IFR: Phil, we’d like to start with you, if I may. What has been driving the phenomenal levels of capital formation we have seen in the IPO market?

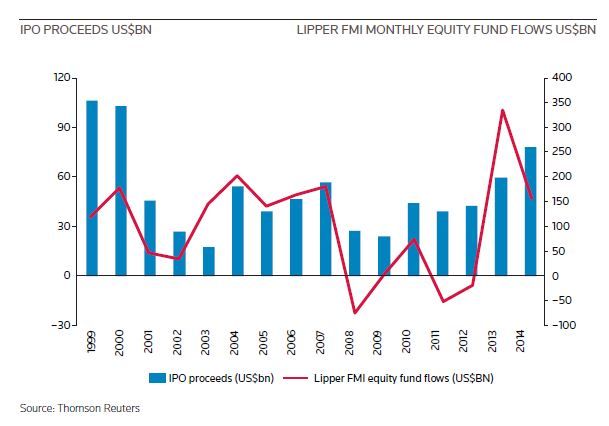

PHIL DRURY, CITIGROUP: As equity capital markets professionals, we’re pleased to have seen how robust IPO volumes have been in both 2013 and 2014. IPO volumes are up close to 20% year-over-year [pre-Alibaba]. It helps to have the S&P 500 setting new highs and breaching 2,000. Generally speaking, a lot of issuers, whether they be corporate issuers or sponsor issuers, are much more prone to issue equity when they see valuations are robust.

The healing process post-crisis is not just one that impacts equity valuations and our issuers. It obviously has an impact on investors as well. We’ve seen positive equity fund flows now in quite robust

fashion over the last two years. So we see a very healthy market with very efficient pricing. About 75% of IPOs [in the year to date] have priced within

or above their marketing range. All of those factors help produce the robust environment that we’re operating in today.

IFR: JD, it has been a great year for ECM, but on the other hand we did have a significant sell off from March to May in the momentum names, many of which were recent IPOs. What sort of impact has that had on the IPO market?

JD MORIARTY, BANK OF AMERICA MERRILL LYNCH: In order to understand what’s happened this year, you have to think about what went on last year. Last year was really the first year [since the financial crisis] that the IPO market diversified. It wasn’t just high growth companies going public. We suddenly saw industrial companies going public. There were also some very successful lower growth companies being well valued, which was probably a reflection of economic views here in the US. You saw that in the back half of 2012, and that powered us through 2013.

Notably, last year was the first year with 200-plus IPOs since that 2004 to 2007 period that we’d all love to get back to. Interestingly though, with the way the indices finished 2013, investors were chasing performance into year-end. That continued in the beginning of 2014. Pricing conditions were materially better in the first three months of this year than they have been since that time, and a disproportionate amount of the issuance was in technology and in healthcare. Somewhere on the order of 50% of the IPOs that came out were technology and healthcare in that period. Then you saw a massive reversal in not just the healthcare performance, but also in one sector that had been among the most prominent. That was software.

You saw this correction from, call it March 5, when the Russell peaked, to May 7. In that period, it became really challenging to price a technology IPO, and actually if you look at pricings since April 1, about 44% of deals have priced below their range.

You’ve seen the buyside extract a pound of flesh in pricings. Now the encouraging thing is, as Phil points out, we’ve actually seen a relatively meagre slate of technology companies come forward.

One of the companies mentioned earlier was Zendesk. While that performance has been extraordinary most investors did not participate in the IPO. Only a very narrow set of investors did. That’s true of most of the technology companies, or high-growth companies that went forward in that period.

Interestingly, we’ve had a somewhat challenged market since, call it April 1, for technology companies – companies like Mobileye proving the exception to that.

The encouraging thing is that other sectors continue to chug along and get public successfully. So that’s really a continuation of 2013 and the reason we can be excited about 20% higher volumes overall. It’s just a healthier overall capital market environment.

IFR: Joe, maybe you can elaborate a little bit on some of some of the sectors that have been active in the second half of the year and filled the gap?

