To view the digital version of this report please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

IFR: In a global marketplace is that valuation benefit as strong as it has been in the past?

DeClark, Credit Suisse: Given the strength of the technology IPO market in the US, I would say that it’s as strong as ever. QIWI, which has all of their operations in Russia right now, is being valued similarly to a US-based company.

IFR: A lot of foreign listings are also companies incorporated in tax havens.

Baird, Citigroup: You do have some tax havens out there that US public equity investors are used to investing in. They understand all the charter provisions and corporate laws. But I think really at the root, the US is where the money is. It’s just there’s a depth of investor, there’s a depth of sophistication. And that depth of investing expertise means that valuations are higher.

Water always finds its own level. At the moment, multiples are highest here – and so it is perceived as the world’s stage, particularly for the tech industry. The tech leaders globally are all out in California, and people want to run alongside that. I think, at the end of the day, it’s what motivates a lot of those sorts of issuers to come to this market.

Morrison, Blackstone: I would just summarise it by saying when we’re looking at where we want to list a company that’s going public, we look at what sort of a company it is, where the comparable companies are listed, and where the biggest, most informed shareholders are from a liquidity standpoint.

We also look at where the multiples are for relative sectors around the world, and you love to list in the highest-multiple marketplace. Also you think about where the business is domiciled, where their business is transacted and where their growth opportunities are. An IPO is certainly a branding event, and you want to maximise the amount of attention on a company’s business. From a business standpoint, you can benefit from the listing venue.

Schacter, Goldman Sachs: Even in the equity-linked markets, I would say that there’s a lot of recognition that the US market is just more buoyant and more willing to pay a premium valuation. We saw that with ArcelorMittal. So not even in a growth industry, but also with a global steel producer that was able to recognise the US is the most liquid market.

When we led the ArcelorMittal US$4bn dual-tranche offering of mandatory convertibles and equity, we specifically started the process in the US morning to allow for US investors to opine first, and express a view on valuation that we knew would be more constructive than the valuation that would be expressed outside of the US. That really created a lot of momentum.

IFR: So let’s switch back to the private equity side of the business. It seems that we have tested limits in terms of leverage multiples on recent IPOs such as Intelsat and HD Supply, where there was seven/eight times leverage. Is that the high-water mark?

Morrison, Blackstone: You have to look at each business and each sector – and how dependable those cash flows are – to see what sort of leverage a business can handle. We’re constantly talking with investors to get a sense of how they’re thinking about leverage. We try to bring an appropriate capital structure to the marketplace.

I think we try to approach this conservatively. Obviously we’re in an improving economic environment now, but one never knows what’s going to happen in the future, so you want to make sure the balance sheet is set up appropriately.

There have certainly been firms that have gone out with relatively high leverage recently, and some of those transactions have gone well and some have had challenges. We try to really think about what an appropriate capital structure is when we take a company public, and try to have that off the table as an issue so that investors are able to focus on the business and the growth going forward.

IFR: It seems that deleveraging has actually become more common at the IPO rather than it being an exit point for a private equity firm.

Morrison, Blackstone: It has been pretty well tested over time that you want to make sure the capital structure is appropriate when you’re going public, and frankly at any stage. So primary proceeds are the most appropriate form of issuance until the capital structure is incredibly conservative.

You raise the appropriate amount of primary proceeds to de-lever the balance sheet. At some point down the road you think more constructively about secondary share sales, because we want to improve liquidity and, like I said, return capital to our LPs.

Baird, Citigroup: When you think about earlier questions around fund flows coming out of fixed income and going in to equity with rates so low, it’s an odd moment in history with interest rates being as low as they are and the cost of debt being as low as it is. If you’re not properly leveraged, you can’t actually drive return on equity. It’s kind of weird.

So we’re at a moment in history where leverage is directly linked to a higher ROE. If you’re a believer in the classroom, like I am, ultimately return on equity drives P/E multiples at the end of the day, and growth rates are legitimate shorthand for getting at that.

But I think equity investors quickly figured out, particularly coming out of the crisis, that, “I’m not all together sure I want that debt paid off, because it will impair returns to me”.

Even though we’ve reached relatively record-setting levels of leverage in the IPO market, think about Allison Transmission. It was an all-secondary IPO. It was never an exercise to begin de-levering the company – and equity investors didn’t care.

IFR: We have also seen many dividend recaps before an IPO as a means to deliver value to a private equity firm’s limited partners.

Morrison, Blackstone: There is a sweet spot for leverage. You don’t want to go too high. Certainly the market is willing to accept more leverage now, given the economy looks better for a dependable business, and given low rates.

But also you don’t want to go too low, because you want to drive the appropriate return to the shareholder. You have the ability in a business that has very little leverage to potentially do a leverage recap as a way to return proceeds to the LPs and still not over-lever yourself.

