IFR: Mark, from your position as a service provider to the banks, how do you respond to some of the issues that have come up so far? Do the issues we’ve discussed so far reflect the key themes you confront when you talk to clients?

Mark Rodrigues, Thomson Reuters: Yes. We’ve talked a lot about regulation and how that impacts business decisions and priorities and we’ve talked about funding, whether that is direct from shareholders or other markets, and the efficiency of the funding mechanism. But I want to start with the customer.

There was a time in this business not so long ago when capital was plentiful, the balance sheet mattered a lot and distribution mattered. Then of course, trust matters and relationships matter a lot. While some firms base their whole model on trust and relationships, others are more transactional.

So what has changed in terms of what people actually need? Is it discrete expertise around an industry? Is it the ability to structure deals, the ability to execute? Is it around efficient distribution? Is it unbundling? Or is it that people are still looking for a more comprehensive solution? Do sales and trading, research – all the things that were part of the true global model – still matter?

I’m seeing a lot of different bets being played out right now which have profound implications, including how you’re staffed and what kind of talent you need to put in front of the client. I would ask what actually matters to the client and work backwards from that.

IFR: Ted, do you want to respond to that?

Ted Moynihan, Oliver Wyman: I don’t think the fundamentals have changed that much. What we’re hearing around the table is a bunch of decisions have been made, banks have got a bit more disciplined about where they have an edge and where they can play because they have to in order to earn a decent return on the capital that they’re putting on the table.

There’s a lot more to come. I don’t think the behaviour of the clients is helping that much in this regard. If you look at the data, what’s happened in DCM or ECM underwriting situations is the number of banks on any deal has actually increased fairly significantly. The client is spreading its money around because they want to increase the number of financial providers at the table from something like five to seven, typically, to something like 10 to 13.

We talked about the mispricing point; what you’ve been seeing over the last couple of years is, despite all that pressure, the banks in many cases going to clients and saying: “we’d like to get onto your revolver” and clients saying: “great, we’ll spread the number of people on our revolver”. I don’t think right now we can depend on the behaviour of clients to help us make some of the tough decisions that still have to be made.

Saul Nathan, Morgan Stanley: That was very well put in the sense that we made a very good living before Glass-Steagall was repealed advising clients and raising capital for them without using our balance sheet in the form of long-term relationship lending. That all changed and it’s a very different competitive landscape. One big challenge is certainly the notion that clients are being presented with lending propositions from banks that are perhaps less adept, less well-equipped to provide them the kind of insight, advice, distribution, structuring, you name it that you talked about, and still feel the need to feed the relationship.

That dilutes economics, it dilutes value and it frankly dilutes the proposition of trying to do business. That is one of the big challenges – to William’s point – that both the client side and the provider side need to address over the next three to five years.

William Vereker, UBS: Clients want the same thing today as they wanted 10 years ago: they want good ideas, good advice, access to capital, and liquidity provision from their banking providers. And they want that as cheaply and as competitively from capable providers as they can get. So I don’t think we should rely on the clients changing their behaviour in order for us to change our behaviour.

We, as an industry, need to determine what businesses we are prepared to be involved with, where we’re going to put our capital, what the minimum returns are, and to be disciplined about that. If organisations consistently do that, then clients will ultimately change their behaviour. But what is happening to-date is that there are different levels of discipline from different providers on these topics. So clients are still able to have the best of all worlds by picking from different providers who don’t have the same levels of discipline.

John Langley, Barclays: The ‘Holy Grail’ here is trying to find the right balance between intellectual capital and financial capital. I don’t think anything has changed from the perspective of the needs of our clients. The notion of disaggregating products and services is not consistent with the way our clients think; we need to consider the client needs broadly.

For example, one of the more challenged areas from a capital perspective has been derivatives. But in order to continue to help clients to access pools of capital around the world, currency hedging forms a very important part of the overall discussion. It’s naïve to think that we can provide the fee-based services but not support their hedging requirements, for instance.

