IFR: This is the fourth year we’ve held this US ECM roundtable, and the financial markets are seemingly challenged this time every year. In 2014, uncertainty surrounding China fuelled concerns about the sustainability of global economic growth. Last year, investor nervousness surrounding highly levered companies and the poor performance of IPOs began to hurt issuance. Indeed, those concerns continue to cloud the outlook.

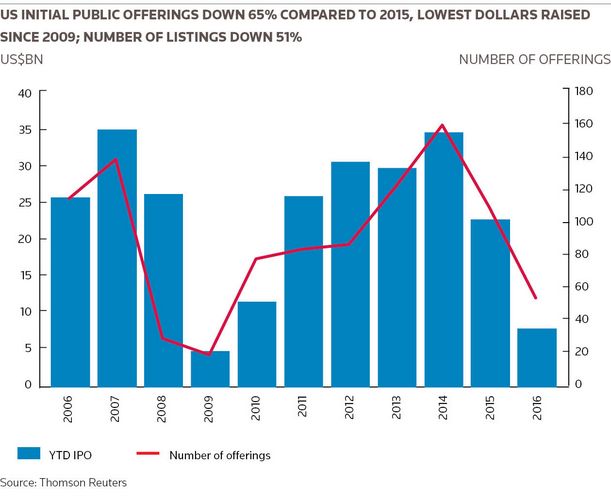

Now after a period of market tranquillity, equity capital markets face renewed fears of interest rate hikes, drawing the curtain on the post-crisis period of accommodative central bank policies. IPO volumes are down 65% year-on-year to US$10bn, a seven-year low, yet activity is picking up.

Confidential filing provisions of the JOBS Act, a seminal piece of legislation enacted nearly five years ago, means limited visibility into the forward IPO calendar. But members of today’s panel have visibility into that pipeline. Hopefully we can glean some insights into the rest of the year and into 2017.

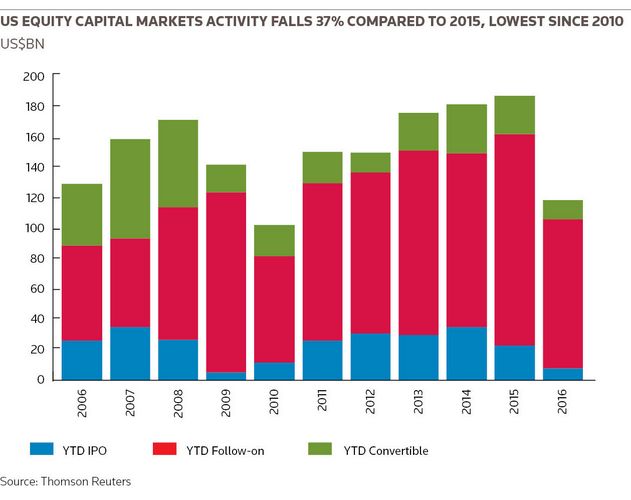

While much is made about IPOs, capital formation from a broader perspective remains as robust as ever. Responding to investor pursuit of alpha and a desire by sponsors and issuers for risk-free capital, investment banks have extended balance sheets to facilitate capital raising. Blocks and accelerated book builds this year have totalled US$48bn, more than half of all follow-on capital raised and up from US$42bn at this time last year.

With that I’d like to start the conversation with a question for Brett. At one time, there was not a day that didn’t go by when we didn’t talk about the lack of IPOs. That has quickly changed, but is there something fundamentally wrong with the IPO market?

Brett Paschke, William Blair: There is no question 2016 has been a real challenge. Year to-date IPO volumes are down 65% for the year and there have been 59 IPOs, excluding SPACs. For context, the last several years have been between 150 and 250. That became kind of the post-JOBS Act “new normal”.

A couple of things drove the decline. The 2015 class materially underperformed in terms of where those stocks traded relative to where they priced. Then there was a real flight to safety where you saw utilities and dividend-paying stocks driving things, and there was a bit of a back-off from growth names.

