Deutsche Bank’s corporate banking and securities operation has been plunged into uncertainty after the shock resignation of the bank’s co-chief executives just weeks after unveiling plans that put the struggling business at the heart of the firm’s strategy.

Anshu Jain will step down at the end of June, while Juergen Fitschen – who is on trial in Germany charged with giving misleading evidence – will stay on until next May, by which time the case is expected to be over. He denies the charges.

The resignations come after the two had been in charge for just three years, during which both repeatedly failed to hit their own targets. Their short tenure was marked by three major strategy overhauls, two rights issues and billions in fines for misdemeanours.

Disgruntled shareholders boiled over following the latest strategy overhaul in April, which, despite five months of work, was short on detail. Nearly 40% of investors voted against the leadership in the May AGM. Two weeks later, the co-CEOs resigned.

“We have previously raised concerns about the management board’s delivery on key targets set under the 2015-plus strategy, progress on culture change and the way in which it has dealt with pending litigation and investigations,” said Hans-Christoph Hirt, a director at Hermes EOS, which represents more than 40 institutional investors.

“It had become increasingly apparent in recent months that refreshment at the top of the management board was necessary in order to regain the trust of investors and other stakeholders and thus have a basis for the successful implementation of Strategy 2020, unveiled in late April 2015.”

One senior banker at Deutsche paid tribute to Jain, but said that the bank had little choice but to move on: “Anshu was the creator and very smart. But he lost credibility with investors and regulators,” he said. “When it happens that publicly, there was a growing feeling that regardless of what we did, he couldn’t get it back.”

Too little

The April overhaul was particularly criticised for its light treatment of CB&S, the investment bank that was largely built by Jain. Although the strategy aimed to slash the unit’s leverage exposure, cuts were to come from disposing of low-yielding assets and rolling off positions. No businesses were culled in the latest strategy overhaul despite widespread calls for such action.

John Cryan, a former financial institutions banker and chief financial officer at UBS in the years immediately after the financial crisis, will take over. His first task will be to decide what to do with a strategy that clearly did not have the backing of shareholders.

According to one insider, CB&S bankers and traders are bracing themselves for big cuts.

“Anshu only ever trimmed around the edges of the investment bank,” said one person who has worked closely with him. “John will need to do a lot more to please shareholders. A lot of people are now worried about how much balance sheet they are going to have; what resources they will have after further cuts that are inevitable.”

The truth or otherwise of that statement depends, of course, on the definition of “round the edges”. A Deutsche spokesperson says that Jain and Fitschen have closed down the bank’s single-name CDS business, exited from commercial paper, significantly scaled back its European rates trading team and shut down the commodities business.

It is certainly true to say that the investment bank has not been the worst-performing part of the group over the past few years – that ignominy went to the retail and small business unit that Jain and Fitschen wanted to largely get rid of but were blocked by regulators from doing so.

