IFR: Alain, if the Euro PP market grew out of investment banks’ placement strategies at an odd time in the market; if market conditions change, does that take away a driver for Euro PP or have you opened the box now?

Alain Gallois, Natixis: We’re entering a phase where we’re moving towards standardisation. With more standardisation, you will attract more investors to come on board and you will start creating a virtuous circle where more investors understand the credits which by extension creates demand for small-cap, mid-cap credit.

We are building a structural market regardless of the level of yields. It’s true that when yields rise investors may be less tempted to go down the curve because they will be back with double A or single A credits with much less risk-raking. At the same time, now that more and more market participants – issuers and investors – are equipped and it’s easier to have access to that market, we are building a real structural market.

IFR: Jason, back to this notion of homogeneity that Ash was talking about earlier, does that process take your price advantage away? If you have a huge pool of investors, the paper is going to go to the lowest bidder. Does that undermine your ability to find value?

Jason Rothenberg, MetLife Private Capital Investors: No, I don’t think so. The way our market works, there’s a clearing spread at which the company can issue as much as it would like to issue. It does create price tension for issuers so it’s beneficial in that sense.

From an investor standpoint, there’s always going to be a spread at which you see a significant number of investors start to drop out as it becomes too painful. So whatever the clearing spread is, most deals reach that level regardless of the number of investors.

Stuart Hitchcock, NYL Investors: Part of the reason the traditional private placement market, the US PP market, has been such a beacon of success over the last two decades is the fact that the US investor universe has been so competitive from a pricing perspective.

The investors we have are institutional investors; insurance companies or pension funds but we’re relative-value investors. We look at opportunities and alternative assets in the US to compare the credits that we see in Europe to determine the appropriate price.

It’s not about yield as such, it’s about relative value and making sure that the price makes sense. I worked on the banking side from the early 2000s and since that time, the US investor bid has become tremendously price competitive. That dynamic has not changed. The relative value we see is against US dollar public bond comparables. It’s extremely liquid but also it’s extremely price competitive.

Just to clear up a comment earlier, which is what happens if it’s more homogenous. We want to see more investors. The more investors there are, the more issuers there will be and good opportunities to put money to work. There’s nothing wrong with competition. We do not mind it; in fact we fully embrace it.

Ash Shah, Barclays: What Alain was mentioning, that some French investors have built credit teams to analyse unrated, i.e. smaller businesses, is absolutely what we would encourage. Some UK investors did that a long while ago and are benefiting from that. But what we see as developing the institutional investor side is that ability to underwrite credit, hold credit, analyse credit.

Not every European investor is there yet because they have focused on Eurobonds and relative value with more of a trading orientation than a buy-and-hold mentality. One of the things that we’ve tried to do with our institutional sales force is pass the message along through them to their counterparts that: “guys, if you want to get involved in the pan European private placement market, you need to be able to underwrite and hold credit”. That’s no mean feat.

You need to buy in talent or be able to put processes involved, get systems in place. That isn’t there yet in some countries or in some areas, so that is an active development area.

IFR: Are you saying that to really engage with this market you need to be a quasi-bank? What you’ve described is exactly what banks do. Do PP investors need to behave like banks?

Ash Shah, Barclays: They need to be able to underwrite like a bank maybe …

Richard Waddington, Commerzbank: If you look at the investors around the table, most of them have developed their credit skills at banks and spend a lot of time analysing the underlying credit. However, they have a different pool of capital to put to work as well as different investment drivers. For the market to develop further, in general, European institutions need to “tool up” with people that are comfortable working on unrated credit.

When a rated bond comes out, orders go in very quickly. That’s not the process in the private placement market we’re talking about. People have to analyse, smell and work through the credit, which is a longer process.

Stuart Hitchcock, NYL Investors: And manage it over time because that’s ultimately what you need. You need to be able to portfolio-manage your investments. That’s very important and that takes resource. It takes commitment to the asset class and resource.

IFR: Are PP investors to some extent hybrid bankers? After all, you’re doing some of your own origination so using some of those skills. You’re using your portfolio management skills to make those decisions. I’d be curious to understand, the three of you, how you see yourselves, as investors, as hybrids?

