IFR: Franz-Josef, Rafael makes a good point. Every argument has two sides. How does the current status quo influence the way that you approach your job?

Franz-Josef Kaufmann, Commerzbank: It’s very interesting following the different opinions. I’m closer in my view to Rafael. In my various conversations with the Bundesbank, I have the impression that the Eurosystem wants to be seen as an investor and we, as the market, we as issuers, should see them as such.

As Rafael said, we remember times when we had one or two investors placing significant orders and they pushed hard at that time with regard to allocations. I have the impression the Eurosystem is not doing so now. My recommendation: treat them as an investor and see whether they want to behave like an investor.

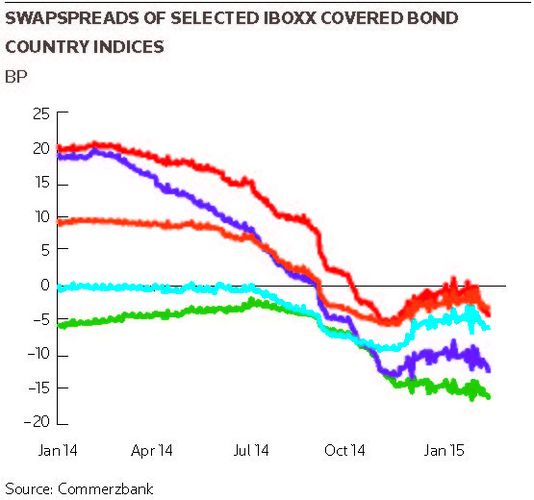

There has been certain developments since the start of the covered bond purchase programme and maybe today the Eurosystem is at a different point than where it was a few months ago. One should think about that. Indeed, I believe the overall discussion is also very much driven by the fact that we have some extraordinary situations. We have absolute yields close to zero, a level we have never experienced in Germany or in Euroland and we have spreads for most products, especially Pfandbriefe, at historic lows.

Having an additional investor and additional demand moving spreads even tighter on top of that clearly creates a challenging situation for investors: they search for spread – no spread there; they search for absolute return – no absolute return there. We know that demand from one investor is there and very likely will be there for quite a while and we don’t foresee that changing.

As an issuer, you need to take that as it is. We are paid to engineer the best result for our company as an issuer so when we tap markets, we need to see how we can handle that in the best way to get the best outcome for us as an issuer. The final spread we pay is probably not the only measurement; there are other aspects that also play into that equation.

So looking into the beginning of the year and the first covered bonds, the market looks more healthy when looking purely at the way the deals get placed in the market, get accepted by the market, get handled by all participants. That’s my impression up to now.

Jörg Huber, LBBW: Can I some in here? Yes, the ECB is there and they are putting orders in, but we use this word ‘investor’ the whole time. We need to be aware that the ECB is not an investor. When we talk about investors in the past who were putting in big orders, they were investing their reserves, they were pension funds were investing the money.

The ECB isn’t investing its money; it’s just pushing money into the system. There’s a big difference. Of course it helps us achieve fantastic spread levels, fantastic yield levels but it’s artificial. We should not forget this.

Rafael Scholz, Münchener Hyp: Yes, there is a difference. You call it ‘investor in brackets’; I call it ‘investor’ and ‘typical investor’. I have no indication that bonds bought by the ECB purchase programme will be sold but that is the case by a typical investor because the investor is always able to sell. We know what happened after 2008 with all those huge positions in several investor portfolios. From that perspective, the ECB is a great investor, to be honest and I disagree with Bodo. Yes, I never crowd out any typical investor but if you are looking for stable, long-term funding, the ECB is a perfect investor.

Jens Tolckmitt, VDP: Maybe it’s the role of someone from an association to take the longer-term view. I’ve already said I don’t expect this current situation to harm the overall product in the medium to long term but if you’re looking back – and that is coming back to what Franz-Josef said – we have been in an unnatural environment for, I would say, three years, with spreads tightening and tightening … and tightening to unnatural levels.

Then suddenly came the announcement of the CBPP3. You can see the ECB as a saviour of a situation they’ve created for themselves over three years in tightening spread levels, then stepping in as an investor but I don’t know whether this is the right approach, especially if you don’t understand the political reasoning behind the measure that they have taken.

IFR: Friedrich: syndicate was mentioned earlier as a party to the allocation process. Ultimately, you guys fix the price and advise on allocation. Has your life become much more difficult or much easier as a result of CBPP3?

Friedrich Luithlen, DZ Bank: Both. Pricing a bond, as you all know, is more of an art than a science so it should be on the more interesting end of things. There’s emotion involved and there’s market read involved. But that has become very boring.

Before Christmas, when the CBPP3 was already running, it was very much a game of “where is the secondary”?” What we’re trying to achieve is pricing flat to the curve, so how much in terms of new-issue premium would we like to suggest when we start the process in order not to scare the Eurosystem away from the transaction.