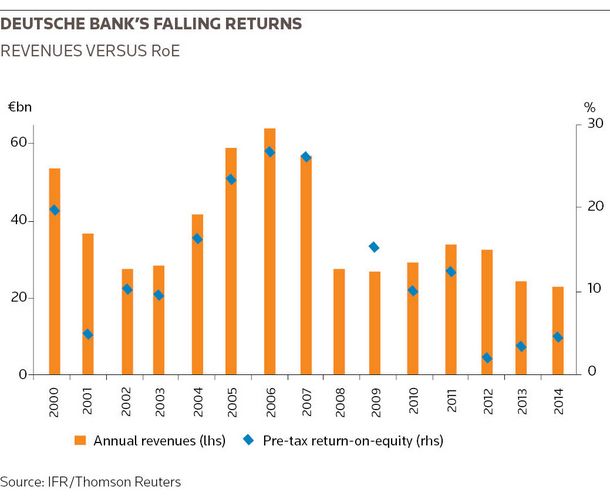

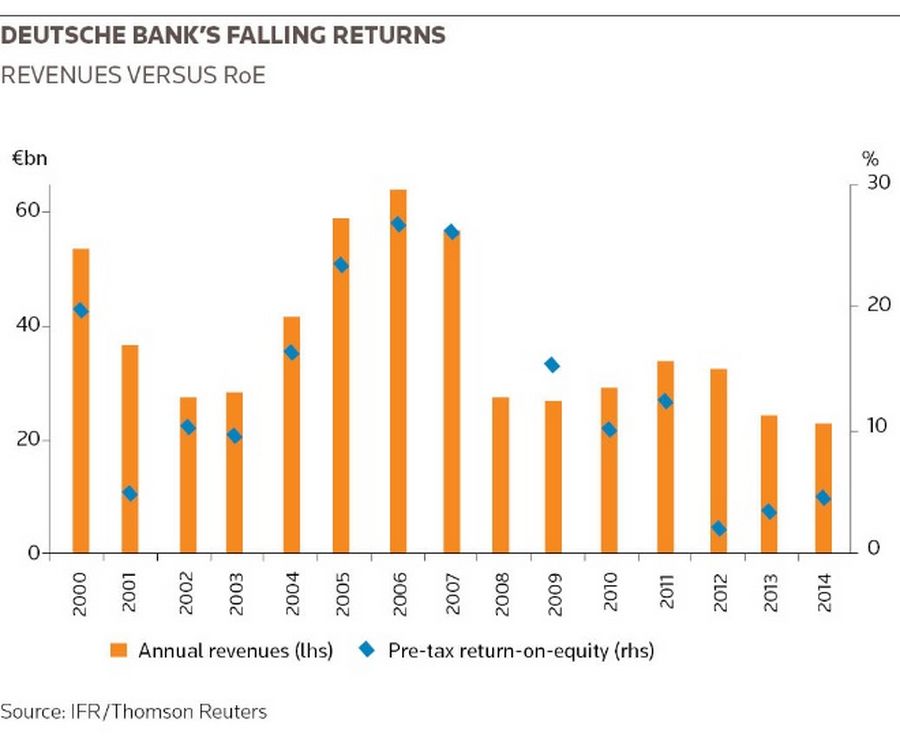

Still, a dramatic fall in revenues at CB&S has hit the group hard. At its height, the investment bank pulled in €21bn in revenues a year, but that fell to just over €13bn last year. Fixed income, Deutsche’s biggest breadwinner, has been the most affected.

With the non-core unit – largely made up of CB&S assets – bleeding money and the bank frantically building up capital to meet new rules, returns have collapsed. Return-on-equity during Jain and Fitschen’s three-year tenure was the worst in a decade.

Deutsche bank’s falling returns

Deutsche bank’s falling returns

CB&S, where returns were most severely affected by new regulations (in particular, restrictions on leverage levels), became the focus for many who believed that Deutsche needed to replicate the deep cuts – especially within the investment bank – made by rivals such as Barclays, Credit Suisse and UBS.

Lost patience

But the two co-CEOs were not convinced. Their vision was to be the last big European trading house standing and eventually reap outsized rewards. For those who believed that trading would thrive again once developed economies recovered and interest rates returned to more normal levels, it was a rational strategy. But with the blip of an upturn in trading in the first quarter of this year looking to be just that – a blip – too many investors finally lost patience.

Cryan’s task will now be to decide what balance to strike between “doing a UBS” – banking shorthand for slashing trading operations – and sticking with the last-man-standing strategy.

“Anshu Jain never adapted to the post-crisis investment banking world and was still going in all of his businesses for market share, revenue maximisation and league tables, while all other banks were trying to restrict their resources to the businesses that could generate good returns in the new regulation while exiting all the others,” said Dirk Becker, an analyst at Kepler Cheuvreux.

“The hope of investors today should be for the new CEO to amend the strategy and announce cutbacks in the investment bank in businesses that have become unattractive under the new regulation,” he said.

It is not a certainty that the new boss will make deep cuts, however. Cryan, after all, has been a member of the bank’s supervisory board since mid-2013, and signed off both on the rights issue last year and the Strategy 2020 plan in April.