We certainly see those things becoming increasingly linked in certain client segments, so we need to take a portfolio approach to looking at returns. But this requires the discipline William talked about within the industry.

IFR: That said, Jim, thinking about the client solutions and client-service aspects of the debt financing business, because of the liquidity changes that have been wrought by regulatory change clients can’t expect the same level of provision. How has that changed the dialogue?

James Esposito, Goldman Sachs: I’d say extension of credit to our corporate client base is as important as ever. Extension of credit historically has been something that banks may have mispriced or may not have been as thoughtful as they could have been but most banks now are spending a lot of time thinking about what revolver commitments they want to go into, what the expectation is for pricing of that commitment in terms of the overall wallet share that’s available that they might participate in.

Extension of credit hasn’t changed materially in terms of the amounts that are being provided by the banking system to the corporate sector. But banks

are getting smarter about who they want to lend to and what the contract is between banking corporate if they’re going to enter into that revolver commitment. That’s been a healthy change for the banking system.

I think it’s important to point out we are talking about investment banking today, not the overall sales and trading part of the house. Investment banking is a very high ROE business; it typically generates some of the best returns that an overall commercial bank might make and that’s true even with the extension of credit, which many people think is a low ROE business. I’m not sure the banking system prices that as wrongly or perhaps as inaccurately as some might suggest because banking taken as a whole has been a high ROE business, which is why many banks are loathe to exit it.

IFR: But does it need to be run on an integrated basis? Where does componentisation come in? And why are we seeing this trend towards ‘boutiquisation’. There are lot of M&A guys particularly going out and setting up their own shops because they don’t need the securities business. What do you think that the proliferation of advisory boutiques is saying about the industry as a whole?

Sophie Javary, BNP Paribas: What it shows is the pressure which is being put on the system globally. In a very large organisation you have individuals who still see themselves as rainmakers and don’t want to face the transformation that we all have to deal with so I think it’s a question of the evolution of those individuals in particular.

However, our clients are global and there is a limit to what a boutique can offer in terms of the global access our clients want. To provide advice you need to have access to the capital markets, because if you are going to advise a large corporate to do a very large acquisition, if it cannot be financed, if the shareholders are going to react negatively, then it’s the wrong advice.

There is also a limit in the sense that you need to have the research and distribution side both on equity and debt to provide holistic advice so I think you’ll always see boutiques, but I think there is a limit to what they can provide.

James Esposito, Goldman Sachs: I agree with that, I can understand why someone who’s worked in the industry for 25 years, built up an incredible amount of expertise, built long-term relationships with corporate CEOs, has depth of experience around markets, could go to a boutique and be successful.

We probably won’t all be around long enough to see the results of this social experiment, but I’ll be really curious to see if that next-generation banker can grow up at a boutique and end up being dominant in terms of building relationships, because I don’t think they’ll have the same access to market expertise, knowledge, complex cross-border mergers.

In many ways, senior bankers are monetising the 25 years of expertise they’ve built up; that makes perfect sense to me; but I’m not sure that next generation of banker will be as successful if they grow up at a boutique, so that’ll be an interesting space to watch.

William Vereker, UBS: If you look at the 25 years I’ve been in the industry, this has been a pattern for the entire period of time. When there’s been a downturn in the industry, or there has been pressure on it for whatever reason, senior bankers have gone and set up boutiques and have been successful. It’s a viable business model and clients will always use them.

They go through a life cycle, reach the end of that life cycle, get absorbed back into banks again and the cycle begins again. We’ve seen a proliferation of boutiques. Some will do very well, others will do less well – like in any market – and I would expect to see the same pattern emerging again.

John Langley, Barclays: If your point, Keith, is around disruption within our business, I think

that’s right; I don’t think this is a new development. What is more interesting: the returns for the advisory and capital markets businesses are typically good. Where the challenges come is in terms of the costs

of the trading and sales infrastructure needed to support that origination model, and that’s where we could see more disruption from technology. That will be an important area of focus for banks going forward.