Stuart Hitchcock, NYL Investors: I wouldn’t call us a hybrid bank in any way, shape or form. We are a long-term institutional investor but we will invest in multiple ways as Jason pointed to earlier. That could be through transactions that are shown to us via agent advisors; alternatively, it will be via direct financings with an issuer if they want to.

The key thing is that the issuer determines how they’d like to finance. For us, that’s in private placements and that’s what we do in Europe. We look at situations and whether we’re willing to invest on a bilateral club or syndicated basis. We have the investor skill-set, we have the ability to originate transactions and portfolio-manage the investments over time. That’s our commitment. We should get rid of the bank analogy. We have investor skill-sets.

Alain Gallois, Natixis: This is absolutely not the mission of the banks. The job of the banks in this new market environment is to assume liquidity and guarantee undrawn facilities, which is not what investors do. Banks guarantee undrawn facilities so when the market is tough for issuers or closed, we will be present with these kinds of facilities.

The second role of the banks is to help corporates finance their projects, to bridge their immediate needs and refinance them. The role of the banks is not to act like asset takers. That’s the role of institutional investors.

IFR: Calum: Stuart mentioned something I wanted to pick up on, which is this notion of going through an agent bank versus direct lending. I’m told there was about US$10bn done in 2014 in direct institutional lending. What are we talking about here?

Calum Macphail, M&G: Direct lending is a bit like private placements; it’s a term that gets bandied around and will mean different things to different people. Therefore, being able to categorise the size of the market is difficult.

IFR:Is there a difference between you going to an issuer directly and negotiating versus doing the same thing through an agent bank?

Calum Macphail, M&G: As Stuart said, it’s merely about the route the issuer is taking to the market rather than the end-product itself.

IFR: Are there benefits either way?

Calum Macphail, M&G: In certain situations, there may be benefits to one side or the other, but obviously the issuer has chosen to go down that route for a reason that suits them. For example that may be one of confidentiality, even in a private market, and not having the deal discussed widely.

As an investor, the lack of other investors creating price tension may give you an opportunity to get a better deal but in a market where price transparency is difficult, that’s quite difficult to judge.

Jason Rothenberg, MetLife Private Capital Investors: The reason we started marketing directly wasn’t about price, it was about trying to get the hold size that makes sense for our institution. Having a large portfolio, if we put in a bid on a competitive agented deal for US$100m we don’t want to get cut back to US$30m. That would not be an efficient way of managing a portfolio of our size.

We are happy to work bilaterally or in a smaller group because we’re able to get a larger piece of that deal. Whether there’s an agent involved in that process or not doesn’t usually matter to us. For us, it’s more about trying to get the right hold size for our institution.

If it was about trying to get a better price, we wouldn’t be able to do any deals that way because companies are pretty savvy and they know where the market price would be, so they’re going to expect that regardless of the number of investors they’re working with.

Calum Macphail, M&G: We don’t directly market but what we do want to do is maximise the channels that we have open to us for companies to come to us so it’s about keeping the bandwidth as wide as possible for your origination platform.

Brian Bates, Morrison & Foerster: There are no companies at the table so I’ll speak for the issuers. The difference between the direct deal and what we call syndicated private placements, we’ve seen a lot of cases where there has been an unfortunate price difference.

But it’s not just price: the other aspect is that 99% of the time the terms you agree are probably worse in a direct deal than you would get in a syndicated deal simply because of the competitive nature of the syndicated deal. Sometimes those terms aren’t important to the company, but if more companies were aware of the differences, I think that they might think differently, or they might ask for a better deal.

Jason Rothenberg, MetLife Private Capital Investors: I would definitely disagree. In the deals we’ve done either bilaterally or in a smaller group, if it’s an existing issuer we’re working with their existing documentation, with maybe a few tweaks to update the document around the edges.

In terms of the core financial covenants or the baskets for liens or subsidiary debt, those numbers are going to be based on that company’s existing documentation or what they already have with their banks and are typically not changed.

