IFR: Ingo, on this specific instance of competition between DCM and direct institutional lending, where insurance companies are getting quite aggressive and engaging directly with corporates, can they get the pricing piece right, given the various issues at play? More generally, is this development complementary or competitive?

Ingo Nolden, HSBC: I would certainly view this as an addition to the game. Insurance companies can provide long-term liquidity, in fact longer tenors than we can from a regulatory point of view. Banks will be pushed down the tenor curve more and more, that is very clear, but there is a gap. Maybe insurance companies or other institutional investors can fill it, so I think it’s above all good for the client.

But on the other side, insurance companies will also come to realise that we have something to bring to the table. Insurance companies are not in the market on a daily basis, they don’t know what the latest trends are; they might on the investor side but not on the origination side. Over time, even if they try to avoid originating banks in the first instance, there will be a time where we will add our value again, and they will realise why.

You touched on the Mittelstandanleihe market. There was no reputable bank active in this market and we all knew it was an accident waiting to happen. That was why the professional guys didn’t get involved. We have reputations to protect.

I see the direct lending bid as a complementary game, one that is very well established in the US where you have the US private placement market and no one complains about insurance companies taking market share from the banks. It has just evolved over time into a different market structure.

On Christian’s point about Pandora’s Box, everybody was talking about disintermediation 20-30 years ago, the 80/20 capital markets to loan funding split etc and we seem to be moving in this direction, maybe not exactly like we’ve seen in the US but a new market structure is evolving.

So you see all these different dynamics on the private placement side, be it Euro-PP in France,

GPP in Germany or the internationalisation of Schuldschein. Whatever you want to call it, it is all an expression of a different market structure evolving over time.

Matthias Gaab, Deutsche Bank: An interesting comparison came to mind when Ingo was speaking. In the bond market, the banks are active as intermediaries between issuers and investors whereas in the loan market there is no intermediary function. If you think it through, if there wasn’t an intermediary function in the bond market, would investors really be better off if I look at what life looks like on the lending side?

Apart from anything, issuers wouldn’t be able to deal with all those investors on a bilateral basis anyway in terms of capacity.

Roland Boehm, Commerzbank: Plus on top, if you look at the numbers I think disintermediation has happened but I am not sure as a phenomenon it is as much of a growth factor as it was in the years before. The bond markets are having a great year, but volumes in Germany are pretty much on a par with what they were last year.

Loans are up considerably while in EMEA [as of September 15] bond volumes are actually slightly below where they were this time last year. As a result I think we have found the right kind of balance and clients are taking advantage of that.

IFR: In terms of how you frame the various options, what are Schuldschein, Euro-PP or GPP subsets of? Are they subsets of the loan market? Are they loan substitutes? Are they bond substitutes or alternatives? At the end of the day, a negotiated private placement is a loan isn’t it?

Roland Boehm, Commerzbank: We had a very interesting panel at the LMA Conference in London on that topic. It is a bit of both and again, coming back to the point earlier, we need to stop thinking purely in product categories and think in terms of solutions that we provide our clients.

I think Schuldscheine have certainly found a niche. But it’s not a huge market: roughly €6bn year-to-date against €577bn in EMEA in the loan market. So it is not a huge market but it is flexible and agile and it brings new investors into the market. So I think it serves both the bond and the loan market in providing something new.

The European private placement market is really starting to take off in many different ways, shapes and forms. That’s exciting and I think beneficial for clients. We do need to be very careful about providing too many fragmented alternatives for borrowers or investors. But at the end of the day let’s get it out there and clients will decide what they want to use.

Christian Reusch, UniCredit: Why are we increasingly seeing things like private placements and international Schuldschein? Put yourselves into the shoes of a pension fund, an insurance company or any other fund manager. You have piles of cash available for investment and unfortunately there is not sufficient supply coming to the market to cope with their needs.

Diversification is a topic that a lot of people are preaching, especially in Germany, That’s why we see the internationalisation of Schuldschein. If you can find people to accommodate German law, it’s fine and from that perspective it doesn’t bring too many headaches to the table.

That’s why those PP formats are gaining more and more relevance for investors. The overall allocation they receive in benchmark transactions is not that big. Plus, the liquidity, which was always an argument for benchmark transactions, isn’t that big either. So putting these factors together, they figure they can dedicate more time in looking at transactions where they have some sort of exclusivity.

In other words, they put themselves into competition with one or two others, but not with 100 or 200 or 300. That’s certainly an argument which I buy into from an investor’s perspective, because you get the allocation you want. You have to deal with all the other risks but I think that’s already on their minds when taking the investment decision.