You can work within a fairly wide range of the sweet spot.

Baird, Citigroup: What’s also interesting about the kinds of businesses that Blackstone owns and manages, even in the public market – and your peer firms manage – is that they’re all de-levered by the time they hit that first maturity tower. So equity investors look at a company that’s six/seven times levered today. When that first tower shows up in 2017, if you believe the forecasts – which you do if you’re buying the equity – it’s two-times levered.

So the refinancing risk – which is the real risk, it’s the risk we all lived through in 2008 when the markets closed – the refi risk is perceived as very low, regardless of how levered you are when you are pricing the IPO. That’s a sophisticated, legitimate, accurate mind-shift of equity investors in the last five or six years. The headline amount of leverage matters a lot less than the ability to de-lever over time.

Companies are doing great. Margins are great. Cash flow is great. Balance sheets are great, so financial leverage doesn’t present much financial risk in the minds of equity guys.

DeClark, Credit Suisse: I think investors seem to be more willing to invest in highly levered companies that are in cyclical industries and are benefitting from the economic upturn. In a recovery people are able to see that by 2017, for example, the leverage is down to two times.

IFR: So are there some solutions in the equity-linked world that can be used to help de-risk the balance sheet at the time of an IPO?

Schacter, Goldman Sachs: There are definitely ways to bridge the gap. We saw that in Intelsat, where we had US$172.5m of mandatory bonds offered alongside the US$400m IPO. That allowed Intelsat and its sponsors to take upside, as they were able to strike the conversion premium at 20%. They were able to retain that upside while still getting value for the mandatory offering.

The mandatory also created an ability to market to investors who knew the company from the fixed income world. A lot of high-yield investors couldn’t buy the equity, but they could buy the mandatory by charter. It opened it up to a whole new investor base, because income funds who couldn’t buy the equity could buy the mandatory.

It not only worked out for the sponsors and the company, but it was a real home run to get exposure to the deal for these investors who would have otherwise not been able to play it. It really bridged the gap from all sides.

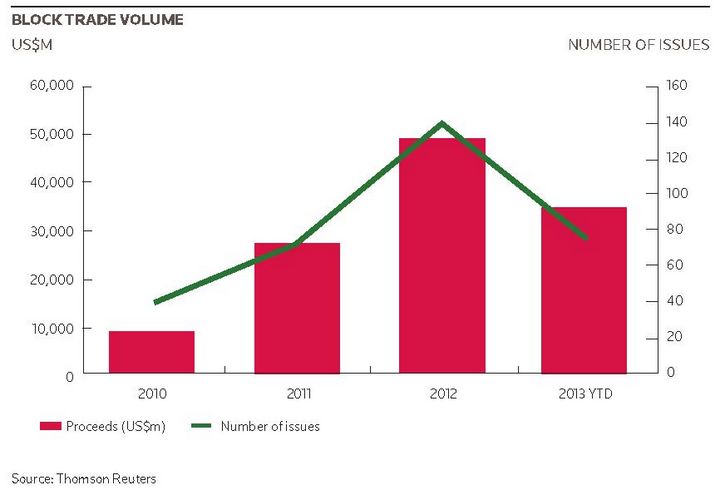

IFR: Private equity firms have obviously played a significant role in the ECM markets this year and have been particularly heavy users of block trades. How does Blackstone think about blocks, and what is the advantage of selling stock via a block trade versus a marketed offering?

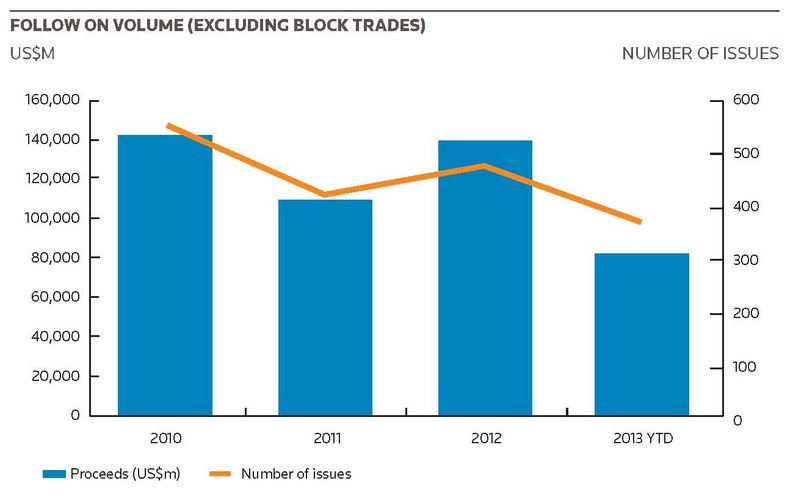

Morrison, Blackstone: The way we think about it is that there’s a typical lifecycle when you take a company public, the IPO being the first stage. Then you’re typically doing marketed follow-on offerings where you’re continuing to get the story out. You’re bringing more and more investors on board, so you’re seasoning the shareholder base and improving liquidity in the stock.