IFR: What do you mean specifically in terms of technology disruption? What’s the practical outplay of it?

John Langley, Barclays: When we look at the trading and sales businesses and compare and contrast what they look like versus maybe 10 or 15 years ago, there are clearly some very exciting developments that technology has helped to drive, so if we think about electronic trading, just as one example. But has technology truly driven down the cost to access markets or deliver products and services? I’m not sure that has fully materialised yet.

Saul Nathan, Morgan Stanley: That depends on your scale. I think it’s very expensive, as Jim alluded to, to run a global business in these sorts of arenas. It’s probably more expensive in Europe to run an investment bank than it is in the US because you have a product matrix, coverage matrix and country matrix; it’s complicated.

But if you take the technology piece, you have to be able to scale that technology over a big enough platform for it to make sense. The one question that is yet to be answered – and it is pretty interesting – is what does technology do to the investment banking side of the business? We’ve seen enormous strides in the sales and trading businesses in terms of creating connectivity with clients in ways that we’d never envisaged.

The investment banking side – the advisory and underwriting businesses – must be a new frontier for deeper technology penetration, and I think that is actually one of the quite exciting opportunities for the future in terms of how we recreate the industry.

Thomas Huertas, EY: Could I come back to the question of capital and emphasise that success depends on the capacity to respond, to have the capital available to put against the deals. If it gets stuck on the balance sheet, there is less capacity to respond to what the clients want; namely, immediacy of execution and certainty of execution. So having the extra capital and liquidity is essential to the success of the investment banking operation, at least in the integrated investment bank.

IFR: Staying with you, Thomas, investment banks, or banks generally, are trying to solve for the future in terms of responding to the regulatory framework that’s been set up, but one of the things that we haven’t seen as yet, despite the best efforts of the G20 and the FSB, is a level regulatory playing field.

We’re moving towards it in Europe, but certainly there’s a level of dysfunction at the regulatory level between the US and EU. How confident are you in predicting that we will get to some kind of global regulatory nirvana?

Thomas Huertas, EY: There is certainly a discrepancy between the US and EU. The traditional US view of convergence is: “if the rest of the world comes to our point of view, we can converge”. Europe is resisting that approach, and what we see in the mandatory clearing space is an example. I’m not confident that we will get to a solution to that any time soon, because it is ultimately a political question.

IFR: So does that un-level playing field pose a challenge to the industry, or is it actually an opportunity?

James Esposito, Goldman Sachs: The barriers to entry have never been higher in the global banking industry and so for new entrants into this marketplace it’s going to be that much more difficult to service a large-cap global corporate client. So, in many ways, while regulation puts challenges on our business, it’s lowered returns in the industry longer term, particularly when economic growth picks up. You’d have to be wildly optimistic about large banks’ prospects in the global investment banking industry, because it’s a very hard industry to break into right now because the regulatory burdens are quite significant.

IFR: Mark, one of the themes we hear a lot when we have industry conversations is do investment banks need to control everything they do in-house? Do you think that, bearing in mind discussions around disaggregation and non-banks being able to provide services as well as the banks at potentially better cost, this will play more fulsomely into the industry?

Mark Rodrigues, Thomson Reuters: There are a number of areas where there are alternatives to the banks. We’re being asked, for example, to participate in what I’d call the mutualisation of utilities. In the same way that there are deal databases to which everybody contributes because it impacts comp and bonuses so there are a number of firms – and we’re one of them – that broker transparency or standards.

We see the same kind of activity in areas like credit. Right now, there’s too much friction in the industry to allow any kind of risk transfer. So when people want to improve the balance sheet or get more leverage out of it without the attendant regulatory hit, when they want to securitise, hedge or insure in a different way, they can only do that if there’s transparency.

In the credit business right now, for example, we see an asset management industry that’s seeking alpha and is desperately looking for investable products with a decent risk return profile. And then the sell side of the business has all kinds of opportunities to originate and get into more deal flow, but is constrained by how much can be put on the balance sheet.

