Scaling new heights

In the space of a year, Saudi Arabia has established a debt management office, sold a jumbo syndicated loan and issued the biggest publicly syndicated sovereign bond deal in history. The Kingdom of Saudi Arabia is IFR’s Issuer and SSAR Issuer of the Year.

In November 2015, at the start of IFR’s awards period, the Kingdom of Saudi Arabia hadn’t even established a debt management office, never mind stunned the financial markets with a record-breaking transaction.

In the 12 months since, however, the kingdom has made its mark in both the bond and loan markets as no debut issuer has before.

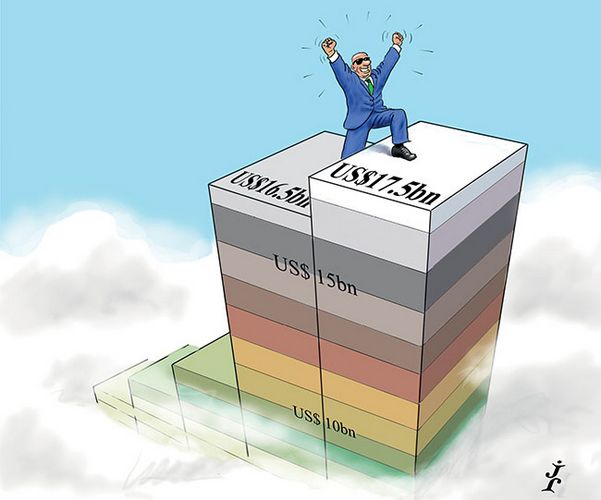

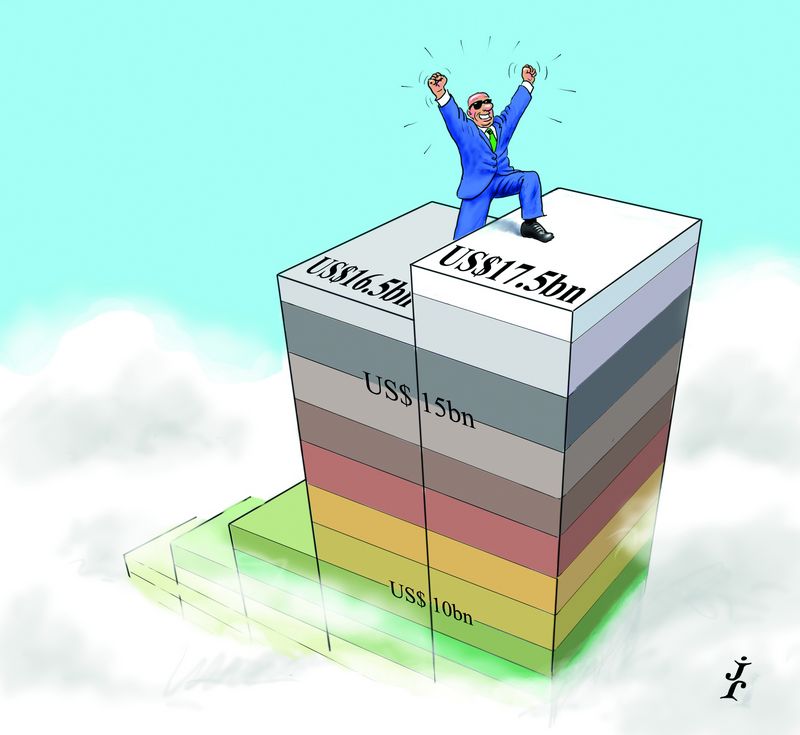

If its US$10bn syndicated loan in May was an early sign of appetite for the credit – initially Saudi was seeking to raise between US$6bn and US$8bn – the US$17.5bn bond deal in October left little doubt about the importance of the sovereign’s arrival on the international stage.

That transaction not only rewrote the record books; it created a new benchmark for the Middle East region.

Not that the DMO was thinking about making history as it developed its funding strategy after being established in December 2015.

Rather, it was mulling over issues around communicating the sovereign’s credit story to investors, especially in light of the broader narrative of structural reforms the country is undertaking as envisaged by “Vision 2030”, a roadmap to transform the economy and reduce the country’s reliance on oil.

One of the key pillars of Vision 2030 is the National Transformation Programme, which was launched in June across 24 governmental bodies operating in the economic and development sectors, with certain goals to be achieved by 2020.

For the Ministry of Finance they include strengthening public financial governance, increasing non-oil revenues, improving the efficiency of spending on government projects, safeguarding state assets and achieving sustainability of public debt.