So once you’ve seasoned the stock appropriately – broadened the shareholder base and put an appropriate amount of liquidity in the stock – then you can start thinking about the block trade market. The block trade market allows you to move incredibly efficiently through the capital markets.

As part of the follow-on, typically you’re out talking to your best investors for several days, so you have market risk. It is great from an investor education standpoint, and everyone knows what the market is going to do over time. In a block trade you typically don’t have market risk. And as the stock has seasoned, you’ll have certain investment banks that have a constructive view on the marketplace and are willing to express that view by putting their capital to work behind block trades.

We are willing to have conversations with them, and their investors, to access that marketplace. It allows you to move very efficiently, from a time standpoint, through the market, and it is economically efficient from a discount standpoint. Because of the seasoned stock and the information in the stock, investors are willing to pay a tighter discount.

I think the block trade market is a great opportunity for us issuers to raise capital very efficiently.

IFR: So the lifecycle is: IPO, first follow-on is still marketed, and third trade goes block?

Morrison, Blackstone: I think you have to look at each stock individually. You have to see how seasoned a stock is and how well informed the investor base is. Today the information flow is as efficient as it has ever been. That helps. Investors will be more educated on what’s happening with a stock.

You also have to look at the marketplace and see how aggressive the investors and the investment banks are around a situation. But I think, certainly, we want to make sure that we’re doing an appropriate capital-raising, because we will typically still own more shares, and we care about the shareholders in the stock.

We have to be very, very thoughtful about this. But it’s an incredibly effective tool for us.

IFR: Why do you think investment banks have been so receptive to the block business?

Morrison, Blackstone: It really boils down to how constructive an investment bank is about the marketplace. The investment banks are incredibly well informed – lots of smart people working in them, lots of great research analysts keeping people posted with where the market’s going in the future. Investment banks are willing to express a view.

Secondly, from a league table standpoint, if you’re a sole bookrunner in a block trade, you can capture all of the league table credit – versus a traditional offering where you are one of several active and several passive bookrunners, and the league table credit gets diluted. But I really think it’s that first point that drives block trade activity.

Frankly, we see the number of block trade bidders broadening out as people become more and more constructive on the marketplace.

IFR: We’re in a pretty friendly market here, right? There haven’t been many landmines this year, have there?

Baird, Citigroup: You know, it’s awesome how smart everybody is when stocks go up every day. It’s been a long time, but there are a lot of super-geniuses – Wile E. Coyotes – out there these days.

I would say that a bunch of things have conspired to take the market in the direction towards blocks. The markets are generally more liquid every day. Liquidity is higher, although trading volume is a little bit more scattered than it has been. There’s just a lot of ways that people now access the market very quickly.

Investors become more sophisticated every day. They have their own research capabilities that are far more vibrant than a lot of big sell-side firms at this point. They know stocks well, they understand stocks well, they have their own models and their own sophistication around any issuer. They even own companies before they’re public now.

They have the ability to move quickly. Six/seven/eight years ago, you couldn’t get a buy decision overnight at a big mutual fund complex because they never had to do it and they didn’t know how. So now they have the personnel and the procedures in place that they can get a phone call, put you on hold, and then pick up as to size and price right away. I think the underwriters alongside that development have gotten better and better at it as well.

You guys do a great job in your daily piece about sussing out which banks missed it on a block. It’s obvious. They can give you all the rigmarole they want. But you can tell, in terms of price action and volume, that those guys are probably long. It hasn’t happened in size in the US in a while. It got a little choppy in Europe. I think a couple of guys got their fingers burnt. When that happens, there’s a natural ebb and flow of how much risk people choose to take on.

But all of the machinery – the owners, the sellers, the issuers, the underwriters, the investors – everybody’s gotten good at this. As Tom pointed out, it is an incredibly efficient way to have buyers and sellers meet.

IFR: Not that it ever happens to Citigroup, but what does it feel like to get burnt on a block?

Baird, Citigroup: I’m trying to think what that must be like. (Laughter)

IFR: No seriously, it is hard for us to understand what happens when an investment bank chooses to commit capital, makes a bad decision, and is left pregnant with a bunch of stock. Where does that stock end up?

Baird, Citigroup: I would say nobody bats a thousand. We talked about this earlier, even in marketed deals. How many people here have a Facebook page? Good. For example, you can have a widely oversubscribed transaction. Everybody loves it. Everyone’s indifferent to price. We can do whatever we want. But whoops, you can still get that wrong.