Joachim Erdle, LBBW: Maybe just to add one aspect here, if you will allow me. It’s not only a question about whether it’s part of the capital market or the loan market. I think it’s more important that as a bank you’re able to offer the whole range of products to the client and then advise them in a way that they can decide on their preferred structure. There are advantages and disadvantages to all products, but as a bank you need to be in a position to offer the whole range of products and then advise the client in a most efficient way.

IFR: That’s fine if you’re Bayer or Volkswagen and have a sophisticated treasury operation. When it comes to the less sophisticated corporates, is there a point about the extent to which it’s a good idea to let the client choose? If you go to clients and say: “Listen, I’m not a product guy, I’m your financing guy. I can offer you long tenors in the bond market. I can offer Schuldschein, I can offer you a negotiated private placement, I can show you my balance sheet”, whatever. Clients are certainly spoiled for choice but do you end up confusing them? How do they choose? What is the deciding factor in all of this? Pricing?

Joachim Erdle, LBBW: It’s not price anymore, because prices are very transparent. I think it’s more important to come up with customised structures. The structure certainly includes terms, tenor etc but you’ve got to bear in mind the full financing of the entire company. This is a very important aspect.

And it’s one of the reasons we’ve added advisory units to our corporate loan and leveraged finance departments. Because we try to advise corporates independently. We want to have the best solution for the client, and it’s that that drives the relationship with the client.

It is not a question of whether we want to sell a certain product, the key is to come up with the right structure and advise the client. For some of them price is important, for others it is complexity and for others it is tenor or other aspects; it depends on the individual situation.

IFR: Fine, but all of that said, banks are fiercely tribal in terms of how they are organised. So how does the client, who is at the centre of this financing universe, deal with the fact that you are ultimately product originators? That’s the reality of life. Is it a problem? Do the banks need to evolve in how they cover clients? Isn’t it better to have a client coverage guy at the centre of the financing relationship dealing with origination?

Matthias Gaab: The debate between product and relationship is ongoing for each of us. But just a comment on what Joachim was saying, basically the beauty of our jobs is that we have this advisory function, where we’re in a position to explain the whole range of options available, which as you say is pretty big.

Then in an iterative discussion between ourselves and our clients, we come up with results. The result needs to be a solution where clients find their needs across all aspects taken care of. Those needs will vary from client to client, even if they are in the same industry.

Then it’s also a matter of crossing the bridge internally to say: “well the product I had in mind is probably not exactly the one that serves the best interest of the client, at least not in the medium term”. It needs to be a discussion with other guys internally. As a product person, the relationship person plays a pivotal role in order to get it all across and bring the product originators into the discussion mode in a solutions-orientated context.

That is the key thing. I’ve been doing this for quite a few years now and I know a lot of clients personally but I’m on the product side so I speak to some clients now and then only whereas the relationship person is the one who, depending on deal flow and all sorts of other aspects, talks to the client on a very frequent basis.

As a product person, I rely on a relationship person to tell me where they sense the need in order to get engaged in the discussion. They rely on the product people to give them guidance and to set up a discussion, let’s say on the debt side, with other product colleagues to have a solutions-orientated discussion.

IFR: OK but that said, at the product level, you still have to make budget.

Roland Boehm, Commerzbank: I can make this very easy for our institution. We engage in client-focused origination and the client relationship manager plays a key role here. Their job is not only to keep the client happy but to make sure that we do not have a product push situation, and that we seek to find the right solution for our clients.

At the end of the day, regardless of how an institution is set up, I think that in the phase that we are in and with the competitive dynamic being what it is, you can only get it wrong once. If you have tarnished your reputation with particular clients, they are going to use someone else to solve their problems going forward. That is an incredible incentive for banks to get this right. You do not want to push the wrong thing to the wrong client at the wrong time.