JOE REECE, CREDIT SUISSE: You know it’s funny, I feel like whenever I do these things I realise how old I am. Something is happening and some of the guys up here will remember this. It started after what some affectionately refer to today as the GFC, the Global Financial Crisis. I’ve been in the business for about 28 years. I think I’ve seen eight 100-year crises, because every three or four years we have a 100-year crisis.

One thing I think is a little bit different this time is we’re seeing very, very robust demand by liquid investors for illiquid product. In the last 12 months, if you look at the 25 largest liquid long-only mutual funds and if you look at the 25 largest hedge funds by assets under management, there have been almost 300 issuances by private companies.

If you had asked five years ago if Fidelity, BlackRock or Wellington were going to put large sums of capital in an illiquid name the answer probably would have been no. Right? But what’s happening [now] is that in the search for return in an environment where there is no yield curve – when the yield is non-existent – people are chasing returns, and they’re chasing them in the private markets.

Ridesharing service Uber is a great example. Uber recently went out and raised a pretty large sum of money and now have an US$18bn valuation post-money.

Sadly I remember we had a 1991 energy tech bubble too. The difference now is that people are chasing valuation but they’re chasing it in real companies. Facebook, pre-IPO, there was a lot of activity. You may or may not have agreed with the valuation, but you also have to look at the structure. These guys are masters at saying: “Oh yes, we did a deal at US$X billion,” but then you look underneath the liquidation preference and all of a sudden it’s like: “Well, unless they go public at 30% of the value we priced it at we’re not going to lose money.”

The market, particularly for guys like BlackRock who sit on US$4trn of capital, is buying product that two, three, four years ago they wouldn’t look at, because one, the product wasn’t there, there wasn’t a calendar for it; and two, they had no appetite.

Alibaba is a great example. A couple of years ago they did a US$2bn private raise – US$2bn of illiquid capital is an enormous number, but that’s no longer the exception. We’re seeing it more and more, and my prediction is, not only will we see more, they will continue to perform well. As long as the [ECM] calendar on the back-end when they get to us [ECM desks] is there, I think you’re going to find investors continue to want that product. [They see it] as a way to get in early, to get a sizeable stake and to make money that they’re not going to make in the liquid market.

IFR: That’s a topic we definitely want to come back to. But first we’d like to talk a little bit about master limited partnerships and the more recent phenomenon of yieldcos – not quite as exciting but perhaps JD, you could offer some perspective on the asset class.

MORIARTY, BofA MERRILL: If you go back to the 2005/06 period, there was a ton of issuance coming out of shipping. Interestingly, shipping companies started doing MLPs offering yields at very high levels.

The whole concept was based on distributable cash flow, as in: “What’s your distributable cash flow yield?” These were much more volatile assets than traditional MLPs, and ultimately were bought largely by hedge funds. The difference now [with yieldcos] is much lower yields. One of the ones that we’re very proud of is NRG Yield. In all, there are five yieldcos out there right now. In some cases they are yielding, call it 100 basis points, over the S&P 500’s dividend yield. In this environment, where the 10-year Treasury yield is very low, that’s actually pretty attractive.

Because of drop-downs from the parent, these vehicles also have, call it 15% growth. As a result we have a better base of buyers for those deals than we saw in that period with the shipping companies. They were creating structures that probably weren’t appropriate for those assets.

MLPs and yieldcos are tax-advantaged assets. This is corporate finance looking at a large company and saying we’re not getting credit for this. There is clearly a bid for yield in the market, as we all know.

The question we’ve all discussed is: How many more will the market tolerate? I don’t think it’s a function of the buy-side [demand]. I think it’s a function of the quality of supply. How many parent companies can continue to identify appropriate assets that they drop down and that have a nice growth trajectory?

The interesting thing with the NRG IPO last year is that the mid-point yield on the IPO was 6%. It now trades with a two-and-change percent yield. After our July follow-on offering, it made a major acquisition. So it’s a really interesting opportunity for investors who are challenged to find yield in traditional sectors.

Now, it’s not all yield funds. That’s one of the things that people ask us: “Is it people that were buying banks and utilities before?” No. Investors need to understand the area. So it’s utility investors. It is infrastructure investors. It’s more than traditional yield funds.