ECM professionals are accused of being perpetually optimistic, but if you look at the deals since July, they’re not just getting done but that they’ve been really oversubscribed. We’re back to the 10, 15, 20 times oversubscribed-type situations where you’re able to pick and choose the shareholder base and place the shares well.

As a result, you’re seeing very strong performance. The last I looked, I think 85% of all IPOs this year are trading above issue. Of the nine technology companies that have gone out this year, they are up on average about 100% from issue. Those are the conditions that you need to, one, encourage issuers to go out against a market that has been notable only for everyone saying how bad it was; and two, for the buyers to have confidence that the performance is going to be there.

Ashley Delp Walker, Jefferies: I would agree with Brett. If you strip biotech out of that, north of 95% of the deals that have priced this year are trading above issue. We’re seeing not only greater subscription rates, but we’re also seeing follow-through buying in the aftermarket from investors, something notably absent earlier in the year.

In the past we had deals that were five times oversubscribed and not a single buyer showed up at the open, which meant that you had a very strong transaction that unfortunately traded down on day one, ultimately caught its footing and traded well over time. We’re starting to see a return of strong aftermarket buying, people buying on the open, people following through with what they said they were going to do at the time of the IPO. This creates that nice aftermarket performance that we’re looking for.

The broader market conditions are ripe for issuance right now. You’ve got low volatility, significantly below 20, and I think you have to go back over 100 years to find volatility as low as we’re seeing currently. And very low intraday swings.

Brian Reilly, Barclays: My view on this is that the media has gotten it all wrong. Not IFR, of course, you guys never get anything wrong, but for many months now they’ve been talking about the lack of demand for IPOs. So, anybody in the room who is in ECM or syndicate, for the last three or four months have you had an investor tell you they didn’t want to buy an IPO?

Don’t raise your hand, because I don’t want you to prove me wrong, but that was certainly the case coming into this year. But since April, maybe May, certainly since June, the issue hasn’t been lack of demand. It’s lack of supply.

Why is that? Tech is normally 15% of the IPO market. This year it’s 5%. We don’t know what’s going on there. Over the last couple of years, companies have been able to fund their business plans in the private markets at valuations that are higher than what is achievable in the public markets.

Energy was 20% of the IPO market in years past. There has not been a single energy IPO across any sector since June of 2015 [Extraction Oil & Gas subsequently went public in October]. You could argue that’s demand driven, given what happened to the price of oil. But I will tell you, in our experience of the last few months, it was more that issuers didn’t want to launch because of valuation.

Private equity is 40%–45% of the IPO market in 2011–2015. Private equity issuance is down. Again that’s not because of demand; I think it’s just because of where we are in the cycle. You think about all the huge private equity-backed IPOs that we did. We worked off that supply and now we’re in the process of rebuilding it.

Finally, M&A. Think about the dual tracks that we did in 2012–2014. Virtually every single one of them went the way of IPO. Starting in the fall last year, they all went – most of them went – the way of M&A. Think about how many mandates we have all lost to the M&A market: SunGard, IDC, Blue Coat, United Guaranty. So, M&A taking supply out of the IPO market.

The good news is that’s changing. M&A is not changing; the M&A bid is still there. But energy is coming back; we just launched an MLP IPO last week. Again, [it was the] first energy IPO since June of 2015.

Tech is slow. It’s coming slowly but surely, but there’ll be a handful that will come. Those are companies where the VCs have gotten comfortable with lower valuations. There is still a whole bunch of high-quality internet and software companies that have zero appetite to go public at these valuations.

With private equity, we’re starting to rebuild the backlog, but it still doesn’t feel like what it felt like a couple of years ago. That’s going to take time. I do agree that conditions right now are ripe for the IPO market, but in my opinion, I don’t think we’re getting back to 2013 and 2014. It’s because of a supply issue and [won’t happen] until companies and VCs, particularly on the tech side, start to get religion around valuations.

