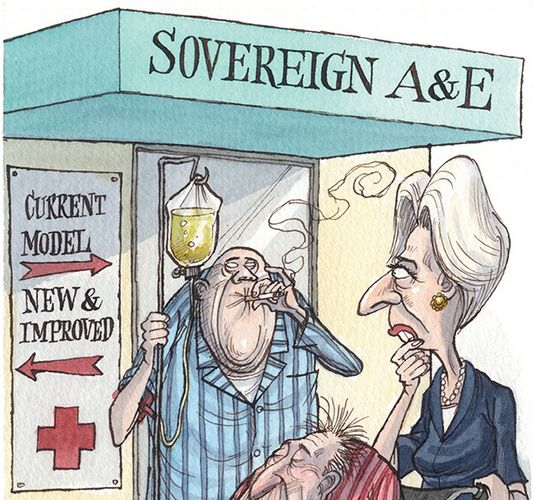

Holdout investors in recent years have done better than those that accepted the terms of sovereign debt restructurings. That has prompted renewed efforts to change the system, level the playing field and bind in defiant creditors. But can the reforms actually work?

The apparent success of holdout investors in the sovereign debt restructurings of Greece and Argentina has re-ignited talk about the need to reform the system, and to do so quickly.

But advisers involved in the process say any changes will take years to take effect – and ultimately might have little impact on how restructurings are carried out anyway.

Holders of some €6.5bn par value of Greek bonds managed to escape the estimated 70% haircut dished out in the country’s 2012 exchange – the biggest sovereign restructuring ever.

And, thus far at least, holdouts that refused the terms of Argentina’s 2005 and 2010 restructurings have made a good go of it in court. While they have not been paid themselves, they have lately been able to block exchange holders from getting paid as well, while tying the sovereign up in years of legal battles.

Those “victories” have underscored how difficult it is to make restructurings apply equally to all – and made it even less likely they will hold together down the road.

“It emboldens people to hold out in the future,” said Yannis Manuelides, a partner at law firm Allen & Overy.

New and old ideas

When Argentina first defaulted 13 years ago, the IMF – the traditional lender of last resort for sovereigns – considered establishing a formal sovereign debt restructuring mechanism, similar to the US Chapter 11 corporate bankruptcy protection process.

While pressure from the US blocked it, the IMF hinted at a milder version in a 2013 staff paper suggesting sovereigns would only get IMF funds if they extended the maturities of their outstanding debt. So-called re-profiling would save the IMF and the sovereigns both money and time.

This has also been widely rejected, though many believe re-profiling, without an automatic element for all recipients of IMF funds, could still be a useful tool with which to address the problem.

“This is precisely what was done dozens of times in the 1980s and early 1990s,” said Lee Buchheit, a partner at law firm Cleary Gottlieb. “No one pretends that it will solve a sovereign debt problem, but it will give the country and the IMF some time in which to assess the seriousness of the situation and the effectiveness of the programme.”

Instead, the International Capital Markets Association received a warmer reception – including backing from the IMF board – for reforms to sovereign debt contracts.

The ICMA wants it made explicit in future bond documents that use of “pari passu” language confers equal legal status on bonds – but does not entitle them all to the “rateable” payment that the US courts have adjudged applies to Argentina’s bonds.

ICMA also urges collective action clauses (CACs) to aggregate votes across different series of bonds in exchange offers. Bondholders blocked 17 of 35 series of foreign law bonds in the Greek exchange, for example. But with an aggregation clause in its domestic law bonds, the sovereign got approval for the 2012 restructuring via one simple vote.

“This approach is a standard tool in corporate bankruptcies in the US and elsewhere,” said Mark Walker, a partner at Millstein & Co who advised Greece on its restructuring when at Lazard. “Endorsement of the concept of aggregated CACs by ICMA and the backing of the IMF are extremely positive steps.”

Just after the IMF blessed the contractual changes in September, Kazakhstan debuted in the international markets and incorporated the recommended clauses in its documents, after advice from law firm Morgan Lewis.

Yet other sovereigns may be more cautious. The proposed clause has no option for holding a second vote with a lower quorum or reduced threshold, as is standard in most CACs.

“Getting 75% of all bondholders to vote may be hard,” said Francis Fitzherbert-Brockholes, a partner at law firm White & Case.

And this might mean that aggregated CACs end up being more investor-friendly than intended.

This may not be the case for eurozone issuers, which have already had to include their own version of aggregated CACs, with reduced quorum provisions, since the start of 2013.

“I don’t think the eurozone will adopt [the ICMA version], as they have just gone through their own reforms,” said Allen & Overy’s Manuelides. “Amending the European Stability Mechanism treaty, involving political votes across Europe, would be the only way of doing so.”

Playing politics

Without a definitive mechanism in place, of course, sovereign debt restructurings will continue to be at the whim of political considerations that inevitably leave some investors – and indeed some sovereigns – better off than others.

“We are back to case-by-case situations where exceptional circumstances can lead to some very politically driven decisions that do not necessarily make debt sustainable,” said Gabriel Sterne, who used to work at the IMF but is now head of global macro at Oxford Economics.

And the political dimension has become even more important (and complicated) with the rise of bilateral lending from one sovereign to another, which has made it even easier for bondholders to avoid having to settle for restructuring terms.

“Domestic political considerations can often be the single biggest factor discouraging a highly indebted government from acknowledging and addressing its financing problems in a timely manner,” said Sebastian Espinosa, managing director at White Oak Advisory.

At the start of its political crisis in 2011, for example, Egypt initially turned to Qatar, via bond financing, rather than the IMF. China has become ubiquitous. And bondholders got off easily earlier this year over Ukraine, one of whose major creditors is Russia, as the two nations teetered on the edge of war.

“It’s tricky when your biggest creditor is also your political opponent,” said one adviser.

“I suspect the US and Europe did not wish to aggravate a tense geopolitical situation by forcing Ukraine into a debt restructuring,” said Cleary Gottlieb’s Buchheit. “The moral hazard concern pales in significance to the political concern.”

“The obvious trend in recent years has been for taxpayers to bail out bondholders. This is a sharp departure from past practice. In the dozens of sovereign debt restructurings in the 1980s and early 1990s, creditors were told to reschedule their exposure. The official sector took a hard line that taxpayer money would not be used to indemnify bad credit decisions of private sector lenders.”

But bondholders in perennially troubled sovereigns such as Grenada, which is in default again, may not be so lucky. Such countries tend to be drowning in other debt as well, leaving all classes of lenders at risk of taking a bath.

“Some countries have too much senior multilateral debt in their debt stocks to be made solvent on conventional debt restructuring terms,” said Brett House, senior fellow at the Centre for International Governance Innovation.

To see the digital version of the IFR Review of the Year, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.