REECE, CREDIT SUISSE: JD, what happens when – maybe eventually in my lifetime – rates rise? What happens to this calendar issuance opportunity for all these folks that have great sponsors and all these assets?

MORIARTY, BofA MERRILL: Well, it’s interesting. While we’re calling them yieldcos, 15 points of an 18-point total return is coming from the growth characteristics of the assets.

I agree issuance will likely drop off [if rates rise]. Hopefully we’ve got broad enough ownership in those assets that they will react much the way that their parent utility companies do. But it’s an interesting area where we’re certainly seeing a broadening of the investor base. That’s encouraging.

DRURY, CITIGROUP: As you say, the theme is total return; growth plus yield. But I do think the chase for yield in the equity markets is one of the biggest surprises of the year. If you rewind 12 months ago, when Bernanke came out and started suggesting we were going to be in a rising rate environment, REITs meaningfully underperformed.

Fast forward to today, and the real estate index has outperformed the S&P 500 by 1,000 basis points. So if you look back and say, “Okay, last year, what did you not expect to occur?” I think most people had rates rising 12 months sooner. Now everyone’s forecasts are back-end loaded for 2015. I think we’ve seen a nice combination this year of growth plus yield.

IFR: MLPs and yieldcos are a US$600bn asset class now. One of my Canadian sources mentioned that it might be a potential blood bath in terms of investor losses on a rise in rates, and that there would be a risk that some of these subsidiaries could be orphan companies.

REECE, CREDIT SUISSE: I don’t know. I’m going to agree with JD, because if you look, the last four times that there has been a rising rate environment, what’s interesting is that the MLP index has actually performed pretty well. There’s no issuance, though. There’s not new product. Yes, we’re focused on how the deals perform, but we’re also focused on generating product, because if we don’t then half of this roundtable would cease to exist, right, and Matt would probably be less busy as well.

[Rising rates] don’t necessarily mean performance falls off. There’s just no new product. In the last four rate increase environments, the product performed well that was public.

MORIARTY, BofA MERRILL: You have to look at what’s going on not just in terms of a retail investor looking for yield, because it’s diversified in terms of institutional interest there. The last time around on MLPs, in that 2007 period, we got institutions over the K-1 issue, but the institutions who got there were hedge funds. And then they went through 2008.

So we’ve rebuilt that buyer base, and if you think about the needs of endowments and others, in terms of a predictable return, that base of just needing yield is really substantial.

Issuance will trail off, but as long as the quality of the assets is there, the sector will be fine. I think the sector is actually, at this point, big enough that it won’t become orphaned.

JONATHAN ROSS, BLACKROCK: JD mentioned there is a technical dynamic as well, which is that the hedge funds might have gotten over the K-1 issue. I know we haven’t. It’s not a situation where our funds are necessarily prohibited from buying MLPs. They can and do. We own MLPs, but not in real size. The K-1 issue is just pervasive and people are concerned about it.

Because yieldcos are structured as traditional corporations, they have been very effective in alleviating that concern, so when we look at MLP issuance versus yieldco issuance, and we look at BlackRock’s participation, we’re still, in general, not the biggest buyer of yield assets, relative to our size. But it’s a significant delta between MLPs and yieldcos, and we’ve been a large participant in several of the yieldco deals, whereas if it were an MLP we’d be very, very tiny participants if at all. So alleviation of the K-1 issue via yieldcos is not insignificant.

IFR: Andrew, I’m sure you have some interesting perspectives in terms of low interest rates and what impact that has had on the convertible bond market. Perhaps you can elaborate a little bit from a historic perspective.

ANDREW APTHORPE, RBC CAPITAL MARKETS: As you know, the convertible market has certainly faced its challenges beyond the credit crisis. In the US, we’ve seen on average, annual issuance running at about 55% of pre-crisis era levels. Yet by comparison, over this same time frame, we’ve also witnessed the high-yield market, a close cousin to convertibles, almost triple its average annual issuance levels as corporates take advantage of low rates to fund their business needs.

One statistic I continue to monitor is therefore convert market issuance as a percentage of the high-yield market issuance. Pre-crisis we were running at about 60% of high-yield volume. Today, we are now closer toward 11%, so I’d say the convertible asset class in the US (and globally for that matter), has certainly faced its challenges over the last four or five years due to this low funding rate environment lowering the perception of relative value to corporate management teams.