Brian Bates, Morrison & Foerster: It tends to be OK if it’s existing private placements. But when a company does its first private placement on a direct basis, you have two problems. One, you’re inevitably going to agree terms that you would not need to agree in a private placement that’s syndicated. I’m thinking most particularly of things like three financial covenants and the Most Favoured Lender (MFL) clause which according to the direct lender “we always get in every deal”.

The other thing that you have to be cognisant of when you do direct deals is down the road when you start doing multiple deals – and many issuers do multiple deals – you’re going to have one direct deal out there that has in effect veto rights over all of your other private placements when they go to make an amendment down the road to reflect the company’s growth.

We’ve had some instances this year where phenomenal companies that started in the market when they were mid-caps and which are now well inside the FTSE 250 or even the FTSE 100 cannot get amendments done to change their financing structures because one or two direct investors very early on have their deal and they want to keep the deal. So they have a veto over all of the other deals. As long as companies are cognisant, that’s fine, but too many times they’re not.

Jason Rothenberg, MetLife Private Capital Investors: Companies always have external counsel though advising them on any deal that they do, so wouldn’t that be the role of counsel to help them?

Brian Bates, Morrison & Foerster: It is if they’re good, but unfortunately they saddle up with people who don’t know the market.

Stuart Hitchcock, NYL Investors: I think the key point of this is that it’s very investor specific. This is a long-term relationship buy-and-hold market. Part of the evolution of the market is the importance of the advice or the relationships that an issuer has or the advice that it takes in terms of determining who the right investors are for the long term for them, whether that’s bilaterally or in a club or in a syndicate. That’s an increasing area of focus.

Calum Macphail, M&G: It’s important on both sides to act responsibly throughout the life of the deal. Both sides have to recognise they’re entering into a long-term relationship and they need to act responsibly during the relationship. Whilst it’s true that for some companies the syndicated process may result in looser terms, for other companies they don’t have the option of going to the syndicated market.

Therefore for them, getting a bilateral relationship with an institution that may be there to support them again and again might be the best option for them. It’s on a case-by-case basis.

Alain Gallois, Natixis: We can’t disagree with Brian because we know it’s happened in the past. But look at the competition between all kinds of market participants that want to buy or to intermediate. Issuers have the pricing power today; they can do whatever they want because there is such an imbalance between supply and demand. Circumstances are on their side.

Calum Macphail, M&G: It’s certainly true that some companies were surprised by the actions of their relationship banks during the 2008-2010 period. They thought they had entered into long-term relationships which meant that the banks would be there to support them in their hour of need and they found that that support wasn’t as forthcoming as they had hoped for. I don’t think you can always lay it at the door of the investor.

Brian Bates, Morrison & Foerster: You’re talking about two different investors though, right: the banks and the insurance companies? If someone were to ask me how I think the two vary, I think you’ve hit on a very good point. Private placement investors are excellent long-term relationship investors and they do stay with you time and time again versus the banking relationship which they assume will be there but aren’t always, as you say.

Jason Rothenberg, MetLife Private Capital Investors: Two quick points. We certainly always encourage companies when we’re working on a direct basis to choose external counsel that know the USPP market because it helps in terms of speed of execution. It also helps in terms of keeping the costs down because typically if you go with a firm that doesn’t know the space, it just results in a lot more billable hours, and so we try to help move that process forward correctly.

With respect to the amendment point, I think it’s important for investors to take a balanced approach. As investors our priority is protecting our investment and our capital but it has to be balanced against protecting the long-term health of the market.

If investors are overly aggressive or act irresponsibly through amendment processes or in terms of how they view the document and potential changes, then it doesn’t do any favours to the long-term health of the private placement market. Treasurers talk to each other all the time, so you want to try to do things correctly and responsibly to encourage the growth of the market and not scare companies off.

Richard Waddington, Commerzbank: One of the things that is attractive about the European market is that an issuer has different product options available to it. Each of the products has different characteristics. Potential issuers can look at each product and ask: “Which one is most attractive for me?”

The US PP is very competitive and offers attractive pricing, but the documentation is usually pretty tight, there’s not a lot of wriggle room. We’ve seen a lot of issuers that are stuck with very expensive deals.