My opinion is they’ve got to come down; I don’t think the market is coming up to them. We’ve seen that with the tech IPOs this year. They’ve been done at two to five times forward revenues. That’s not what most of our [corporate] clients have on their mind.

With the private market really slowing down, that’s going to cause more of them to come to market and be more realistic on valuation. Then, of course, you have the big internet companies rumoured to go any time over the next 18 months. None of these rules apply to them, but, generally speaking, I don’t think this is really going to start to come back, notwithstanding the demand. It’s not going to come back to 2013/14 levels, because the demand is at different valuations than where issuers are.

IFR: Nelson, the line between public and private companies has somewhat blurred in recent years. Mutual funds have invested in private companies, and there have been other trends that have seen a move towards more private funding, but then private valuations have come down more recently. What are some of the trends that you’re seeing?

Nelson Griggs, Nasdaq: A few years ago we launched what’s called Nasdaq Private Market. It’s a company controlled process that provides liquidity mostly to employees or early investors. It’s a growing space, but from 2015 to 2016 there was a really big change in terms of how companies were using it. It was mostly high-growth companies. About 40-plus programmes were using the platform. This year we’re at about 19. We think we’ll get close to 40, but the size of the deals is a lot larger.

We’ve moved towards a lot of it just being secondary capital raised and a lot of internal tenders where companies that are able to do this are the ones that have a better balance sheet right now. But it takes a lot more to get those done and it is a lot more challenging.

How does that affect the IPO market? Certainly the fact it has been harder to raise private capital means when you get to 2017 and beyond, companies are going to have to make a choice: Do they decide to go public or are they going to do an M&A transaction but at a lower valuation?

IFR: Can you discuss how the programmes work and how a private market solution would contrast to being public?

Griggs: The private market is much more about episodic transactions. Typically they’re going to be once-a-year programmes. We’re seeing them be semi-annual in some cases, and are in conversation with a few of the larger companies to consider quarterly programmes, so the idea of private liquidity is out of the bag.

We go in via the front door and work with the company and work with their counsel to run structured programmes. Just picture it as restricted stock for the most part, where employees or early investors need capital or liquidity because they’re staying private so much longer. They bought into these stocks because they thought they were going to have IPOs two or three years ago. They’ve got positions in some of these companies that are very outsized. It’s a very evolving, new space, but again Anna [can talk a lot] about that.

Anna Pinedo, Morrison & Foerster: We’ve found that Nasdaq’s private market is very helpful in terms of these secondary late-stage or mezzanine private transactions. What I mean by that is some of the crossover funds, or family offices, or other institutional investors that are investing in large, privately held companies are choosing to do so by purchasing securities that are held by early investors, friends and family rounds, angel investors, others that have held for a long time or where there’s some investor fatigue.

Nasdaq facilitates that tender process and so that does provide liquidity for early investors. It also helps sort of clean up the cap table, whether it’s looking forward to an IPO or looking to an M&A exit, so it reduces a lot of those early-investor stakes in the companies. I think that’s certainly a way to use the Nasdaq private market that has been very helpful for pre-IPO companies.

Going back to some of the points that were made, I do think that in many respects there is a very fundamental shift, and I think Brett and Brian both referred to it. Many of our companies now are privately held, whereas they might have started thinking about an IPO four or five years in and aimed for an IPO within their first five or six years. Now we’ve had companies that have been private for 10, 11, 12 years.

To Brian’s point, if private capital is available at very attractive valuations, then the incentive to go public isn’t there. Also, valuations in the public market – and this has happened with a number of our companies – have been less compelling versus [the terms of] the private capital they can get. They’ve been subject to IPO ratchet type provisions that are included in the arrangements worked out with the crossover funds and private investors. But you do get into an interesting new landscape where there’s significant privately held companies that have dispersed ownership and that don’t necessarily see a compelling reason to go public.

