To view the digital version of this report please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

IFR: Welcome to IFR’s third German Corporate Funding Roundtable. The objective of this session is to review activity year to date, glean some ideas from you about the current level of activity in capital markets as it pertains to German borrowers but also to understand your expectations for growth in the months ahead. Roland, can you give us your thoughts on the market to date, whether it’s met with your expectations, whether you have been surprised by any developments?

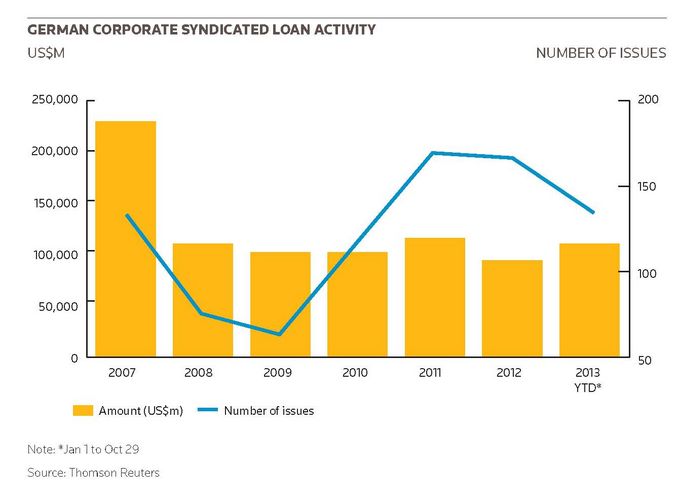

Roland Boehm, Commerzbank: Thank you very much, Keith. We have had another strong year in Germany, albeit from the loan perspective at a fairly low level. There is certainly room to grow and the good news is that the market is as open as it’s been for many years. Underwriting capacity is available for corporate activity, particularly in the EMEA space. As banks, we are more than happy to support clients in the next stage of their development.

If I look at where we are now compared to this time last year, there is a real feeling in the German market but also in the wider European market that people have stopped looking back. We are looking ahead and sentiment is good. Banks are open for business. The German market has always been competitive and it continues to be. So we are in a pretty good place.

We also need to remember that no capital markets activity is more closely correlated to economic activity than the loan market. Growth in the loan market will pick up very naturally as soon as companies start expanding. I would love to hear what Henner has to say in this context.

Finally, when you buy Germany, you are essentially buying “global”. As soon as we see growth and expansion accelerate, we will see volumes increase further. The refinancing market essentially isn’t fresh money; it’s recycling something that’s already there.

Paul Kuhn, BayernLB: I agree. Whether you look at the investor space or the bank space, the market environment is excellent and there is a lot of liquidity but there’s been a significant reduction in financing requirements on the borrower side. Corporates did their homework in 2009/2010. We haven’t seen much M&A activity kicking in but we did see a lot of refinancing in 2012, including of 2013 maturities. A lot of parameters have made the environment a very favourable one for borrowers; less so for investors.

You can see that across the loan product, in Schuldschein and in the bond market too where there’s been a significant reduction in spread levels. But we’ve also seen a very strong recovery in default rates, which offers investors additional comfort. But in summary, the environment is split into a good world for borrowers and a difficult environment for investors and banks.

IFR: Where are we in the refinancing cycle in Germany? Is there still a lot to be done?

Paul Kuhn, BayernLB: A lot has been done already so we’ve seen a significant reduction in financing this year. Obviously we will see loans, Schuldschein and bonds maturing next year but if you compare total volumes this year to previous years, I’d say this year has been a pretty good one but volumes aren’t going to increase that much. It’s going to be continuously good environment and the market is liquid. There will be deals completed, but a significant, 30%-50% increase is not on the horizon.

IFR: Matthias, do you concur with comments so far? Last year, there was an expectation – or perhaps we should call it a hope – that there would be a pick-up in event- driven activity. But as Paul alluded, we haven’t really seen that. Can you talk about that aspect?

Matthias Gaab, Deutsche Bank: Looking back at the past nine months, I’ve been surprised on the loan side by the relatively low level of activity, especially at the beginning of the second quarter. But I’ve been equally surprised at how business picked up after the summer break. We’ve seen significant numbers and refinancing demand while pricing has come down dramatically. The volatility between the second quarter and the end of the third quarter has been pretty surprising. So the year has been quite differentiated; a tale of two halves.

