future, needing new approaches, new levels of planning and co-ordination and the use of new technologies to deliver to its citizens employment opportunities in a healthy, inclusive, energy efficient and pleasant environment.

There is no standardised approach to designing Smart Cities; each city has its own characteristics, its own competitive advantages and its own requirements. In developing countries, the rate of urbanisation is astronomical. The task has become one of building capacity in these rapidly expanding mega-cities in a planned and sustainable way, as opposed to the more recognisable and haphazard approach blighting some of the world’s biggest metropolises.

In developed countries, therefore, it is more about dealing with the problems of aging infrastructure and old design mistakes. In certain developing economies, it is more about how to build cities from scratch. There is a chance to learn from the mistakes and successes of other cities and make the most of new technologies to create a more harmonious environment in which people can still prosper.

Smart Cities are often associated with data and the overlay of IT. Data is a great way of managing behaviour; technology is relatively cheap and can lead to significant savings. For example, traffic monitoring can mitigate congestion, thereby speeding up traffic flow and reducing carbon emissions which, in turn, results in a benefit in healthcare. Data is also a way of interacting with inhabitants. Most people carry mobile phones, which can be used as a means of monitoring activity, and to access information as well as provide feedback.

Smart Cities, while hungry for data, are clearly not all about information technology. “Being smart is not just about smart meters,” said Graham Smith, head of bus rapid transit (BRT) financing at HSBC. “It’s also about renewable projects, energy efficiency, transport, lighting and more.” There are also structural challenges to any smart development, with different departments often responsible for different functions within the whole – public transport, waste, and water and energy provision, for instance. And each of these may have different budgets.

Co-ordination and collaboration are essential in developing a coherent, holistic strategy for a sustainable city. Co-ordination and collaboration are similarly essential on the financing side as the sustainability teams become more of an important feature in discussions within treasury departments. It is part of an overall change in mindset.

“It’s important to work with colleagues in the sustainability team as they have the experience to answer questions from investors on impact reporting,” said Borelius at the City of Gothenburg, an early adopter of Green bonds who launched his inaugural bond in 2013. “Money has an additional meaning in this instance. It’s not just about financial returns.”

Gothenburg is a frequent visitor to the Green bond market, an important mainstream instrument developed to explicitly finance the low-carbon transition. Borelius is planning to add to that supply with his fourth visit to the market in early June. And, despite being approached on many occasions for private placements, the city is keen to play its part in the development of the market by remaining in the public sphere. “We want to remain transparent,” said Borelius.

Being able to raise finance as a city entity is an obvious advantage when achieving scale for on-lending to projects that would be difficult to finance in their own right. “If the city is big enough, then raising funds through the Green bond market is relatively straightforward and could be part of the answer,” said HSBC’s Smith.

City financing is often complicated by budgets sitting in siloed departments with little incentive to accommodate the mutually inflicted consequences of misaligned decisions. There is also potential for conflict at the national level in determining the costs and benefits of large-scale infrastructure. Who gets the main benefit from the construction of a cross-country mainline railway, for instance, and who pays?

It all points to treating city development in a holistic fashion and then providing a template for financing that will eventually draw the private sector into commercially viable projects. Countries and cities need to be transparent in their sustainable development plans and committed to creating a sustainable financing climate.

Turkish delight

As well as funding from public finances and development banks, there needs to be sufficient security behind contract law and enforcement in order to attract debt and equity at levels that make project economically viable. Public-private partnerships (PPP) can then play a part.

Perhaps the recent experience of the healthcare sector in Turkey is one worthy of consideration. In 2013, the government revised its PPP laws in the healthcare sector to complement its ambitious plans to generate more bed spaces and improve facilities of existing capacity.

The law was based on the British PFI model, but tweaked to make investment as seductive and as attractive as possible for foreign companies. It includes, for example, coverage of foreign exchange risk using an indexation mechanism and a cap on performance deductions within the PPP contracts that effectively create a revenue guarantee to the project company. The legislation has worked and won plaudits as it effectively takes out the downside risk from lira depreciation, thereby improving the bankability of projects.

The deals have worked with the participation of development banks, such as the EBRD, and private sector domestic and international banks. The effort has been so successful that participants are coming up against capacity constraints and the search is on for new sources of debt and equity. Insurance companies are attracted by the long-term nature of the projects and the prospect of secure cash flows. Recycling loan risk into the bond markets is also likely (with some form of IFI guarantee); private equity, PFI specialists and international construction companies are also coming in at the equity end of the investment life cycle.

The hope is that, once proven to be successful, the model will be sufficient to leave in the hands of the commercial market as has been pretty much achieved in the case of northern European wind projects.

Best practice

There is still a great deal to be done before the wider market reaches that stage of maturity, but there are steps that can be taken as part of the process to bring about a quick transformation in mindset.

This could be through creating new financial vehicles, such as Green bonds and securitisation, which explicitly tackle the 2oC transition. But it is also important to massage existing instruments: incorporating climate change into benchmark indices and the considerations of credit rating agencies. “We must create a level playing field, for this the consideration of climate aspects in first-tier financial market actors, like credit rating agencies, can also help,” said Allianz.