IFR: So Anna, one thing we’ve always been wondering is whether a lot of these private companies have to go public eventually or whether they can wait indefinitely. What’s your take on that?

Pinedo: A lot of investors that come into private companies have different trajectories in terms of their investment span. For a long time, the crossover funds would only come in if the IPO was within a 12-month, maybe 24-month time horizon or there was the possibility of an M&A exit.

I think, depending on sectors, many investors now understand that that trajectory could be extended, sometimes significantly, and they’re becoming a little bit choosier about the terms. Indeed, to some of the points that were made earlier, for some companies the crossover funds are just not available, particularly in certain sectors.

In any event, usually they will negotiate an IPO ratchet, meaning that if they came in at a price that turns out to be higher than the IPO price, they’ll get made whole functionally, so you might think about it as a make-whole. They’ll get more shares issued to them, which obviously could make the IPO less appealing to the company, less appealing to IPO investors.

There’ll often be M&A provisions so they get some protection on an acquisition; and governance provisions. Once upon a time crossover investors were not so anxious to be involved in a company’s governance process, but that’s becoming more common.

Because the crossover investors are not as enthusiastic as they once were, we are seeing more very large strategic investments in the most successful private companies.

Obviously, some of those have been in the news. We’ve been involved as a firm with quite a number of those. Those are very, very different from the perspective of negotiating the terms. There’s really no compulsion necessarily for a company that receives such an investment to go public. In fact, a strategic investment may be made with a view toward consolidation in a particular segment or something else entirely.

Griggs: Certainly it’s been much more expensive this year to get the capital.

IFR: Ashley, thinking about biotechnology companies or the types of companies that benefit from late-stage crossover investments – they seem to be prime beneficiaries – could you talk a little bit about how those crossover investments impact the IPO bookbuilding process? Walk us through that.

Delp Walker: A successful formula that a lot of the biotech companies have implemented over the last 12 months as the biotech funding market has become a little more challenging is to do a successful crossover round. Those crossover investors then tend to seed the public IPO round. It’s not that dissimilar from some of these unicorn tech IPOs. They just haven’t got to the point where they’ve gone public yet.

The expectation if you are participating in a crossover round for a biotech company is that when the company goes public you are going to make another investment. Then it becomes a question of around valuation and the step-up. Sometimes we’ve done a down round, although that’s been more the exception than the rule on biotech IPOs.

It can make the IPO challenging from the perspective of new investors coming in, particularly for a hot deal that is multiple times oversubscribed. New money feels like they should get a seat at the table and get a meaningful allocation; existing investors feel like they should get a meaningful allocation as well.

For a deal that’s not as oversubscribed, you’re seeing those transactions come together in a more club-like format, which has been more the norm this year than a deal that’s been 20 times oversubscribed for hot sectors like gene therapy.

For those transactions, for the most part, biotechs that have gone public this year have been spoken for at launch. It gives you certainty of execution.

Certainly, a number of those existing investors are comfortable being cut back if we get a lot of new money in. We weren’t seeing that trend in the first, call it, six months of the year. We’re starting to see a lot of people do a fair amount of work in the biotech market. We’re starting to see new money come in away from crossover investors.

That trend will continue, but certainly doing a crossover round and having visibility prior to launch of a biotech deal is still the norm in the market in order to have certainty of execution.

IFR: So definitely it sounds like it’s challenging under either circumstance, whether you have a club IPO or whether you have a hot IPO where investors are clamouring to get involved.

Delp Walker: It can be challenging. The club IPOs are less challenging. Existing investors know prior to launch that you’re going to have to fill them in order to get a transaction across the line. Where that’s more challenging is in the aftermarket when there is not a lot of liquidity.

For any new money that’s coming in for a club deal, they have to be coming in knowing that they’re going to have to hold it likely through data, because there’s not going to be any liquidity past the first day in order for them to get out. It takes on a different dynamic.