Doesn’t that present itself as an opportunity for further ways to structure credit and move it? Can it clear the market and can it move to the asset management space and to other long-term holders, like pension funds and others? It looks like an easy thing to do, but it’s just not happening.

There is still not a proper clearing mechanism for credit; it’s still got a lot of friction due to a lack of standards among other things. We’re seeing a lot of institutions coming together. Typically they are coming to us in groups of four or five. They are saying they would like us to lead an initiative because it’s in everybody’s benefit not to try to do it on an individual basis. This not only creates scale but also creates a better argument to regulators that it actually is economically priced and could move. We’re seeing more of this kind of co-operation and mutualisation than ever before.

James Esposito, Goldman Sachs: And there’ll be more of it. I would just cite things like on-boarding of new clients. We spend an inordinate amount of money on-boarding new clients every year and we like to think the way we do it is fit and proper and probably as good as anyone in the industry.

But is it really better than anyone else’s on-boarding service? Why couldn’t that become a utility-like function? So a client gets on-boarded by this utility function and we all have access to the same information about whether or not that person is an appropriate counterparty.

There are lots of places to take out the administrative cost and burden from the industry. Most banks now are using low-cost areas like India or Poland to outsource certain functions. I think the industry, again going back to the initial comments on lack of ROE, is getting laser-like focused on this topic. It’s true on the investment banking side; it’s true on the sales and trading side.

Ted Moynihan, Oliver Wyman: As William put it, if you step back a minute, the industry that was delivering pretty good returns has doubled to trebled the amount of capital it holds. There’s been huge focus on using that more efficiently but the only way out of that with there or thereabouts flat revenues is a massive reduction in the cost structure of the industry. There hasn’t been enough movement on that over the last three to four years.

Part of the reason for this on the back end is there has been some questioning about the game theory of that. If you’re a very large institution and you mutualise the cost, you’re potentially passing the benefits of scale to smaller players to access that. What we’ve seen over the last few years is a lot of the very large players saying: “there are places in which we were really aren’t actually getting any benefit of scale at all, so let’s engage in more of these things”.

That being said, complexity is also a problem for the banks. Ending up with a ‘Spaghetti Junction’ of new utilities feeding into their back office is not particularly helpful so I think there needs to be a lot of careful thought about where these things can really apply and where they can take off. There’s probably too many of them at the moment that are going down some blind alleys.

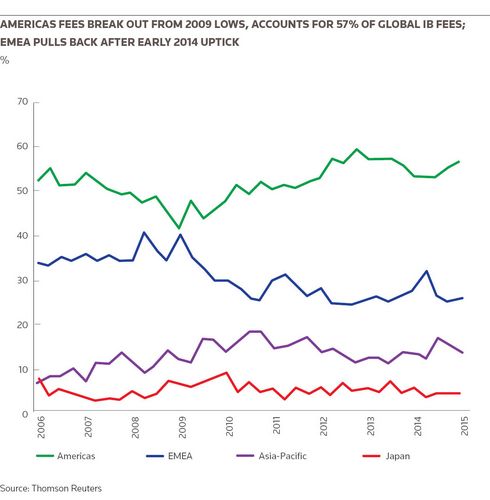

Sophie Javary, BNP Paribas: Regarding digitisation and technology for the IB business, yes, it’s a factor but another important factor is the digitisation of our client base. This element explains why EMEA is lagging. The US investment banking business has benefited from the tech digital cycle but this is at a far earlier stage in Europe.

So an opportunity in Europe that we are going to face is the development of the digital economy. When you look at the number of start-ups, investment banks that are able to cross the bridge between the large corporates and that extremely buoyant base of start-ups are going to make the difference.

This is where we have a very important role to play and it gives me optimism as to how we could see a larger pool of fees in EMEA. When we observe events such as Spotify’s private financing announcement earlier this year or more broadly the development of the venture capital industry in Europe, we can say that this is an area in which we all have a very useful role to play.

To see the digital version of this roundtable, please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com