US fund rating giant Morningstar announced in March that it will introduce ESG/sustainability ratings into its mainstream funds; MSCI has developed a new index and metrics designed to support sustainable impact among institutional investors; and S&P Dow Jones Indices has teamed up with RobecoSAM to launch an index designed to measure the performance of companies in its index with a weighting scheme based on an ESG score.

What everyone calls for, however, is more transparency and knowledge sharing in order to allocate resources efficiently, to benefit from best practice and to design out mistakes as early as possible. Much of this can be fulfilled at the political level. The IIGCC has called for governments to, among other things: provide meaningful carbon pricing, strengthen support for energy efficiency and renewables, support innovation in low-carbon technologies, phase out fossil-fuel subsidies, and ensure strategies are structured to deliver investment.

The debate on carbon pricing is not conclusive but removing subsidies is a popular call. Increased transparency is universally requested, such as transparency in procurement, although there are other areas in which transparency is important. In December 2015, the Financial Stability Board announced it was creating a Task Force on Climate-related Financial Disclosures (TCFD), with the intention to develop voluntary, consistent climate-related financial risk disclosures for use by companies in providing information to lenders, insurers, investors and other stakeholders.

The TFSD was tasked to make a co-ordinated assessment as to what constitutes an efficient set of disclosures on climate-related risks from which investment decisions can be more easily made. “Enhanced disclosures on climate-related risks that are used by investors, creditors, and underwriters can improve market pricing and transparency and thereby reduce the potential of large, abrupt corrections in asset values that can destabilise financial markets,” it said in its Phase 1 report.

Just as there is widespread agreement about the threats posed by climate change, there is also agreement that climate change will present material risks and opportunities in the business and financial communities. To reflect those risks and opportunities, financial markets need better access to information sets that are consistent and comparable.

“It is also helpful if governments define clearly their investment priorities and develop a long-term investment plan that allows all market participants to properly prepare for these projects while removing policy uncertainty,” said Allianz.

The removal of policy uncertainty is possibly one of the most important levers in directing private finance into financing the public good. “It is important to develop a reliable framework that establishes clear principles of how stakeholders will interact with each other and how risks will be allocated to the various parties … . regulatory certainty and stable investment conditions are key,” Allianz continued.

The political will to drive the transformation into a low-carbon, sustainable and socially encompassing economy is in place, the institutions are already established and private investors stand ready to finance that transition. It now becomes a question of how quickly co-ordination and collaboration will result in putting goodwill into good practice.

Explicitly green

The development of the Green bond market has been a bottoms-up phenomenon, driven by the requirements of a set of investors – mainly based in northern Europe and the US West Coast, who understand the importance and the economic benefits of the transition to a low-carbon economy.

Green bonds are issued under the umbrella of the Green Bond Principles (GBP), voluntary guidelines that recommend transparency and disclosure, and promote integrity. This ensures proceeds are directed specifically towards an environmental benefit, but the bonds are backed by the balance sheet of the issuer. The GBP have four main components: use of proceeds; project evaluation and selection; management of proceeds; and reporting. The intention is to move the market towards consistency.

The issuance process for bonds labelled as Green gives investors the confidence that funds are being used in a systematic and measurable way in order to contribute to their ethical, social and governance commitments. The option of utilising third-party verification, an independent assessment as to the use of funds and conformity to the principles underlining the transaction, is seen as an important feature of any deal. Transparency and reporting are of critical importance to the development of the market.

Moving the market towards consistency is an ongoing process. Climate Bonds Initiative has released a set of criteria across a range of asset classes to standardise the types of project that conform to climate change solutions. More sets of criteria will be published. “We’ve got to make the criteria granular,” said Sean Kidney, CEO and co-founder of CBI. “We need to make sure that investors really understand where the money is going.”

For the borrower, launching a bond with green certification comes with additional costs as the burden of transparency, the need for independent verification and certification add to the cost of issuing straight bonds. But the costs are not prohibitive and can be outweighed by the benefits of diversifying the investor base and gaining public exposure. There is also a knock-on effect in terms of mindset.

“Treasurers and finance managers are becoming champions of sustainability,” said Vikram Puppala of Sustainalytics, a sustainability research and analysis provider. “They want to get more involved and share their Green bond issuance experience, which is fantastic.” The first green bonds appeared in 2007 when the World Bank and the European Investment Bank tapped the market.

Since then the market has developed quickly, with issuance of bonds labelled Green reaching a high of almost US$42bn in 2015. The range of issuers and the type of security has expanded in line with the demand for these instruments.

In China, the development of the Green bond market has been driven from the top. At the end of 2015, the People’s Bank of China issued its Green Financial Bond Directive outlining the process for financial institutions to issue bonds and the qualifying assets against which they are measured. Domestic securities firms have been quick to take the hint and underwrote US$7.9bn-equivalent in Green bonds in the Chinese market in the first quarter of 2016, bring total global Green issuance to US$16.5bn, according to CBI. That is the biggest quarterly supply of green bonds to-date. “We hope to see US$100bn of green bond issuance this year,” said Kidney. “We’re aiming big.”

To see the digital version of this special report, please click here