That said, now with equity markets breaching all-time highs and M&A volumes on the rise, we have certainly found corporates more sanguine toward the use of the product for their various needs. So we’ve begun to see a notable resurgence in issuance off the recent 2012 low, but still I’d say, at levels below the crisis.

Interestingly though, in the last significant rising rate environment of 2004 through 2006, we did see average annual convertible issuance appreciate by about 25%; whereas when rates decline, convertible issuance has tended historically to be flat or down.

Looking forward, I am very optimistic on the prospects for our market, particularly when you consider volumes we’ve seen issued in the fixed income markets in recent years. If you aggregated the last five years of US high-yield issuance for example, we had about US$1.5trn of paper come to market. The outlook therefore sets up well for us, as we anticipate a heightened level of refinancing activity, almost certainly in a higher rate environment one to two years from now.

For a good rule of thumb, think about the scenario of a 100 basis point increase in interest rates; interest cost on a convertible bond would only appreciate by about a third to half of that move. So the best way for corporates to minimise interest expense and manage their EPS, is very likely via use of convertibles as we head into a different climate for rates.

IFR: One of the interesting dynamics in the convertible market this year has been the use of the product by technology companies. I think it started with ServiceNow. Andrew, could you walk us through what is happening here?

APTHORPE, RBC: I’m sure my colleagues across the Street will want to debate when it really began, but I’d say one of the very notable deals that sparked this recent trend in technology companies accessing the convert market, large caps in particular, was a $575m offering by ServiceNow in November 2013. While others have pushed the envelope before, they elected to fund their needs with a remarkable ‘zero-coupon/zero-yield’ convertible instrument, in combination with a 37.5% conversion premium. So although growth companies have been a mainstay in our market, this deal was one of the most aggressive pairings of coupon and premium we have seen since 2005, absent a AAA-rated offering from Microsoft. This offering galvanized interest, as others observed the art of the possible. Yahoo then followed roughly 20 days later with a US$1.25bn offering, elevating the bar higher still with a similar zero-coupon, zero-yield – what we used to call ‘no-no’ deals in 2003 (ie “no coupon, no yield”) – but substantial 50% premium. So pairings of coupons and premiums have certainly shown some robust follow through in this low rate environment, particularly for large cap, bellwether issuers that are Index eligible.

Another point, corporations are also using the convertible product to fund their share repurchase programs, a very topical subject in this cycle of finding ways to redeploy excess capital to shareholders. Citrix Systems is a great example. In their case, we raised them US$1.4bn with de minimis 0.5% coupon, high 50% premium, then, like others, augmented their structure via a separate equity derivative comprising a bond hedge plus a warrant, to take their effective premium to 100% above the share price at time of issue.

This additional call spread overlay strategy, as its known, allows bullish issuers to achieve premiums substantially above where rational market participants are willing to buy. So call it bridging the bid-ask divide if you will, between buyside and corporate expectations. Citrix then used proceeds to fund a concurrent share buyback, both on the deal and via an accelerated share repurchase strategy - a separate structure with its own merit. So this offering is a prime example, of a sophisticated issuer combing structural enhancements in the equity-linked market - like net-share-settlement (cash upon conversion), call spread overlay and ASR buyback strategies - to repurchase more common stock at time of issuance, than they would ever likely issue upon conversion. It is notable they chose to access our market for these benefits, over and above the investment-grade market.

In summary though, I’d say we continue to find ourselves in the hybrid world of equity-linked: On the one hand, opportunistic issuers using convertible bonds to lock in a low cost of capital, refi their existing debt, fund share buy-backs or for other general needs; and on the other, working with those that need to finance acquisitions or manage down leverage on their balance sheets with the use of more equity-surrogate like instruments, ie mandatory convertibles – and one of my favourites, the perpetual convertible preferred security. Either way, this market allows corporates to meet their needs, and I’m very optimistic on the outlook going forward.

IFR: Twitter is another high-profile convert issuer.