You knew that if it was halfway reasonable pricing, they would be in. In some of the transactions we’ve seen, they were pretty much the only ones in so it was definitely not a functioning market at the time and allocation was easy.

Pricing wise, the process hasn’t changed. If you’re looking at the core markets, you’re trying to price your bonds flat to the curve, give or take a basis point, and then you calibrate a suggestion of a little bit of a pick-up, such that you don’t annoy investors too much on one end by taking it in by five, six, seven basis points and you achieve the best outcome for the issuers as well.

But at the moment books are carried by proper demand. That may be due to the well-known January effect that there is liquidity in the market, and there is a lot of pressure for investors to put money to work. I’m not sure, looking ahead to the next eight to nine months, whether that would be the situation throughout the year and I can well envisage a situation where we are again more reliant on the official bid from the Eurosystem.

Pricing wise, it’s become easy, too easy; allocation wise the Eurosystem is fine with an average amount of bonds and placement wise we’re in a fairly normal place. I’m dreading, however, a return to the world we were in at the end of last year because that wasn’t nice for issuers, it wasn’t nice for investors, and I think the ECB would start thinking: “why do I own 60% or whatever, 50% of a specific trade? Isn’t that a bit much?”

Bodo Winkler, Berlin Hyp: What we saw at the end of last year was really quite horrible because even if you have an investor who is able to buy 70% of your bonds, at these levels, who is buying the remaining 30%? In some of the cases that were issued at that time, you really ask yourself: “Who was in there apart from the ECB”? You saw a lot of order books that just managed to reach the size of the issue.

If we return to the spread-levels of end-2014, I really see the danger of long-term harm to our market. In this low-interest environment, it’s not about losing investors today and maybe they’ll come back later. Some of them could be very disappointed in a market with almost no yield, and might look for alternatives.

Someone said earlier how favourable these low levels are for issuers. I don’t see any benefit for us in the end, because as competition in the lending business remains as intense as before it just takes place on another level. We don’t increase our profit at all by issuing at lower levels.

Matthias Melms, Nord/LB: We’ve been discussing if the ECB is or isn’t a good investor and if the market is healthy or not. What we can really say is that if the ECB is in the order book and if their participation is around 40% or higher, we have a problem with demand from other investors, because the deals are priced too tight for other investors.

In contrast to that, Franz-Josef said the market seems to be in a healthy condition at the moment, and I agree completely with him. The reason for that is that the central banks of the Eurosystem maybe have learned in the last weeks of 2014 that they can’t place orders demanding nearly 50%, 60%, 70% of the whole issue. What we see at the moment is that they’re placing orders 10%, 20%, 30%, 35% and getting an allocation on that level.

Then you get back the other investor groups, real-money investors and banks and the bid-to-cover ratio indicates that if they are in the market – and they want to be in the market because of specific reasons – they have to act a little bit more responsibly than they did at the end of last year.

If they demand something around 30% of the deal, it seems to be a good compromise between the big investor and other investors and leaving some space for some basis points that a real-money investor could earn in the secondary market. That should be the way that they work. If we have to deal with the ECB, the ECB has to be a little bit more responsible and leave some room for other investor groups.

IFR: Which brings me back to you, Ralf. At the end of the day, it is what it is but it won’t last forever. Should your approach be: “we’ll just deal with the situation as it is today, but at some point next year it will go back to level of normality” and just accept you’re getting priced out?

Ralf Burmeister, Deutsche Bank AWM: I don’t dare to make a forecast about central bank policy in a year’s time. I tend to agree with the camp that says the ECB is a special investor in your book because they’re not going to sell and they’re going to sit on it. That’s different to the big investors back in the glory days that Rafael just mentioned.

I still have the words in my mind from an issuer back then. He said: “We were roadshowing in Asia and did the issue but by the time we flew back, one Asian account has already sent the bonds back to Europe”. At that time, we knew that a €500m issue was a €500m issue. If you issue €500m today and x% is placed at the ECB, they will, to the best of our knowledge, sit on it. Then, effectively, it’s, say, a €300m bond so do I want to be in there? That is the technical limitation.

Maybe that’s an explanation as to why investors are partially squeezed in, no matter what the price is, because they know if the ECB is saying: “I’m in for a minimum amount of 25%–30% of this new issue” and they’re reckoning I won’t have a chance to get hold of paper later in a decent amount. I’m not talking about €1m–€3m, but if I need €20m–€30m of this particular bond and I know the ECB is in there, it’s probably too hard or too expensive to try in secondary at a later stage, so you may place a corresponding order up-front in the primary.

That’s maybe one technical explanation as to why you will still see participation at levels where everyone agrees rationally: “This is tight, maybe too tight and there is hardly any scope for performance” but the point is you know effectively the free-float of this bond is much smaller than if you look it up.

To see the digital version of this roundtable, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.