Some of the other products have more flexibility and give issuers more optionality. I think it’s important for the issuer to have a look at all the private placement options available in the European Market and decide what product suits them best at the point of issue.

IFR: Nick, on the point about standard documentation templates the working group put out, what, in your estimation, will they have down the track?

Nicholas Pfaff, ICMA: They will have a positive impact. What we’ve done is ensure that there is some commonality on the key terms between the LMA docs and the Euro PP docs. We’ve also cleared the foundation for other markets – and I’m thinking particularly Italy which is now looking with great interest at this market – to develop documentation which is derived from that.

Dialling back 12 months, there was a risk that we would have ended up with LMA docs and Euro PP docs, which were pretty far apart. We’ve avoided fragmentation. If you look at what we have now, very broadly speaking, if you are coming from the banking world, if you want to issue under UK law, if you are implied investment-grade, you might look more favourably at the LMA docs.

If you are a French or Continental European issuer, and you are perhaps cross-over or sub-investment grade; you may want to work with the Euro PP documentation. The Euro PP documentation also has a bond format that is very close to the Eurobond docs which may appeal to market practitioners familiar with that standard.

Looking at that matrix, we’ve covered a fairly broad space. It would have been great if we could have come up with one set of documentation such as exists in the Eurobond market, but that’s going to take some time. Clearly one of the challenges now – and we’ve started discussing that – is: are there ways of bringing our set of documentation closer to the other major market, the Schuldschein market? There have been some approaches in that respect now, so let’s see how that develops.

Again, without reaching complete harmonisation with one set of documents, we’ve now got a set of documentation which covers most situations in the market

Emilie Wong, ING: Standard docs do help. It also helps investor education. We’re not just talking here about big investors; this also involves smaller investors who have been asked by their local authorities to get involved in the SME private placement market.

On a deal we were working on recently, on NDA, we used the ICMA template and it was much easier. It was a bit erratic before; everybody was using their own internal templates so standardisation definitely helps.

Issuers sometimes say to us: “We want to have documentation in French”. But as this market has now developed we don’t necessarily only target French investors. You see Dutch, Belgian and Italian investors coming to this market and therefore it makes sense to have English language to be used as a template. The more we can have standardised documentation. it will definitely help to harmonise and educate the people involved in this market.

Nicholas Pfaff, ICMA: The Pan-European Private Placement guide is not just about documentation; it’s a broader effort to try to advertise and agree on a standard for the pan European market, and promote best practice.

That’s important because there’s a risk of reducing this to a documentation discussion. We’ve said there’s going to be a variety of documentation; it’s going to take time for standardisation. What is more important is to agree on the product, what are the best standards, what are the roles of the banks, what can the issuers expect, etc. That’s what we tried to do here.

This is going to evolve. It’s version 1.0.

Richard Waddington, Commerzbank: The word standardisation needs to be explained. I would say it’s more of a starting point/framework because each of the documents are heavily and individually negotiated. Obviously the US PP is much more advanced in terms of that framework, but the Euro PP and the Schuldschein both have frameworks in place but are much looser.

Ash Shah, Barclays: Richard, on the Schuldschein side are you seeing a huge amount of volume changes or differences from issuers’ expectations? Are they saying: “I’ll do a Euro PP or a Schuldschein?” because we’re not seeing that in the US PP.

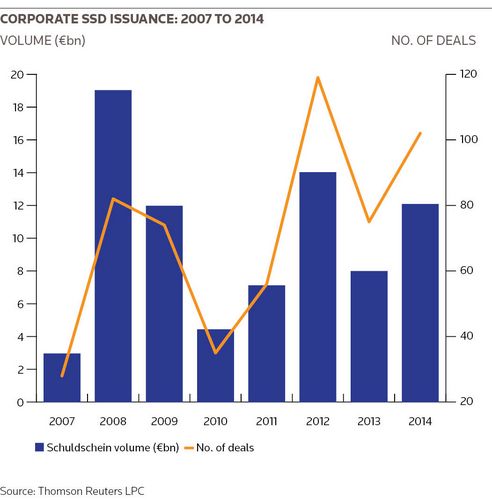

Richard Waddington, Commerzbank: In France right now, a lot of people are marketing both Euro PP and Schuldschein, and over the last 18 months we’ve seen a lot of Schuldschein issuance coming out of France. The question is why is that? In my view, we have seen a bifurcation of the French market, with the Euro PP moving more into the BB space; whereas the Schuldschein has been more active in the investment grade and cross-over space.

