To view the digital version of this report please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

IFR: It sounds like the Schuldschein market is a bit of a beneficiary of the end of the retail market in syndicated loans, now that borrowers are arranging deals themselves? Do you feel like the Schuldschein market has picked up business as a result of that?

Michael Schramm, BNP Paribas: I’m not too sure, when I’ve seen the last retail bond – and I would regard a retail bond with a €1000 denomination, for example. I haven’t seen being issued that in a very, very long time for regulatory reasons, mainly. So, yes, that could have been the reason why Schuldschein has been performing. I would also say that the issuers still want to diversify a little bit away from the relationship banks, maybe, and want to open up to new refinancing sources, and Schuldschein was able to give that in smaller ticket sizes. There are various reasons, we’ve seen that the spreads and the demand has been very resilient to the last two crises. Schuldschein was always there and 2008 was an exceptional year when even the DAX companies made use of that market. We are now normalising and using the Schuldschein as a market entry point for mid cap companies, for unrated companies, for family companies, which are not really transparent. But we still see the diversification of the market and the internationalisation of the market on the issuer and the investor side.

I was trying to pick up on the last comment, we do have something like a European private placement market. We’ve got it already, it’s sometimes good that it’s been so private, and all of a sudden it becomes more noticed, and nobody really knows what it is. That’s also the beauty of it, to some extent: that it is so private. There will not be one private placement market for some time, I think. We see investors opening up and enjoying the idea of buying into non-rated paper in a bond format, for example.

It takes a little bit of time and convincing, and maybe the lack of opportunities, yields dropping, supply is not there, and all of a sudden we see UK investors looking at non-rated corporates for the first time ever. Yes, that might require some financial covenants and the issuer might not be willing to give that up, but all of a sudden you are having the discussion about, “Would you invest into a non-rated company and what are your parameters?” That is definitely going on, and therefore I still think that we will get some depth in the European private placement market. All the other documentations that we already have will go on with all their specific features.

Ingo Nolden, HSBC: Just to clarify from my side, when you say, was Schuldschein benefiting from limited growth in retail loan market, are you referring to the Mittelstand market?

IFR: Well, from what I see, there’s a lot less broadly-syndicated loans out there. Regarding the comments that Rachel just made about getting access to paper as a retail investor – developments around the top end of corporate lending as borrowers focus on big-ticket lending are probably having a beneficial effect by pushing retail loan investors into the Schuldschein market.

Richard Waddington, Commerzbank: Yes, it definitely has in my view, you guys will have seen the same. Internationalisation has been very much driven by the reforming of the loan market. In the boom times in 2006-7, there was so much paper moving around the loan market, it wasn’t an issue for investors to access it, and there was always people looking to sell on down. Obviously the market has restructured, banks have deleveraged, there’s a lower financing requirement and more of it’s moved into the bond market. The loans out there are much more core relationship loans with aggressive pricing. The cross-sell is a quid pro quo; ancilliary business is kept to the core group of banks. As a result, some of the banks looking to buy smaller ticket sizes in the market, €5-25 million have found it hard to get supply. Certainly Schuldschein has partly helped to fill the gap for some of those organisations. I think that’s the case for your bank Rachel? Everyone was struggling for product at the end of the day, certainly if you’re a core relationship bank you get a piece of the action, but it’s usually an undrawn revolving credit facility. But if you want drawn loan debt, it’s quite tough to find in the secondary market in chunks of €5m-€10m. Schuldschein fits that demand nicely.

Ingo Nolden, HSBC: It’s a challenge to keep the Schuldschein market as professional as it is, that was the reason why I wanted to clarify your reference to retail demand. When we are looking at the Mittelstand bond market, which is currently under pressure due to defaults, Schuldschein arrangers should be conscious of quality and professionalism. It’s important to analyse the cycle; it’s sunny days now, but we know that there will be tough times ahead. The Mittelstand market is characterised by the professionalism of people in that market, every bank that brings a deal to a market has a reputation to lose, that’s a very important lesson from the financial crisis. All our clients are long-time clients of our institutions and each of us is very conscious of bringing deals with the right quality, we don’t want to see investors finding that what they have bought is collapsing. That means developing professionalism further in the market, it’s in the interests of everyone to keep the highest possible standards. It’s good that we have the LMA standards, although there are limits to standardisation. It’s important that we ask ourselves, “Is this something that is now feasible?” One reason why the market did so well in tough times was because there is an unspoken common agreement about quality.