ROSS, BLACKROCK: I mean it’s free money, or close to it. If you’re Twitter, and you’re doing five years, and maybe you’re priced with 25bp coupon, maybe it’s a no-no, up 50%, you layer a call spread on top of that to take the premium to whatever, 75%, 100%. So if you’re [Twitter CFO] Anthony Noto, you sit there and you say, “Well, I can take a billion bucks in, and my cost of carry is essentially zero basis points.”

I think there is a bit of a ‘me too’ phenomenon as well for those companies. To a large extent, those companies are becoming increasingly more acquisitive as they try to build out their assets, and having that cash on hand is very helpful. Not for the big transformative sort of deal, not for like a WhatsApp [which Facebook acquired for US$19bn earlier this year], but if you’re out there spending US$500m or US$1bn, and you don’t want to use a lot of stock to do that, it’s nice to have the cash on hand. Particularly if the cost of carry is somewhere between 0 and 50 basis points to do it, that’s relatively cheap.

MORIARTY, BofA MERRILL: I think you started out by mentioning ServiceNow and a couple of software companies. But Priceline is probably the one that really started this. You really this year have seen a lot of M&A in internet land. That sector really hadn’t had M&A for three or four years – software certainly had – so the two go hand in hand, and it just makes a lot of sense on a certain scale.

IFR: There are a lot of technical aspects to these trades, and there are a lot of technical investors, but Jonathan, perhaps you can offer a perspective on the convert market from a fundamental point of view.

ROSS, BLACKROCK: Yes, fundamentally a 0% [yield] deal with a 30%–50% conversion premium is pretty challenging to get your head around. You’re looking at a dynamic where you’d probably prefer to own the stock. That said, we have participated in some of those deals – primarily through funds that are large equity owners already.

For the most part what they’re looking to do is swap some exposure, so it’s not really an either/or, it’s a case of: “I’m already a large equity holder, I can take down a large convertible. Yes, the premium may be reasonably high, but it changes my correlation profile a little bit, it’s going to potentially insulate me a smidge from stock price moves, yet I still maintain exposure to the name.”

The other thing it does from a technical perspective for some of our funds is it opens up participation. If I’m a high-yield account, I may have a hard time under my IMAs [investment management agreements] to otherwise invest in equity directly. But if someone is willing to issue a mandatory, or a convertible, even with a 0% yield, it now opens up capacity where previously I didn’t have any. So there’s a benefit on that front as well.

APTHORPE, RBC: I think it is a helpful perspective to hear the fundamental insight, but the market really breaks down into two distinct buyers, both technical buyers and fundamental buyers, as you’ve just heard from. Nothing really has changed dramatically in the last 20 years as to how investors really look at these instruments, and in some cases it’s a sum-of-the-parts valuation of the instrument first from the technical buyers’ perspective, coupled with an evaluation of the management team and the underlying prospects for the company.

So to the extent that it’s a technical trade, which many of these things are, you generally see allocations heavily skewed towards the hedge fund community. This also augments the company’s objectives of repurchasing common stock, as they look to buy back the stock from the hedge funds that need to de-risk their equity exposure.

On the fundamental side, clearly there has to be a fundamental view of the underlying common stock. [Some of these instruments] may have de minimis coupons, but you do get an aspect of unsecured bond protection. In today’s environment we find ourselves at an inflection point where there is debate on where the equity markets and the credit markets will go, a convertible is at the prime point of offering downside protection, yet continued upside exposure, if there’s a real stock view.

Also, and probably a shameless plug for Thomson Reuters, there is an aspect of investing in an index, and tracking an index. Thomson Reuters owns one of the benchmark indexes, and there is almost a captive audience looking to align with that index.

ROSS, BLACKROCK: We have some people at BlackRock who do take the technical perspective, so they’re going to consider participating in these transactions. From a fundamental standpoint, if we don’t already have exposure to the name, the convertible (and in particular, one of these tech convertibles that have very thin yields, if any, and high premiums) is not going to be our entry point into the name. We’re going to buy the common. We might participate if we’re already a very large holder, and the team is looking to perhaps swap some portion of the exposure out.

To continue reading this roundtable, click the relevant section. Introduction - Participants - Part 1 - Part 2 - Part 3

To see the digital version of this roundtable, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.