Heightened sovereign risk has played a major role in driving spread movements within the covered bond sector. Contagion fears from the Greek crisis have rocked confidence and increased volatility in the European peripheral government bond markets of Portugal, Italy, Ireland and Spain. Hardeep Dhillon reports.

Primary market issuance in the peripheral countries started strongly this year, with 14 jumbo covered bond transactions totalling €17bn launching, compared to a total issuance volume of €72.2bn from 59 deals year to date. Nine deals have originated from Spain, three from Portugal and two from Italy.

January and March were the strongest months for issuance, with five and six deals respectively. February saw a single transaction and only two were issued in April. The last benchmark from the periphery region was launched on April 20.

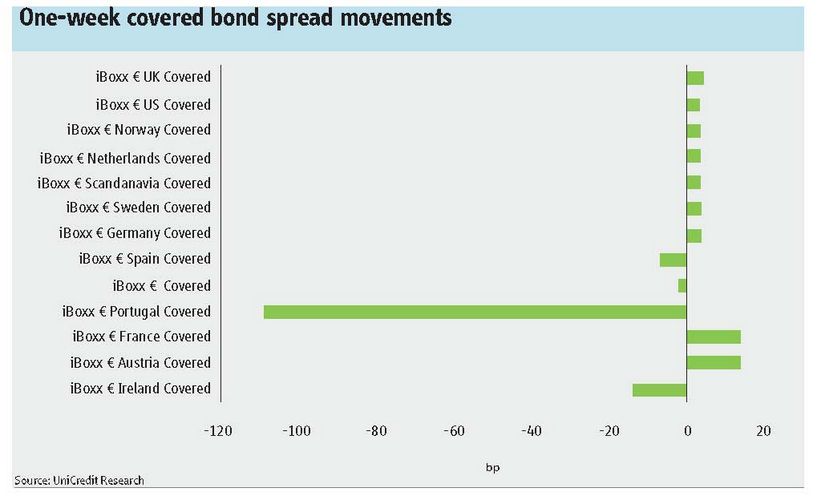

Portuguese covered bond spreads have experienced the greatest volatility since January, moving from a low in the 50 basis points area, peaking in the 350bps and moving back down to the 200bp area. Spanish transactions have also widened significantly (for more on Spain see separate feature). Volatility has had a considerably lesser effect on Italian deals.

By May 27, Banco Portugues do Investimento’s five-year offering widened from a January launch spread of 62bp to 216bp over mid-swaps (MS). A ten-year deal issued by Caixa Geral de Depositos in the same month at 80bp over MS was trading at 193bp, while Banco Santander Totta’s three-year deal ballooned out to 187bp over MS from a launch spread of 85bp in March.

Santander Central Hispano’s five-year issue came at MS plus 50bp in January and widened to 145bp by May 27. Its seven-year deal launched in March at MS plus 75bp was trading at 142bp. In the Italian market, Banco Popolare launched at 82bp over MS in February and tightened in to 65bp by May 27, while Intesa SanPaolo’s April deal softened from MS plus 50bp to 57bp. Both were seven-year deals.

Ireland has yet to launch a covered bond this year. However, its banking sector is not heavily reliant on the covered bond market, having access to other funding sources. Irish issuers view covered bonds as an additional funding instrument and will wait until market conditions improve, said Ralf Grossmann, head of covered bond origination at SG CIB. “Investors still question investing in Ireland given the current uncertainty,” he said.

Although Italy has high debt and deficit ratios, there is more confidence in the sovereign. Despite there being less covered bonds spread volatility, movements are also reliant on the government market: many Italian banks pre-funded last year and with asset swap spreads of the sovereign debt currently at relatively wide levels, thus providing only small pick up over covered bonds, more momentum is required before the market re-opens for domestic issuers, said Grossmann. “There are covered bond offerings in the pipeline but issuers are now waiting for greater stability and delaying launch until the third quarter or even later,” he said.

There has been a greater level of differentiation within the covered bond sector. This has mainly been between those markets assumed to be most vulnerable to contagion risk to Greece – namely Iberia. Though spreads tightened after the first week of May, bankers believe it is too early to tell by how much they will recover. This will depend on the successful outcome of government measures and the impact of the European Central Bank’s €750bn in sovereign support, provided by its Securities Market Program. “Even if the picture becomes brighter, greater differentiation between covered bond sectors will remain,” said Heiko Langer, senior covered bond analyst at BNP Paribas.

Analysing what actions politicians will take to rescue the periphery states is a new problem that investors must factor in to the pricing of covered bonds. “Over time a revival of spreads over the domestic government market is achievable,” said Torsten Elling, head of covered bond syndicate at Barclays Capital. “Covered bonds have the potential to perform and outperform the sovereign debt, given the fact that covered bond issuance is more limited than the amount of cash that might needed by some sovereigns.”