Charmer

Current and former colleagues speak highly of Cryan, with one person who used to work with him calling him “a charming man, a genuine genius whose brain can compute massive numbers very quickly”. Deutsche investors will be hoping his FIG background and time as CFO of UBS, combined with a lack of allegiance to any part of CB&S, will allow him to make the precision cuts that need to be made.

“As Cryan comes, in contrast to Jain, from the advisory side and not from the trading side of the investment bank, the deleveraging within Deutsche Bank’s investment bank unit CB&S could be higher than the €200bn announced in the Strategy 2020,” said Commerzbank analyst Michael Dunst.

Cryan has been known to offer forthright views. Despite being an adviser to ABN AMRO, he warned RBS CEO Fred Goodwin not to buy the Dutch bank because he was convinced the UK firm was ill-equipped to deal with its problems, according to former colleagues. He was proved right.

“He’s really smart – but doesn’t make you feel like an idiot,” said one senior banker who has worked with Cryan at Deutsche. “He’s very smart at cutting to the nub of the problem. There’s a hope here that he takes a look, makes decisions that need to happen. [And there’s] no more paralysis. He’s not wedded to these business lines.”

Colleagues who worked with Cryan during his nearly three-year long stint as CFO of UBS consider him to have been central to the rescue of the Swiss bank from near-oblivion. “The turnaround was down to him and [CEO] Ossie Gruebel,” said one former colleague.

If he does decide to make deep cuts to CB&S, he might even find some allies from within the unit. Colin Fan, who has co-headed the unit since Jain moved up in 2012, has voiced to colleagues a desire to make bigger cuts to the investment bank. Some believe a micro-managing Jain prevented him from doing his job.

“Colin will be released by the departure of Anshu,” said one colleague.

Upbeat

Asked about the mood in the bank after the shock had worn off, bankers at Deutsche said people were upbeat. “Internally, the majority of people are thinking ‘about time’,” said one banker at the bank.

He added that a lot of people were desperate for Cryan to provide new leadership. “There’s hope that Cryan will take a look, make the decisions that are required, and end the paralysis,” said another Deutsche banker.

Another question now that Jain has gone is how quickly there will be changes to what some consider to be a dog-eat-dog culture prevalent in the investment bank and linked to Jain’s demanding management style.

Fan has been vocal about the need to change the internal culture, famously making a video in 2014 highlighting the need to change. But staff on the ground complain that there has been little improvement. They also say that a lack of a collegiate approach has had a damaging impact on the way the business is run.

As well as trying to institute a change in values, insiders argue that the new regime will need to tackle the convoluted structure within the bank.

Deutsche built a complex regional structure with country managers, overlaid by global markets. The elaborate resulting matrix means that there are several overlapping layers of management and business lines.

Building a flow monster

Jain’s future is unclear. He leaves Deutsche after 20 years at the firm, having joined from Merrill Lynch in 1995 to work within the bank’s newly established fixed-income business. Two years later, he became global head of the institutional client group, and expanded fixed income into foreign exchange and credit derivatives.

In 2000, Jain was appointed global head of derivatives and emerging markets, where he leveraged Deutsche’s commercial banking licences set up in the 1960s to build local sales and trading franchises in the emerging markets. After only six months, he became head of global markets for fixed income.

In September 2004, he was appointed co-head of the corporate and investment bank, together with Michael Cohrs, and given responsibility for equities and integrating it with fixed income. The combined global markets division went on to generate record revenues. When Cohrs stepped down in 2010, Jain took over the entire division.

The events of last week should not entirely overshadow the remarkable achievement of building a “flow monster” that connected international and domestic trade and foreign exchange flows to create a hugely innovative business that became for a period before and immediately after the financial crisis extraordinarily lucrative – and Europe’s only real challenger to the might of the US banks.

Unfortunately for Jain, the high-octane business he built, with its focus on seizing short-term opportunities and market share and its reliance on high leverage, was unsuited to the less swashbuckling world in which the banking industry has found itself.