Klaus Aldinger, LBBW: The difference is that the Schuldschein market addresses professional investors like banks, and they all do their own assessment. Therefore, you have to provide good credit quality, and every syndicate and every arranger who wants to try to bring something which is not appropriate quality may fail with the whole deal. Investors recognise if there is trouble ahead with a company, if the business model is not working, if the figures are not right, therefore it’s a very good quality market. Not so many issues have defaulted in recent years; Rachel, of your investments, did anything like this happen in recent years?

The funding costs for Asian banks at the moment are slowly but steadily rising, which makes it hard for us to look at some of the Schuldschein deals; anything that’s short of 150bp makes it really difficult

- Rachel Rueiying Yang

Rachel Rueiying Yang, Chang Hwa Commercial Bank: Not from one of our Schuldschein investments. Otherwise no more.

Raoul Heßling, Commerzbank: I completely agree with Klaus. I don’t know whether there are any statistics on defaulting corporate syndicated loans - in Schuldschein, the default rates must be really low compared to other products because they are all good quality names, that we bring. It would be interesting to run that statistic. But you can count them probably on two hands.

Michael Schramm, BNP Paribas: Well, we don’t even have Schuldschein league tables, so maybe you should start with that before we start a league table of default.

IFR: It sounds like the market has an interesting dilemma ahead, because you’re going to be bringing smaller companies with fewer ratings, so how are you going to ensure credit quality? What are the criteria that companies have to fit to go through that? What hoops do they have to jump through to make sure that you as arrangers are meeting that credit quality requirement?

Raoul Heßling, Commerzbank: Michael already commented on rated versus unrated, that’s not an issue. The Schuldschein market is an unrated market, when we go down the credit curve, we are testing the limits of investment grade. We’re talking about BBB rated companies with half a step into BB+ but this is the limit that we’re testing. Most of us are very reluctant to go further down the curve because we know that investors prefer strong credits and you have to judge whether Schuldschein documentation is the right documentation for a sub-investment grade name because it probably doesn’t give you the right protection that you’re looking for.

So, again, if we’re going down the credit curve, we’re very cautious about it. Normally Schuldschein investors have a lot of requirements, especially regarding quality and normally Schuldschein investors are not allowed to invest in sub-investment grade issuers. That’s one possible reason for the stability of this market.

Karl-Heinz Bühner, LBBW: Other specific investors are high yield investors, but the requirements of the high yield investor’ requirements are different from Schuldschein documentation and so you can’t say, “Okay, you get down the credit curve” and issue sub-investment grade. You can try it, you might succeed, but if you go deeper down the credit curve, you might not be successful.

IFR: You were talking about some potential high-yield issues or issuers before. Would that be something that the market could handle?

Michael Schramm, BNP Paribas: There are specific issuers that can get away with a high-yield rating, especially from Germany. There is some feel-good factor about them, because everyone realises that they are an established name in the capital markets and they just happened to choose the Schuldschein at some stage. That does not mean that any high-yield credit quality is placeable. I completely agree with what you just said. In some cases, I think it could be a question of price, and investors might be willing to pay or to accept a certain spread for a certain credit quality, but then in the end it might not be appealing to the issuer any more. So it’s a dead-end street. Often, then, the question really is, “Is it the right product?” Or would you rather not offer this issuer another syndicated loan? Because it tends to be cheaper and borrowers can continue to grow, and maybe improve credit quality to the extent that it’s eligible for the Schuldschein.