Closed primary market

Market volatility has curtailed issuance and effectively closed the covered bond market since the final weeks of April. This closure has been painful because of the heavy redemptions and the quantity of cash waiting to be invested in the market.

However, things could change quite quickly. “Volatility is making it very difficult to launch deals but more stability in the government markets could lead to a huge amount of supply from the core covered bond markets,” said Richard Kemmish, head of covered bond origination at Credit Suisse. “The question is whether that will set the conditions for banks from the more distressed markets to start issuing. I suspect it probably will. It needs one issuer to send a signal that it just makes sense to launch even at a materially wider spread.”

Many investors have become sceptical of the periphery states because of their structural problems and debt concerns, leading many to focus their attentions on core markets. However, investors should differentiate between issuers within the periphery markets, said Ralf Welge, head of financial institutions origination at Commerzbank. The market is not necessarily completely shut for every issuer: there are higher quality institutions with international banking models and diversified income streams that are not reliant on domestic markets.

Therefore, if market sentiment begins to improve then a Portuguese or Spanish issuer could become very attractive, Welge said, by offering appealing spreads. “This occurred at the start of the year, when even some core issuers were not offering such attractive spreads as Spanish or Portuguese banks,” he said.

Given that yields are forecast to remain at historical lows, investors will have to start to buy risk again. That is already being seen in the market, with purchases of corporate and asset-backed security debt. “With a normalisation of the market, we will see spread buyers return and they will definitely look to covered bonds. Levels will be attractive and enable investors to ramp up their average performance and average yield they receive from their investments,” said Welge.

National champions and better-perceived names, such as Santander or BBVA in Spain or Intesa SanPaolo and UniCredit in Italy, could re-open the market, predicted SG’s Grossmann – but at wider spreads than at the start of the year. These credits would re-price the market and provide investors with a comparison for subsequent issuers. “It is better that a national champion sets the momentum, although you cannot rule out a smaller player. But I do not envisage a third tier bank re-opening the covered bond primary market,” Welge said.

Correlation concerns

The general lack of confidence in governments’ ability to rein in budget deficits and manage debt burdens is holding the covered bond market hostage to the fortunes of the sovereign market. Spread movements in the covered bond markets have closely tracked the respective sovereign bonds, albeit with a certain time lag, explained by higher liquidity in the government markets, said Franz Rudolf, head of financials credit research at UniCredit.

Markit iBoxx Covered index spreads reached 104bps on May 7, and recovered to around 94bp after the announcement of the European Central Bank’s rescue package, widening back to 104bp by the end of May. The driver behind this rollercoaster pattern was concern about Greek contagion risk. “The periphery states are still fragile and newsflow from sovereigns will still be a major driver of covered bonds spreads,” the head of credit research said.

Historically the correlation between covered bond and government debt spreads has been pretty weak but has become extremely strong, to the point of being practically merged during the crisis. “It is still very unclear how well the two markets are correlated and what the real absolute value of comparing the two asset classes is,” said Kemmish. The only outstanding public issue in the Greek market by National Bank of Greece trades substantially through the government; Spanish deals trade considerably over governments; and Portuguese deals have switched between trading wider and tighter than their respective sovereign debt through the course of the year, according to the iBoxx Covered Bond index.

The market still believes that the domestic government sector is currently the floor for any covered bond being issued, despite the current spread movements not being correlated with the covered bond product, per se. This is attributable to the fact that underlying domestic sovereign markets were reaching previously unprecedented levels, such as Greece hitting 950bp over mid-swaps and Spain as high as 250bp, said Elling.

Uncertainty also prompted bid/offer spreads to hit their wides. Spain experienced a 100 cent spread equal to 20bp in the five-year maturity, and this level of illiquidity was transferred to other underlying markets, including covered bonds, which also reached extremely wide levels.

Mauricio Noe, head of senior and covered bonds at Deutsche Bank, believes the market needs to let the current extreme volatility subside and allow sovereigns to start to find their own trading range. Over time participants will have to become accustomed to the risk of restructuring in the sovereign sector for some years.

The market will reach a state where it accepts a certain higher level of risk and uncertainty, Noe predicted. “Therefore we need to adjust to this new paradigm, where people are more comfortable with excessive volatility in certain market segments, whilst simultaneously being able to invest in other less volatile assets,” he said.

Although no one is questioning the framework and strong conventions of covered bonds, the market’s view that every asset class is completely correlated to the risk of its respective government has almost become a self-fulfilling prophecy. “When the dust settles, the market will realise that the covered bond mechanism and supervision arguably makes these bonds more secure and less risky than owning government debt,” said Noe.