That’s one of the reasons that testing the waters is so important under the JOBS Act, because for these biotech companies it’s very difficult [for an investor] to make an investment decision in an eight-day roadshow.

A lot of people are reading the scientific papers, really digging into the data and really making a bet on the science, which is a difficult thing to do in an eight-day process. Testing the waters is definitely the norm in all biotech IPOs and has been very additive to the process in my opinion.

IFR: Joe, I know CCMP has a consumer bent in terms of its investment philosophy. Sticking with the provisions of the JOBS Act, how does CCMP utilise processes like testing the waters?

Joseph Scharfenberger, CCMP: The JOBS Act has been great for the size of companies that we invest in. We do middle-market buyouts and growth equity, so those are companies valued somewhere in the neighbourhood of US$250m to US$2.5bn. They don’t have robust finance staffs. They don’t have robust legal staffs. Usually, we partner with management teams that have family ownership or high insider ownership.

I’m not an expert on the JOBS Act, but it works very well for us on a high level. You don’t have the same executive compensation disclosure. The length of the disclosure that’s required is not as onerous. [There’s the] the confidential filing period, so you don’t have to announce to the market that you’re planning to go public. If it doesn’t work out or if there’s a change of heart or change of market conditions, it’s no harm, no foul.

We’ve used confidential filing on the last three or four of our IPOs and it’s worked out really well. It makes management feel comfortable that all their information is not out in the public, so it’s more of like a strategic tool for us. We did it with Ollie’s Bargain Outlet it was just awesome and it worked really well.

Reilly: I agree with Joe. By the way, I’m not an expert on the JOBS Act either. When the JOBS Act came out I thought it was going to be much to do about nothing. I felt that no legislation can create demand for IPOs. If a company is not ready to go public, there’s not going to be any demand. I was wrong about that and I think Ashley was spot on about the impact it’s had in the biotech market. I think we can all agree that the explosion in biotech issuance is not all because of the JOBS Act, but certainly the JOBS Act has helped there.

In other industries – and that’s how we’ve seen the evolution of testing the waters – we’re kind of using it for every company that we can use it for right now. What we’re seeing – and we saw it on a couple of IPOs that we did this year – is some long-only investors that otherwise would not come into the order book until late in the bookbuilding process are now coming in early.

I’m not saying this is happening all the time, but we have seen it happen.

That’s a benefit also on roadshows. We’re not going to Europe as frequently as we used to, or we’re using testing-the-waters as an opportunity to go to Europe and get some early orders in from European accounts.

Scharfenberger: Correct me if I’m wrong, but it extends post-IPO.

Reilly: Yes.

Scharfenberger: That’s also a huge benefit because companies get really nervous about Sarbanes-Oxley compliance. All these terms that you hear – Sarbanes-Oxley, executive compensation, disclosure, all the different requirements around executive comp – they’re really onerous post-IPO. The JOBS Act lets you stay a JOBS Act filer for a certain period of time well after you’re public. From a practical standpoint, it makes the whole process easier.

[Testing the waters] helps in getting the market educated upfront on your business. Again, I don’t know the exact specifics, but being able to talk to investors in kind of a roadshow format and take the temperature on how interested they are in your story. That is hugely beneficial because then it gives management teams confidence to go public.

That’s probably the thing that we struggle with the most in trying to get our companies public − getting the management team prepped and confident they can continue to execute on their business. They’re not going public simply to be a public company. They’re going public for a whole host of reasons, whether it’s capital raising, having a currency to do M&A, or to monetise their sponsor’s equity position etcetera. Their first focus area is to run their business, and the JOBS Act just makes them more comfortable doing that in a public environment.

Delp Walker: I hear feedback from the buyside all the time that they want to get to know private companies, and they want to get to know them as soon as they can, earlier and earlier in the process, across a wide variety of industries. So, there’s definitely a pull from the buyside as well.

To see the digital version of this roundtable, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@tr.com