Specific targets include attaining a sovereign credit rating in line with Aa2 – Saudi is rated A1/A–/AA–; and a government debt-to-GDP ratio of no more than 30% – it is currently 7.7%.

Establishing standards for public debt management was one of the first initiatives as part of the plan.

“We were extremely happy with the liquidity the transaction generated. It is now considered the benchmark for the region”

After it was set up, the DMO spent the early part of the year analysing different markets and put in place a plan for how to proceed. “We had a guiding principle to optimise our funding costs over the medium and long term. We wanted to target the most liquid markets,” said Fahad Al Saif, head of the DMO.

The first part of the strategy was the loan, which paid an all-in margin of 120bp. Qatar and Oman had already tapped the market, albeit via lacklustre deals, but the kingdom didn’t rely on those transactions as reference points and was able to increase the size of its financing.

“Yes, we were observing others but KSA has solid relationships with global financial institutions,” said Al Saif. “The reception was positive and exhibited broad geographic diversity.”

Coordinators of the loan were JP Morgan, HSBC and Bank of Tokyo-Mitsubishi. In total 14 banks participated.

Crucial to success

At the same time, it was establishing its global MTN programme and working on its potential bond transaction. In July, the team went on a non-deal roadshow to Singapore and Taipei, a trip that turned out to be crucial to the bond’s success.

“That trip gave us a tremendous amount of feedback,” said Al Saif. “We wanted to have the maximum flexibility in our execution and predictability in our analysis.”

One thing that became clear was that there was significant appetite for long-dated paper from Taiwanese life insurers. And by visiting them early, the Saudi team had given them time to get their credit lines ready.

Well prepared

When it came to the bond transaction, the Saudis were extremely well prepared. “We were very precise about when we wanted to issue, how we would convey our unique story, what messages we were willing to convey,” said Al Saif.

One of the key issues to think about was the deal’s size. “We want to access the markets on an ongoing basis. So we carefully analysed the market’s capacity. We also wanted to ensure we didn’t negatively affect our secondary prices, while being responsive to market demand,” said Al Saif, who added that the team considered a transaction ranging from US$7.5bn to US$20bn in US$2.5bn increments.

Pricing was based not on one reference point but a range of proxies, including regional peers, other emerging markets and oil-producing sovereigns, as well as G20 issuers – Saudi is a member of that international forum.

“The DMO’s responsibility is to ensure sustainable access to markets and that each time the KSA issues, it does so at a fair price – that is, the pricing reflects the progress of reforms as outlined in Vision 2030,” said Al Saif.

Thought through

Every aspect of the bond transaction was carefully thought through – from the roadshow where the team met more than 300 investors, to identifying the appropriate tranches, to issuing in the right window and the two-day execution process.

Initial price thoughts, for example, were announced just after the US open on October 18, with Asia, Europe and Middle East books going subject the following day. That enabled momentum to build and ensured there were no glitches.

Total demand reached US$67bn, with some accounts putting in US$1bn orders across different portfolios. Interest came from high-grade accounts, emerging markets investors, commodity funds, insurers, central banks and other financial institutions as the opportunity to get yield from a Single A sovereign proved compelling.

Five and 10-year tranches raised US$5.5bn each, while a 30-year note issue was US$6.5bn – the biggest bond at that tenor from an emerging markets issuer and reflecting the importance of that trip to Asia.

The sizing of the tranches turned conventional wisdom on its head but the nature of the order book, and the stickiness of that demand, meant it made sense.

Interestingly, Saudi priced the 30-year at the same spread as where higher-rated Qatar (Aa2/AA/AA) printed its 30-year bonds in May – at 210bp over Treasuries. And at 4.5%, the coupon on Saudi’s 30-year was inside the 4.625% on the Qatar June 2046s.

The 10-year note had the broadest appeal across investor types, while the five-year bond was particularly attractive to regional accounts, although in the final allocations US and European investors were given the biggest chunks. Citigroup, HSBC and JP Morgan were the global coordinators.

Follow-through demand

As important for the Saudis, all three tranches performed well in the secondary market, with follow-through demand from Asian and regional investors in particular, until rates began selling off some weeks later.

“We were extremely happy with the liquidity the transaction generated,” said Al Saif. “It is now considered the benchmark for the region.”

With its annual fiscal deficit for 2016 forecast to be US$87bn (on top of the US$96.6bn deficit in 2015), the Kingdom will return to the capital markets. Products such as sukuk are being considered too. Plans, however, have yet to be finalised.

“We have a lot of ambitions,” said Al Saif. “But we are cognisant of doing things gradually. This is a cycle.”

To see the digital version of this review, please click here.

To purchase printed copies or a PDF of this review, please email gloria.balbastro@tr.com