On the bond side, corporate issuance volumes in the first nine months have been more or less flat relative to last year. That’s another surprise from my perspective since I would have thought that people would have taken better advantage of low spreads and what they could achieve on coupon levels. For example, Deutsche Post’s recent €500m five-year tranche came at 43bp over mid-swaps and that’s for a Triple B name.

I agree with the comments made already that unfortunately there is little demand from the borrower side because issuers have cleaned up their balance sheets and for the time being don’t look overly inclined to secure those low coupons.

IFR: Joachim, pricing has been mentioned already. When we see this pick-up in economic activity, how do you think pricing will evolve? And do you think we’ll be stuck in this current low pricing cycle for the foreseeable future?

Joachim Erdle, LBBW: I think we’ll be stuck in this low pricing environment for the next year. At least that’s our expectation. But perhaps more importantly, there’s been competition around other terms and conditions. We’ve seen very generous financial covenants, for example. In fact, we’ve seen the first no-covenant deals in the mid-cap market, which is a very interesting development. And we’re seeing wash-out in other terms and conditions, which I think will characterise the market we face in 2014.

IFR: When you say an interesting development, do you mean a dangerous one?

Joachim Erdle, LBBW: From a risk management perspective, it is dangerous for sure. But on the other hand the market’s the market and we have to deal with it. Are we happy seeing a lot of important risk-management factors go away, given our strong focus on the German Mittelstand? Definitely not. The impact of this will be seen in the next crisis.

That said, I think it’s fair enough for corporates to take advantage of the environment. One needs to look carefully at the overall strategy of the bank. For clients, it’s more important to have a reliable bank than a bank that gets nervous because they’re unsure about what’s going to happen.

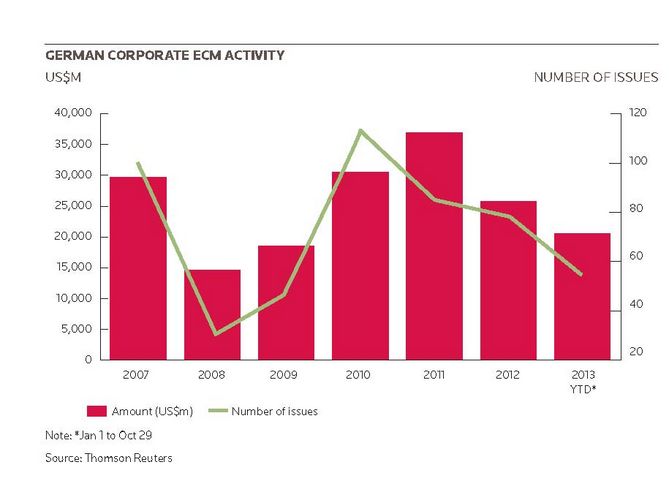

IFR: Let’s move to a review of the bond market. Christian: Matthias already mentioned that he was quite surprised that issuance volumes hadn’t picked up to the extent he expected, given the very positive technical conditions for borrowers. Can you give us an update on year-to-date activity from German corporates and provide some thoughts about it?

Christian Reusch, UniCredit: I agree with the point about volumes, but I would add to that the number of issuers and issues has increased and granularity has gone up significantly. We’ve seen a variety of non-rated names come to the market as well as the major issuers and there’ve been a lot of debut issuers and that is a positive, It’s a signal of the health of the firms coming to the market. It’s also a reflection of the fact that a lot of institutional investors are hunting for yield and investment alternatives. That further fuels the tightening of spreads. But I would say that after several years we’ve seen the bottom in overall cost of funding.

In fact, tighter spreads have to some extent been counterbalanced by a slight increase in overall yields. But as long as the cycle and the economic environment look as favourable as they do, the current situation looks it’s here for a little longer. From an outlook perspective. I think the next 12 months will be as interesting as the last 12. I think supply will be more or less at the same level but the number of issues will be stable to slightly higher.

I would not rule out spreads going even tighter but from an overall cost of funds perspective, I think we have seen the bottom: 1½% for five years (using the Deutsche Post example) is the lowest coupon we have seen for quite a time. I think from a treasurer’s perspective it is also a question of OK, you can always optimise a little bit on the margin. You could probably also go short in the CP market and get money more or less for free.

So from that perspective there is always a way to further, let’s say, optimise your funding structure. But I think we have, at the moment, a situation that from the short to the very long end of the curve, even for lower rating classes, there is a high receptiveness.