Richard Waddington, Commerzbank: From an issuer’s perspective as well, if you’re at a certain credit level, does it make sense to issue a syndicated loan or Schuldschein? Because Schuldschein documentation is loose but if you’re a very cyclical company, then even loose covenants can be a challenge after some years. We have to remember in Schuldschein that each investor takes their own decision and when you’re a cyclical company and you do a five year financing, do you go for systems which you have in syndicated loans, or the bond where you usually have no maintenance or financial covenants?

IFR: At this point, I was thinking about asking about the mix of the market between corporate and financials, and perhaps public entities. However, I’m going to hand over to Alex, who’s been tracking the market, so he can look in a little bit more detail around the corporate part.

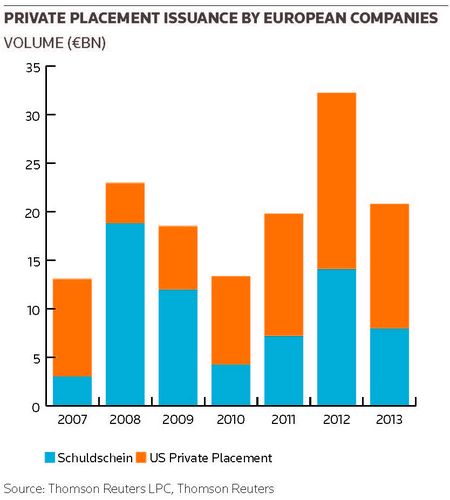

Alex Lembcke, Thomson Reuters: I’ve brought some statistics to show what the data is telling us. We don’t get all the deals, some private deals that will never be disclosed but our data is representative of the market. The first chart shows corporate volume. Last year, we saw about €8bn of issuance, which is down slightly from the previous year. It’s a bit difficult to say what the normal level for Schuldschein is because in 2008 we had a big spike from the large corporates which were having difficulty funding elsewhere that came to the Schuldschein market. But it seems like last year was more like a normal level.

If you look at the average deal size, you see as you were discussing, size has dropped to what it was prior to the crisis. We’ve also seen that Mittelstand is now accounting for a similar portion of the market as it did pre-crisis because during the crisis, a lot of large corporates and international issuers came in as well. Mittelstand accounted for about 40% of issuance last year. But not everything is returning to pre-crisis levels. We have seen – as you guys were discussing – the French coming into the market quite a bit, they now account for about 14% of issuance. We also have a slide showing the breakdown by issuer country. This is interesting and shows that last year there were a lot fewer countries than in 2012, when we had more international issuers. We still did see deals from the UK, Finland, Sweden, but last year I believe we had five additional countries issuing Schuldschein than we had this past year. The next one slide is looking at international issuance, DACH being Deutschland, Austria, and Switzerland, and so these are issuers from outside of that region - France and Nordics. We’ve seen that decrease over the past year compared to 2012, getting more towards pre-crisis levels, where you mostly get Mittelstand. Then we have the league table; a lot of these statistics were available in our 2013 review of the market.

IFR: So in terms of the issuer mix, or anything else, does anything particularly stand out from that data, or look interesting? Does it tally with the experience that the market is perhaps a little less international than it was?

Richard Waddington, Commerzbank: Two trends obviously stand out, the first is the move back in towards the mid-sized companies issuing. They’re the heartland of the Schuldschein. The trend towards ‘small is beautiful’ will continue in Schuldschein, but I also think the second trend of internationalisation is going to continue. Once you step out of Germany, the options for the borrower increase in terms of the product offering. If you chat to the people around the room and you say, “What is your pitch-to-win ratio in Germany versus internationally”, with Schuldschein, you find that the number increases internationally; you’ve got to do a lot more pitching to get a mandate. That’s because there’s more product offerings out there. But that doesn’t mean that the internationalisation’s not going to continue in that regard.

Klaus Aldinger, LBBW: In previous years, you had some French companies or English companies with a rating that went to the Schuldschein market just because it was cheaper. Now with the bond markets already very expensive, these issuers have the opportunity to issue bonds, and bonds in home markets - these bonds are for them cheaper than the Schuldschein. This is the main reason for the international share having dropped a bit. As Richard said, apart from that the international trend is still intact and going on.