Alain Gallois, Natixis: And the Schuldschein market offers longer maturities, right?

Richard Waddington, Commerzbank: Yes and it offers bigger potential volume, so it depends which market you’re in as to what people are offering out there.

Alain Gallois, Natixis: The question about the standardisation of documentation is absolutely key because what the Euro PP suffered from in 2014 is transactions took too much time for issuers and too much time for investors to analyse. On average, it takes four to six months for an issuer to do a €50m trade.

So it’s absolutely crucial if we want to develop and grow the market to have a minimum of standardisation to structure each trade within three months to make it simple for investors to analyse and simple for issuers to produce when we’re talking about mid-sized corporates that don’t have the resources to dedicate.

Calum Macphail, M&G: I’m pretty sure that when Ash goes to pitch a private placement product of whatever hue to a company, the first question is not: “How are we going to document this?” They’ve got concerns that go above and beyond that, but what it does do and what people are saying around the table is it gives them confidence in the execution of that transaction, however you want to ultimately do it.

And it gives them an expectation in terms of what they will end up with, both from a time perspective and the restrictions that they might have to be imposed upon them.

IFR: Nick, did I detect a note of frustration or am I imputing one from the fact the LMA and the Euro PP steering committee came out with their templates literally a week or two before the Pan-European PP Working Group came out with its market guide? Why did you think the Euro PP and LMA guys did their thing; incidentally the former under French Law; the latter under English law?

Nicholas Pfaff, ICMA: We need to come back to the formation of the working group. This is not an ICMA effort but ICMA had enough legitimacy to help co-ordinate a cross-industry effort which did indeed include the LMA, the Euro PP Working Group, AFME, the Investment Association, CBI, etc. We had this incredible list.

I think it was a remarkable success in terms of how civilised and how relatively easy our discussions were and how quick our progress has been. We wrapped this up within about seven months, working on the basis of the French charter. Coming back to your specific question about why the LMA and the Euro PP documentation came out before the European guide, we had a discussion about bringing everything out together, but at that time the documentation was going to be ready a good three months before the guide.

So we just took a practical decision and said: “There’s no reason to hold back the documentation. Let’s make it available to the market”. We knew we were going to lose out a little in terms of the perception of it being a co-ordinated effort, but we decided we would get it out if that’s what the market needed . It was a trade-off.

To see the digital version of this roundtable, please click here .