Ulrich Hoeck, Commerzbank: Something I find surprising is that German treasurers haven’t needed to go outside of the euro, which is a demonstration of the strength of the German market. I had expected activity to be more non-euro biased. We have seen some of the big issuers going to the dollar market, both in Eurodollar and 144A format, but the rest of the German issuing community has been best serviced by staying in its home currency. That tells me a lot about why it’s such a good market.

IFR: Henner, let me come to you. You have heard the reviews to-date. You have all of the pricing power and hold a lot of the aces. How have you played into this as a borrower?

Henner Boettcher, HeidelbergCement: We obviously like it a lot. There are a lot of new players coming into the German bank market, which is bringing down pricing but we’re also seeing documentation requirements loosening. HeidelbergCement is a sub-investment grade borrower and it’s surprising to hear what some players are prepared to do.

Covenant free isn’t just a topic for mid-cap clients, it’s for crossover clients now as well. We haven’t acted so far but we’re listening and observing. Terms and conditions continue to be favourable and we expect they will be going forward as well.

IFR: Are you tempted to be opportunistic in your borrowing?

Henner Boettcher, HeidelbergCement: Yes, I am.

IFR: I’m curious to understand the mindset of a borrower. How far forward do you project? Do you look at pricing on a cyclical basis? How do you play into the specifics?

Henner Boettcher, HeidelbergCement: We do look forward. We have a three-year facility out now which falls due in 2015. So next year we will do something, that’s clear. But we didn’t want to take on the full P&L charge of doing something earlier than that because we don’t think the pricing advantage we could realise right now would justify moving now over waiting another year or two.

It doesn’t make sense for us to issue now to obtain very favourable terms and conditions just to deposit the funds at negative rates in the bank. We think the market will remain very positive so there is no need to rush in the bond market. We look about 24 months ahead; that’s our policy

IFR: Back to Christian’s point, do you think pricing has hit a bottom?

Henner Boettcher, HeidelbergCement: If you look at it from a bond yield perspective I tend to agree with him but we look at the credit spread since we always look at funding on a floating-rate basis.

Roland Boehm, Commerzbank: Keith if I may, just picking up on what Henner said, he made a very important point. I think we focus too much on pricing. Pricing is in many respects a technical point. There is competitive pressure, there’s supply and demand. Pricing is what it is at the end of the day and some players will react on an opportunistic basis to it, others follow a plan.

We have got to take a step back and see what’s actually happening. Let’s not forget that we are coming out of probably the biggest crisis since the Second World War. Germany not only had safe-haven status during most of the crisis in Europe but was able to consolidate that. Based on what Christian and Ulrich said as well, a lot of borrowers actually diversified in terms of the products and instruments they use. We’re actually seeing real growth in capital markets activities.

Most clients think in terms of solutions and not in terms of products. I think if you look at the growth in sophistication and reach like we’ve seen on the corporate side over the last three to four years, it’s been phenomenal. That’s really the story.

Paul Kuhn, BayernLB: I agree with Roland that we have an excellent environment. But on the other side, as we’ve been hearing, there is no need for any real rush on decisions. There’s no need pointlessly to suck in a lot of liquidity and as Henner said, companies focusing on the structure of their balance sheet don’t want to have negative carry for that long.

That’s why there is a limitation in market activity: people are expecting the current great environment to continue. Hence there is no need to rush. Everybody is relaxed in that regard and takes things as they come and needs develop.

IFR: One of the big talking points both within Germany and among a lot of international borrowers has been the Schuldschein market. The expectation at a discussion earlier this year when I came and chaired a Schuldschein roundtable was that growth would be slower over the course of this year and there would be fewer international borrowers accessing the market. Matthias, how has the Schuldschein market developed this year on the corporate side?

Matthias Gaab, Deutsche Bank: The market has developed favourably and especially on the international side has outperformed, initial expectations. We shouldn’t forget although that the product is located in various departments depending on the bank, but at the end of the day it’s a loan.

That speaks to where it is going to be placed, i.e. who the investors are. Increasing the interest of international issuers in Schuldschein is certainly attractive to the investor base because they wouldn’t otherwise have the possibility to lend to those names. That’s the key reason why the product has taken off.

Henner Boettcher, HeidelbergCement: For borrowers it’s definitely a big plus. Before it was more or less just a German product, but now international banks that are not part of our loan group are calling us and play between bonds and Schuldschein. We just look at what’s better priced and that’s what we issue because the terms and conditions are absolutely the same.