Raoul Heßling, Commerzbank: The growing market share of Mittelstand, which as been spiking over the last year, shows that the growth that we saw two years ago, was much more sustainable than what we saw in 2008-09; at that time the issuers didn’t go to this market because it was the product of choice but because they didn’t have any reasonable alternative. Whereas all the issuers that we have seen in the last two years, be it German but as well on the international side, they really like the product. They wanted to get investor diversification, they like to do different maturities in one go, and that’s why they went for it, although we have competition with other products. Maybe companies from fewer nations have been active last year than the year before, however this is only official statistics. Some other countries were active as well. I see that as a positive, we have issuers from various countries in the last years that came to the market full stop. Whether they came two years ago or one year ago, it shows that Schuldschein offers a viable option to issuers from these regions, and that you can find the documentation solutions, because – just between the people here, it’s very tricky to bring a new nationality to the market. You have to be very careful when documenting, looking at regulations on a national basis. This shows there have been solutions in France, in the UK, in Belgium, Netherlands, Switzerland, Finland, Sweden, to accommodate this.

IFR: Are you surprised that there haven’t been more issuers from peripheral countries? That was one argument - that perhaps the shuldschein market might scoop up some of those issuers that couldn’t necessarily tap the syndicated market quite as easily. Has anybody got a view on that?

Richard Waddington, Commerzbank: Ultimately it is driven down by investor demand for the peripherals. So as a result, I don’t think the demand’s been there in a lot of cases to issue. We are now seeing the investors look more towards the peripherals in terms of appetite, as they’re getting a bit more comfortable. Rachel, from your perspective, are you going to get a sign-off from head office to do a Spanish or Italian Schuldschein in the current environment?

Rachel Rueiying Yang, Chang Hwa Commercial Bank: I don’t know, the funding costs for Asian banks at the moment are slowly but steadily rising, which makes it hard for us to look at some of the Schuldschein deals; anything that’s short of 150bp makes it really difficult. Which is part of the reason why we started contemplating doing longer maturities, previously, five-year, five-and-a-half years was the absolute max. But we had to, we had no other option but to convince our head office that, “Look, here is a really good name that’s totally worth looking at from a longer-term perspective” we convinced them, so that’s our very first. I believe that we’re probably one of the first few among our Taiwanese peers to do that. That’s going to be tough, going forward, to push. However, having said that, because of the minimum yield requirement, our head office have now started to say, “How about looking selectively on the peripherals, say, Spanish names?” I’m not sure if they would be open to a Spanish Schuldschein but I wouldn’t rule it out. Because they always say, “It’s on a case-by-case basis”. So as long as its good quality and we do our due diligence then there may be a chance. Perhaps it would be better, then, in that regard, to stick to a shorter maturity, say, three-year or four, if not quite five. It would help if there is a US dollar option in this regard, because sometimes it is better for us to balance our US dollar and euro exposure.

Klaus Aldinger, LBBW: What Richard just mentioned was certainly one of the trends in 2013: that many issuers tended to offer two tranches, dual-currency tranches, and mostly it was US dollars and euros. As far as I know, those US dollar tranches have been very well received by investors.

Rachel Rueiying Yang, Chang Hwa Commercial Bank: I was under the impression that there was one Schuldschein that was arranged in Asia and was pitched to Asian investors directly, not to the London banks’ offices. So If we want more internationalisation for this product, say, in case hard time hits and issuers ever need to diversify their funding base again, then it would always help if investors already know this better. Not just for the people sitting here, but across the board, including Asia. I don’t know if it’s worth pushing that, but then given it’s an issuer’s market, I don’t know how much commercial or economic sense it makes there.

IFR: To come back to the broader syndicated loan market, one of the things that I’ve been noticing in London is that, there’s a lot of interest around SME and mid cap lending as a decent source of revenue. A recent report from Deutsche bank recently highlighted the difficulties in making money in large corporate lending. I’m wondering if, again, this plays to some of the Schuldschein market strengths as well, because it’s definitely an area that banks are focusing on. What do you think, Kirstin?