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com

| US Private Placements – Global Issuers FY 2014 | ||||

|---|---|---|---|---|

| Lender | Value (€m) | No. Of Deals | Market Share (%) | |

| 1 | BofA Merrill Lynch | 10,860.00 | 61 | 21.1 |

| 2 | JP Morgan | 5,955 | 41 | 11.6 |

| 3 | RBS | 3,803 | 24 | 7.4 |

| 4 | Barclays | 3,499 | 26 | 6.8 |

| 5 | Citigroup | 3,474 | 22 | 6.8 |

| 6 | Morgan Stanley | 2,392 | 21 | 4.7 |

| 7 | Mitsubishi UFJ Fin’l | 2,138 | 18 | 4.2 |

| 8 | US Bancorp | 2,067 | 22 | 4 |

| 9 | HSBC | 2,026 | 14 | 3.9 |

| 10 | RBC Capital Markets | 1,781 | 8 | 3.5 |

| 11 | Wells Fargo & Co | 1,682 | 18 | 3.3 |

| 12 | NAB | 1,668 | 14 | 3.2 |

| 13 | Societe Generale | 1,529 | 7 | 3 |

| 14 | CBA | 1,436 | 9 | 2.8 |

| 15 | Goldman Sachs & Co | 1,317 | 5 | 2.6 |

| 16 | Lloyd Securities | 1,033 | 10 | 2 |

| 17 | Deutsche Bank | 854 | 9 | 1.7 |

| 18 | KeyBanc CM | 833 | 11 | 1.6 |

| 19 | BNP Paribas | 454 | 5 | 0.9 |

| 20 | Scotiabank | 431 | 5 | 0.8 |

| 21 | Credit Agricole CIB | 314 | 3 | 0.6 |

| 22 | Santander | 276 | 2 | 0.5 |

| 23 | ING | 274 | 2 | 0.5 |

| 24 | CIBC World Markets | 260 | 3 | 0.5 |

| 25 | TD Securities | 213 | 4 | 0.4 |

| Total | 51,411 | 230 | ||

| Source: Thomson Reuters |

| US Private Placements – Top 15 issues. FY2014 | ||

|---|---|---|

| Issuer | Country of Issuer | Deal Size (€m) |

| Sodexo | France | 1,100.00 |

| Enbridge Pipe Southern Lights | US | 1,061.00 |

| Cobham | United Kingdom | 930 |

| Cabot Oil & Gas | US | 925 |

| Smith & Nephew | United Kingdom | 800 |

| Tri-State Generation | US | 750 |

| AMETEK | US | 700 |

| Arthur J Gallagher & Co | US | 700 |

| Hunt Oil Co | US | 555 |

| North West Electricity | United Kingdom | 511.94 |

| Arqiva Financing No 1 | United Kingdom | 509.58 |

| AEP Transmission | US | 500 |

| Cerner | US | 500 |

| Hearst Communications | US | 500 |

| AptarGroup | US | 475 |

| Source: Thomson Reuters LPC |

| US Private Placements – Top 10 European issues FY2014 | ||

|---|---|---|

| Issuer | Country of Issuer | Deal Size (€m) |

| Sodexo | France | 1,100.00 |

| Cobham | United Kingdom | 930 |

| Smith & Nephew | United Kingdom | 800 |

| North West Electricity | United Kingdom | 511.94 |

| Arqiva Financing No 1 | United Kingdom | 509.58 |

| Capita | United Kingdom | 445.07 |

| Associated British Ports | United Kingdom | 431.77 |

| Shurgard Europe SPRL | Belgium | 403.93 |

| Compass Group | United Kingdom | 400 |

| Fritz Draxlmaier & Co | Germany | 380.74 |

| Total top 10 deals | 5,913.04 | |

| Total USPP issuance by US issuers | 24,819.14 | |

| Source: Thomson Reuters LPC |

| US Private Placements – European issuers only FY 2014 | ||||

|---|---|---|---|---|

| Lender | Value (€m) | No. Of Deals | Market Share (%) | |

| 1 | RBS | 3,183.20 | 21 | 24.6 |

| 2 | Barclays | 1,851.60 | 14 | 14.3 |

| 3 | BofA Merrill Lynch | 1,385.00 | 6 | 10.7 |

| 4 | Lloyd Securities | 982.6 | 9 | 7.6 |

| 5 | HSBC | 908.1 | 9 | 7 |

| 6 | Societe Generale | 736.1 | 3 | 5.7 |

| 7 | JP Morgan | 621.8 | 5 | 4.8 |

| 8 | Citigroup | 592.4 | 2 | 4.6 |

| 9 | Deutsche Bank | 437.3 | 3 | 3.4 |

| 10 | CBA | 431.8 | 1 | 3.3 |

| 11 | Credit Agricole CIB | 313.5 | 3 | 2.4 |

| 12 | BNP Paribas | 310.9 | 3 | 2.4 |

| 13 | Santander | 276.3 | 2 | 2.1 |

| 14 | ING | 273.7 | 2 | 2.1 |

| 15 | NAB | 169.1 | 2 | 1.3 |

| 16 | Wells Fargo & Co | 134.6 | 1 | 1 |

| 17 | Morgan Stanley | 128 | 1 | 1 |

| 18 | RBC CM | 90.4 | 1 | 0.7 |

| 18 | Mitsubishi UFJ Fin’l | 90.4 | 1 | 0.7 |

| Total | 12,916.90 | 54 | ||

| Source: Thomson Reuters LPC |