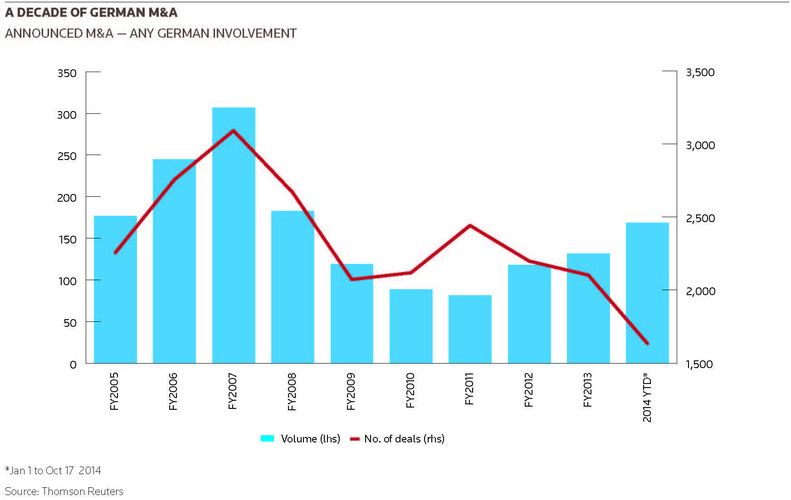

IFR: I wanted to put a bit more focus on the M&A story in Germany and the extent to which you as a panel think that that is going to be a driver of new business in 2015. We’ve seen some pretty chunky German deals year-to-date across industry sectors. Are you factoring in M&A as bigger piece, be it corporate M&A, be it sponsor-driven? And will activity be out-bound, in-bound, domestic?

Joachim Erdle, LBBW: In terms of M&A, you’re right, we have seen an increase in volume in Germany but not in the number of deals. We saw a huge increase in the M&A dynamic in the second quarter. Big takeovers have been announced and this will definitely drive financing markets.

Looking forward, the large caps as we’ve said, have piled liquidity onto their balance sheets so they need to do something. Plus, companies that do deals put pressure on competitors so other corporates will need to take decisions in terms of acquiring other companies as well. So I’m positive in terms of M&A volume in Germany. I’m also very positive that we will also benefit from that from a financing perspective.

IFR: Ingo how does it look from a bond market perspective? There’s been a very good take-up for M&A transactions.

Ingo Nolden, HSBC: Indeed, hoped-for M&A has been an evergreen topic for everyone for around five years but we’re now seeing some very tangible evidence in terms of large deals, whether it’s Bayer, ZF Friedrichshafen [which bought TRW Automotive Holdings for US$12.9bn] or the telecom space, where there’s a lot happening. When you look into the telecom sector, the next logical step is likely to be pan-European consolidation i.e. cross border. It seems there is a bit of industry consolidation in play. CEOs and CFOs are going to come under immense pressure to do something.

At shareholders’ meetings, everybody is asking companies: “what are you going to do with the cash? If you don’t find any investment opportunities, give it back to us in an extra dividend or start a share buy-back”. Which is not a very good use of the resources they have. So liquidity needs to be put to work, we’re seeing green shoots in the large-cap space and the bond market is very supportive. In fact, liquidity is so abundant that I don’t foresee any issues financing M&A activity.

Also, the deals we’ve seen so far have been structured relatively defensively, certainly in the corporate space; you might argue slightly different in the leveraged market. But the corporate trades in the pipeline are decently structured and not very risky.

Christian Reusch, UniCredit: But even though the conditions for financing these activities are better than they’ve ever been, you still need to find opportunities to put your money to work. Last year was a great year; 2014 is heading in a similar direction now. The question is: what opportunities are still out there which make sense economically.

That’s probably the only hindering factor I see. Certainly I see no issues financing trades; nor is it a problem taking them out in the capital markets. The numbers speak for themselves. Even in the unrated space, just shedding a bit of light into that, the unrated bond market has evolved significantly to more than double or triple the volumes we saw last year. But for me the M&A story is about opportunities.

IFR: So financing will be available. But given the liquidity available in the bond market and the competition for funding, will we see a differentiated approach to acquisition financing if we do get an uptake in M&A in the next year in terms of deal structuring and the take-out piece? Or is it a given that the initial financing will always be bank-driven?

Roland Boehm, Commerzbank: In most cases yes, the initial financing will be bank-driven, since the loan market offers the agility, the speed and the discretion that other markets simply can’t match. We will continue to see the loan market being the first point of contact for these situations.

The beauty is, however, that with the bond and equity markets being as strong as they are, the Schuldschein market becoming more active and also, by the way, bank financing becoming much more of an alternative over the last 12 months, clients have an enormous amount of reach in being able to complete acquisitions. It also gives them an unprecedented level of execution certainty that we simply did not have before.

So I agree with Christian: the question is going to be finding a target with multiples that are worth investing in. Be it for an LBO investor or a corporate investor, financing conditions have never been better.