It’s Old Testament stuff, it’s really at the heart of what we do every day. You can have a marketed follow-on, which in many cases is much more difficult to price and stabilise than an IPO – because in an IPO, you have perfect knowledge about the book. You know how many shares every person has at what price.

In a follow-on, you can go out to stabilise a deal, and then everybody comes out of the weeds. You have no idea what people are going to do, even at the back end of a roadshow. So that’s why we get paid to do this for a living, because there’s experience and judgement involved, even if it’s not a block trade.

In terms of getting a block trade wrong, I would say: First of all, people rarely go in guns blazing in a block situation – and Tom will have a perspective on this. The seller knows who researches the stock, trades it, who has smart bankers around it, and whose opinion is likely to be credible. They know who just rode into town on Old Paint, you know, staggered out of the saloon shooting the gun: “I’ll buy a bunch at a price”. So they can sort of police that as well.

When people get it wrong, it’s not because they were reckless; it’s not because they were dopes. You don’t really get a chance to do it if you don’t know what you’re doing. It’s no different than US$38 for Facebook: sometimes you just, for some reason, read it wrong. Your intel out of the market is a little off, or some crazy thing happens, and you’re up overnight – and everybody’s under their desk eating baby food at the open.

Morrison, Blackstone: If an investment bank ends up with a slight residual from a block trade, typically they’re willing to be patient. They’ve won the block most likely because they have confidence in the company. They know the company, they think it’s going to do fine over the long term, and they’re willing to be patient. After maybe an initial dislocation, the stock finds its level and they work out an appropriate time and price.

DeClark, Credit Suisse: We try to be disciplined. Obviously – and as Doug said – you focus on the names where you have a good flow, you have a good analyst. Then if you do end up long, you have a way to hedge it or you’re comfortable holding it, because you believe in the fundamentals of the business.

Morrison, Blackstone: We think a lot about sizing a block appropriately and ultimately pricing the block. When an investment bank buys a block, we don’t want folks to end up long. We want the shares to be distributed to investors and not have a residual position and overhang with an investment bank.

IFR: So are there situations where you may not take the best bid?

Morrison, Blackstone: Yes, that happens every once in a while.

Baird, Citigroup: How tight are the bids? Is it like this awesome moment where, “Wow, look at that, everyone’s within a nickel” or is there always an outlier, a splay, or what?

Morrison, Blackstone: It varies. In some transactions it’s quite tightly bunched. And in other transactions, probably more than you’d expect, there’s a pretty wide divergence and a pretty wide set of outcomes.

Maybe one firm is really aggressive on a company, really believes in it, or a couple of firms do. Maybe a few other firms don’t have a great feel on the market at that point or they’ve recently been stung on a block trade and so they’re not as aggressive in that marketplace.

So it can be either tightly bunched or a wider range.

IFR: How many banks do you typically seek bids from when you conduct a block trade? Is it better to go to two, three, four, five…?

Morrison, Blackstone: I think you want to find a happy medium by going out relatively narrowly. Because you want to keep the information flow as tight as you possibly can, while balancing that against creating an appropriate auction, so to speak, to get a price that is most appropriate for our shareholders. There’s a fine balance there.

You will typically approach people who have been involved and know the company over the long term, as well as people who have been effective practitioners in the block trade market. There’s a nice balance between those who know the company well and those who are experienced in the block trade market.

IFR: Carolyn, what are your thoughts on the JOBS Act and how has this impacted capital formation?

Saacke, NYSE: Absolutely, after it was put into place in April of last year, people expected to see big results right away. What they really didn’t expect, and what they should have been looking for, is that change happens slowly.

Last year you saw a lot of issuers, who were already either on file or that even had already priced, go back and say, “Yes I’m an EGC, an emerging growth company” – and take advantage of certain advantages of the JOBS Act.

What we’re seeing now are companies filing earlier than they would have because of the opportunity that the JOBS Act has afforded them – either in terms of an on-ramp to some of the compliance work-throughs, or simply because they were able to file confidentially. They are investigating a potential dual-track process, or looking to see if whether being public is really the right thing for them, and taking a little bit more time on that decision than before.

So I think we’re going to see a lot more companies taking advantage of the JOBS Act in the future. It’s certainly here to stay. We’ve got 79 of the 100 IPOs that listed so far this year who had actually taken advantage of the JOBS Act and filed as EGCs. So that’s a great number. Again, a growing percentage of them are ones that probably would have not gone public when they did had it not been for the benefits of the JOBS Act.

To continue reading this roundtable, click the relevant section. Foreword - Participants - Part 1 - Part 2 - Part 3