Kirsten Schulz-Lobeck, Erste Group: Well, I read the article. It goes hand-in-hand with this tendency of insurance companies to team up with banks, focusing on the SME sector. I don’t know. I have to admit, the mid cap that I see has stories behind it. On the SME side, personally I’m not sure. I cannot see how you can really market some of these names to a broader base outside either a certain region in a country or that specific country. I see it, but I’m not convinced yet.

Ingo Nolden, HSBC: I agree. At the end, we’re talking about capital market products and each of us is doing a filtering, “Is this issuer a really capital market-oriented minded issuer?” and with SME, you just have the problems of financing cost plus high transaction costs, which produce relatively high all-in costs. If an issuer intends to raise €5m or €10m Schuldschein and is willing to pay all fixed costs for it, I would be worried. We have seen all these mezzanine programmes in the run-up to the financial crisis, which to be honest didn’t work because the typical principal agent conflict couldn’t be dissolved. Mingling everything and then putting it into a box and saying ‘this is an SME portfolio’ might not be, at least for what I foresee for the Schuldschein market, the right way to do it. Some banks have a clear justification to operate in the sector, local banks know SMEs quite well. They have people on the ground; they have information and experts that capital market investors do not have.

Raoul Heßling, Commerzbank: It’s helpful to have a definition of what an SME is first. What kind of sizes are we talking about? Just looking at Alex’s presentation, you’re looking at Mittelstand as corporates with less than €1.5bn turnover. So that’s medium-sized larger corporates. In that area, we see increasing competition. We saw that last year, especially among the big domestic banks from each country, trying to grasp some space in other countries, setting up branches and trying to get their foot in there. There is lots of competition. Not so many companies need funds, so we are harvesting other territories. I will have to see how it works out in the long run.

Klaus Aldinger, LBBW: From an investor’s perspective, there are a lot of investors that say, “You need at least a minimum turnover of €500m per year, otherwise the company is too small and we’re not going to look at them”. Because many of them have got their own credit business, their own loan business, for example, and say, “If you want to do something opportunistic then it needs to have a certain size and a certain volume, and everything else is too small for us”. Direct investments into very small Schuldscheins are rather not favoured at the moment, and putting all those small Schuldscheins together, I don’t know if that makes it better.

IFR: I was thinking, also, that the Schuldschein might have been a beneficiary of bank deleveraging but now that banks are growing portfolios again, that’s probably increased competition for this market. Also, banks were courting the institutional market a couple of years ago and now they’re stepping back into that space. Do institutional investors have a stronger foothold in Schuldschein or will they be displaced by banks that are gung-ho about lending again and trying to take some of that business back?

Richard Waddington, Commerzbank: Banks are going to lend aggressively wherever you look, be it internationally or in Germany. Banks are full-steam-ahead, and they want to get what they can because their loan books are running down. So there is more competition from banks. The institutional side is liquid as well, and you’re seeing institutional investors pushing out tenors and unrated credits.

So you’ve got skirmishing going on out there. Whichever market it is, there’s a scarcity of supply. So I don’t think anyone’s safe or immune from that, but depending on where you are in that investor community you’ve got to play to your strengths. Banks are comfortable at five years and stretch to seven years; the institutional guys are having to go into unrated territory, and go out, tenor-wise.

IFR: I also wanted to ask, just before we perhaps draw the conversation to a close: are there any other significant developments? We talked about corporate quite a lot, but have there been any developments around financials or government issuance that we should be touching on, perhaps?

Ingo Nolden, HSBC: You saw also a trend of internationalisation in public sector issuers. There were a number of highly successful sovereign trades as well as supra-nationals. The search for pick-up from the investors’ side is not only a corporate market phenomenon; it’s in all types of markets, but less so in the financial space, for obvious reasons, but in the public sector space.