Matthias Gaab, Deutsche Bank: I agree and I’d say the reason why in acquisition scenarios you can’t do without a first commitment via bank loans is because usually deals are subject to certain closing conditions. Not least cartel issues and at that point in time, even though there are deal-contingent structures in bonds and other markets, it is probably hard to go for capital market issuance as long as you perceive or you believe that the risk of the non-closing, depending on the cartel issues or other issues, is high.

You only get an underwriting commitment without de-risking for a certain period after announcement following which one can and should do early take-outs. There was a time, in the heyday of 2007, when nobody considered a take-out before the closing, which is something which you see more often now. You can debate whether this was prompted by the banks not wanting to fund once closing occurs or whether it was done on its own merits at the time, but I don’t recall deal contingent structures being in place so that might be another reason why being innovative, as Christian pointed out earlier, continues to be very important.

But it’s worth pointing out – and this is something for capital market colleagues around the table to comment on – that there have been times when the bond market has been shut even for large-caps and not just for weeks, for months. Mind you, that seems to be very long time ago and all of the acquisition finance we’re doing now is certainly hinging on the fact that liquidity is available and will continue to be there to take the initial financing out at whatever point in time is appropriate.

Given the current liquidity in the market and ECB policy, I can’t foresee that changing any time soon. But it will change at some point in time and it will have repercussions on acquisition financing, given the limitations we are all under as a result of new banking regulations. That’s going to be interesting so from that perspective it’s probably not a bad time for companies to consider doing deals now even though in some cases valuations are relatively high, because as Roland and others have pointed out already, funding costs are impressively low.

IFR: What about the LBO market. Will this pick up next year?

Joachim Erdle, LBBW: Definitely. The financial sponsors have been very successful in fundraising over the last 12 to 18 months so they’re managing a lot of liquidity too which they need to put to work. But I’d say in the current M&A market you will hardly find a company at an attractive price level. They’re expensive so if a company is attractive you have to pay full price for it. That’s when the interesting discussions will start again, around whether strategic buyers, private equity companies or family offices are positioned to pay the highest price.

In terms of leveraged buyouts I am definitely convinced that PEs will maintain, if not increase their market share. They need to be active, they need to show performance as well and for them it’s the right place at the right time to put money to work.

IFR: If we do see a re-emergence of leveraged buyouts, Roland, what would be your sense of the amount of leverage banks will be willing to provide? Before the crisis, deals were being done with pretty high leverage and then we came right down. The perceived wisdom is that that kind of leverage is not going to come back. Having said that, bearing in mind the competitive issues that we have been talking about, do you sense a creep back to higher leverage?

Roland Boehm, Commerzbank: First of all, I do not think there is a ‘number’ or a ‘leverage multiple’ at which banks or investors generally feel comfortable. One of the takeaways from the crisis, and I do think there has been diligence in this, is that people take a much closer look at the actual company itself. One of the lessons banks have learned is underwriting is not just a label you stick onto something. You may actually own that underwrite so it should be a business model that you think is sustainable.

Secondly, following on from this, certain companies and certain businesses can accommodate more leverage. That is part of where we are going to see increased activity in the LBO space – finding comfort and the right levels of leverage for transactions on a case-by-case basis according to their respective credit stories.

Thirdly, I think we are starting to see a variety of instruments come back into play to accommodate LBOs. Be it second liens, be it high-yield bonds (I am very glad, by the way, to see such strong use of this product), or be it the term loan B product that has come from the US. I think it is very good for the market, that we have seen that alternatives in this market space grow considerably in Europe.

Finally it is not only about the leverage multiple, it is about finding the right investor group to take a particular risk. That is probably more of an art than a science.

To continue reading this roundtable, click the relevant section. Introduction - Participants - Part 1 - Part 2 - Part 3

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

| German Corporate Capital Markets - Debt raised by German corporates (excluding financials) | ||||||

|---|---|---|---|---|---|---|

| Investment-grade debt | High Yield Bonds | Syndicated Loans | ||||

| Issue date | Amount (US$m) | No. of issues | Amount (US$m) | No. of issues | Amount (US$m) | No. of issues |

| Full-year 2013 | 57,420.30 | 122 | 26,759.10 | 30 | 121,974.90 | 164 |

| Jan 1 to Oct 17 2013 | 49,402.70 | 97 | 21,933.00 | 22 | 88,391.30 | 118 |

| Jan 1 to Oct 17 2014 | 51,549.40 | 107 | 13,226.90 | 15 | 133,124.40 | 123 |

| YoY% change | 4.3 | 10.3 | –39.7 | –31.8 | 50.6 | 4.2 |

| Source: Thomson Reuters | ||||||