Roland Boehm, Commerzbank: It’s a great entry product for new players into the capital markets.

As we see the bond market grow and develop, and as Christian mentioned, the number of new issuers and the granularity in the bond market, the uptake of new names will largely come into the market through Schuldschein.

It’s a relatively small market and I think it will remain so for the next few years. However it is an exciting product space. Because it’s growing, you are entering new territory; you are seeing new investors and new borrowers. There is huge potential.

Christian Reusch, UniCredit: What’s been interesting in the Schuldschein market is the availability of longer tenors. It’s moving away from the classic three to five-year usual suspects on the investor side, more to seven or 10 years and selectively even longer than that depending on name and industry. Nevertheless this is also a positive trend from a borrower’s perspective and is offering an interesting alternative.

Roland Boehm, Commerzbank: And maybe a basis for a private placement market to develop. It’s a great platform for that. So there are multiple uses for this product.

Henner Boettcher, HeidelbergCement: What you must not forget with the Schuldschein market is that you have this put which is free where the bond market demands a premium for it. This is now fully accepted by lenders that you can actually exercise that put.

Christian Reusch, UniCredit: I agree but I would say that some investors have realised that in the meantime and it’s left a bitter taste. But if there aren’t that many alternatives, you have to swallow it.

Paul Kuhn, BayernLB: I think there is also a correlation between current spread levels and that issue, because I’m sure investors would care about it in the event of the significantly higher spreads we would have if we went into another crisis. But right now they don’t worry about it because how much lower can spreads go? We are already at very low levels and there is no expectation that you would call today if you’ve financed something for five years. You would not call and pre-pay tomorrow next year, or anytime soon. That’s why they don’t fear that situation right now. But if we saw higher spread levels, that fear would definitely come back again. The longer we have as of today with regard to maturities, the more likely investors will choose fixed-rate, for that particular reason I guess.

Joachim Erdle, LBBW: One question to you Henner. How important is it for you that banks or potential financing partners offer you loans, bonds, Schuldschein or whatever? Is it important to get it all from one provider or is it something where you can differentiate?

Henner Boettcher, HeidelbergCement: The balance sheet commitment is the entry card for all other products. So you will never see anyone doing a Schuldschein for us who is not part of our syndicate.

IFR: Staying with you, Joachim, how are borrowers generally playing this market environment? Are they tending to go for the cheapest option or are they looking a bit more strategically?

Joachim Erdle, LBBW: First of all borrowers rate their financing partners so it’s important to come up with a product mix accompanied by aggressive pricing. But it’s also about the general approach banks take towards their borrowers. Financing partners also need to have a sustainable approach, which is very important. Borrowers can then start to differentiate the various banks depending on whether they fit into that infrastructure or not.

Tenor is also important; having Schuldschein with a tenor of seven or 10 years is something banks don’t want to offer on the loan side. So the combination of both is important. That’s why I’m interested to understand how important it is that partners offer a mix.

Finally, it comes down to pricing sure. Treasurers focus on margins and we need to deal with that, but it’s important to find a balance. If you look at the partnership on a long-term perspective, it’s very important to have an open dialogue, to have someone around with a reliable, long-term approach to the market.

IFR: For mid-cap borrowers in particular, there is a lot of documentation and transparency required to issue bonds that some maybe issuers are not used to. Ulrich, is your expectation going forward that German mid-cap issuers will look more to the bond market? How does the increase in yields, which we are going to perhaps see over the cycle, change the dynamic?

Ulrich Hoeck, Commerzbank: The rules for approaching bond investors are the same whether you are Siemens, HeidelbergCement or a German SME. Some of the rules are defined by exchanges in connection with listing; others are built into the capital markets law. The bigger companies are better informed, through simple experience, but there needs to be a process of knowledge transformation, which is where bankers come in.

At that point, everybody who is willing and able – I think these are the two key components – to commit to the rules of the game has an open door to the bond market because the market is as desperate for HeidelbergCement as it is for Daimler as it is for an SME. In terms of (a) size and (b) hurdles to be jumped Schuldschein has easier documentation so this is most likely the first avenue after you have done bilateral credit and a syndicated loan.

To continue reading this roundtable, click the relevant section. Introduction - Participants - Part 1 - Part 2 - Part 3