Rudolf Bayer, UniCredit: That’s our observation as well, investors very much favour the Schuldschein. For financial issuers and sovereign and supranational issuers, this is especially true, even more so for longer tenors.

IFR: Do you expect to have roughly the same mix because I understand the issuance is weighted towards financials? Government and corporates is very much smaller; do you expect the same range of business for this year?

Raoul Heßling, Commerzbank: The markets are very different to each other. It’s such a huge difference if you talk about Schuldschein for banks and for corporates that you can’t really compare it.

Klaus Aldinger, LBBW: It’s like comparing loans to individuals to Schuldschein. One is really big and very fast and you have one-page documentation, then you have communities or cities being financed by Schuldschein. Each of these products is very different. The corporate Schuldschein are syndicated and therefore are not disclosed to the public, and the financial Schuldschein is just over the counter. I’d say that the financial Schuldschein business is way bigger than the corporate Schuldschein business. You also have a lot of structures on the financial Schuldschein, like multi-callables. They’re normally in the NSV format, because they have longer maturities and this is attractive to investors because they like to have duration and they like to have the high coupons that come with structures and for many of the institutional. 4% is still the magic number.

This is a daily business, and the product offers issuers swift execution. Corporate issues usually take longer, as borrowers are less familiar with the procedure

- Rudolf Bayer

Michael Schramm, BNP Paribas: The main difference is that with financials you have established market issuers, and they use the German formats like a template, like a programme. It’s widely accepted so whenever a market window opens up and you have the right coupon or yield or the right structure, it is printed with one-page documentation. So it’s not really the issue of documentation per se, but it’s rather the structure and the yield. It’s very frequent - it’s one investor, one issuer, and you just print the deal.

With sovereigns, you have established issuers but it’s more syndicated. But you still have safe haven issuers with a feel-good factor. On the corporate side, however, you very often have the one-time issuer, the first visitor to the market and you have to get credit loans approved. You have to filter, if you have the right name for the specific investor base. So it’s a lot more labour intensive, and a lot more waiting, “Is it the right decision to go ahead with this project or not?” That’s why I would think that the financial market is very un-transparent and probably much, much bigger than we all think. But because you never really find out how big it is.

Rudolph Bayer, UniCredit: This is a daily business, and the product offers issuers swift execution. Corporate issues usually take longer, as borrowers are less familiar with the procedure.

Klaus Aldinger, LBBW: Yes, most financials post levels on a daily or weekly basis and then you can ring them up and ask for a mandate, and execute it within a day with one single investor, like Michael said.

IFR: Who’s doing financials, out of curiosity?

Ingo Nolden, HSBC: The monthly Bundesbank report gives you a feeling of what is going around in this sector; but the financial and public sector is a big unknown to most of us, I would assume.

IFR: Are there any questions that I might not have thought of, that you’d like to ask?

Klaus Aldinger, LBBW: I would like to know what our friendly competitors are expecting for the market volume this year, and in terms of pipeline, where will the bulk of the transactions happen? Will it be the second quarter or the third quarter or, is everybody a bit pessimistic about volumes?

Raoul Heßling, Commerzbank: We have seen a very dull start to the year in the first quarter, with very few issuers tapping the market. We expect some more activity in the second quarter when full-year financials become available, but we can’t see yet how we’ll reach last year’s volume, because there is just not enough issuers out there that need funds. We are all able to get nice order books, nice subscriptions but we’re looking for the issuers, at the end of the day.

Rudolf Bayer, UniCredit: In the last year, we saw already quite a lot of pre-financing and refinancing from corporates.

Raoul Heßling, Commerzbank: But the majority is going to come in the third quarter, because the second quarter can’t make it up yet, so it must be the third and fourth quarters.

IFR: Any other questions or comments? I think we might bring things to a close. So I’d just like to thank you all very much for attending and for a very interesting and very full discussion. I hope it was as useful to you as it was for me. Thank you.

To continue reading this roundtable, click the relevant section. Introduction - Participants - Part 1 - Part 2 - Part 3 - Feature