The NRW joint cities’ bond highlights innovation – and a new level of collaboration – in the German muni market.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.

If the “Ruhr Metropolis” – as tourism officials like to call the EU’s third-largest metropolitan region after London and Paris – is distinctive for anything beyond its history of industrial decline and subsequent reconstruction, it is for sprawl.

But Germany’s only megacity, with a population of 12m in the western state of North Rhine-Westphalia, is in fact polycentric – an urban hydra with many heads. It is the co-operation between at least 20 cities and other districts blending into each other within this vast industrial landscape that makes it something of a social and economic experiment.

And just as the grand burghers of the cities swallowed up by the metropolis have learnt to find innovative solutions to common challenges, they are today charting a new course in public finance through unprecedented levels of co-operation in the capital markets.

A groundbreaking joint issue in February of Germany’s largest municipal bond to-date by six NRW cities highlights that level of co-operation, now driving innovation in the muni market.

“This was something that took a lot of work to bring to the market, but issuing a €400m muni bond in this way really was pioneering for all parties involved – for the cities and for the banks – and we were all extremely pleased with the outcome,” said Robert Mandziara, a director in HSBC’s capital financing division.

“Being able to reach the €400m comfortably and having a subscribed book and high-quality orders from asset managers all over the investor range in Germany was really exhilarating.”

With Deutsche Bank, Helaba and HSBC as leads, the €400m NRW Staedteanleihe No 1 issued by the cities of Dortmund, Essen, Herne, Remscheid, Solingen and Wuppertal – Germany’s largest muni bond to-date – made a successful debut with a February 2018 deal.

Joint municipal bonds have been under discussion for years and this was not the first of its kind – in May 2013, Nuremberg and Wuerzburg issued the first joint bond, raising €100m – but the NRW bond represents new territory because of its size and complexity.

The move towards munis is a reflex by cities seeking greater independence from banks on which they have traditionally relied for loans – in 2013, banks accounted for 99% of outstanding municipal debt. In a sector comment issued in February, Moody’s pointed to an expected tightening of lending from such traditional sources.

Joint bond adventures

Harald Sperlein, lead analyst for Moody’s on the German regional and local government market, said that while bank lending had been and remained popular among cities, they were seeking other funding sources and opportunities to tap other investor groups. A joint bond allowed them to share bank costs related to the actual transaction while providing a “critical mass” in terms of volume to attract the attention in the markets of new investors seeking a certain size of issuance.

“Some larger municipalities and cities are aware of these developments in the banking sector and want to be more proactive and more independent of the banks in the future, so they are exploring new opportunities and hear reports from other market participants and the press that such bonds are not more expensive than a direct bank loan. This is a competitive funding opportunity for the municipalities,” he said.

New Basel III capital adequacy requirements are likely to deepen this trend, making bonds increasingly attractive.

“Let’s be clear: they will always tend to use their classical or traditional ways of funding – their bank contacts,” said Carsten Lohle, director of capital market and treasury solutions at Deutsche Bank.

“Whenever possible they will stick with their banks and that makes a lot of sense: you can’t just suddenly switch to 100% capital market funding. So not every smaller city will have the need to go down this route of joint issuance, but for quite a few of them it can actually be an interesting instrument to access the capital markets.”

While cities have developed extra funding demands due to the financial crisis, fiscal consolidation combined with higher tax revenues is set to improve financial results this year.

“There is no financing problem for municipalities in Germany but given the traditional link between municipalities and banks, which usually grant the loans, and looking at the regulatory environment, which increasingly makes this business a bit less attractive, a bit less lucrative, they have to turn to other sources – but these sources have to be price-competitive,” said HSBC’s Mandziara.

Many cities have experimented with Schuldscheine – negotiable promissory notes popular for their low cost and flexibility but not as liquid as a bond. A joint bond, by contrast, implies volume and liquidity, providing cities with direct access to institutional investors while lowering funding costs. It reflects ongoing innovation in this market that some observers believe may foreshadow the creation of more structured vehicles such as a municipal financing agency in Germany.

Widely considered a pilot project, the NRW joint bond is now likely to be copied by other German cities, but it may not be suitable for everyone.

According to Claudius Siegel, head of structured products and ABS at Helaba bank, one of the three leads on the NRW deal, the joint issue’s pricing was in line with the Schuldscheindarlehen and the normal loan pricing cities can secure, meaning at this stage there is no obvious pricing advantage. The leads opened books at mid-swaps plus 35bp area and final terms saw the bonds being priced in line with that guidance with a 1.125% coupon.

“It’s a really innovative issue and it remains to be seen whether other cities do this. At the moment, I can’t see a really big advantage because it’s a new market – but if the market grows, issuers can approach other investors. In Germany, there were only a few municipal bonds last year and that’s not really a liquid market – so therefore the advantages will become clearer as the market grows,” said Siegel.

The mix of cities in the joint issue combined those already experienced in the capital markets with newcomers, but participants say it clearly helps if they all have something in common.

“It is not physically what they have in common – there should be a ‘common story’ for the cities involved. It makes sense here in the Ruhr: the cities all have the same problems and also the same chances, but it makes no sense to take two or three cities that are not connected in a certain way,” added Siegel.

Some participants in the joint cities deal believe legal questions could complicate efforts by cities in different states to band together, ruling out cross-state deals in the short-term.

The lack of a joint guarantee – it is not politically realistic for one city to be liable for the debt of another – does not appear to be an obstacle to investors, and all eyes are now on where the next joint issue will arise.

Lohle said: “In the mid-term, having been in this market for a couple of years already, I would hope that this is copied by others because I believe it’s a good product and it actually provides access to capital market funding for cities that won’t have that access on an individual basis.”

Yet innovation aside, the muni market remains relatively small, and prior to the NRW deal German cities had issued bonds only three times since Hanover broke the ice in 2009.

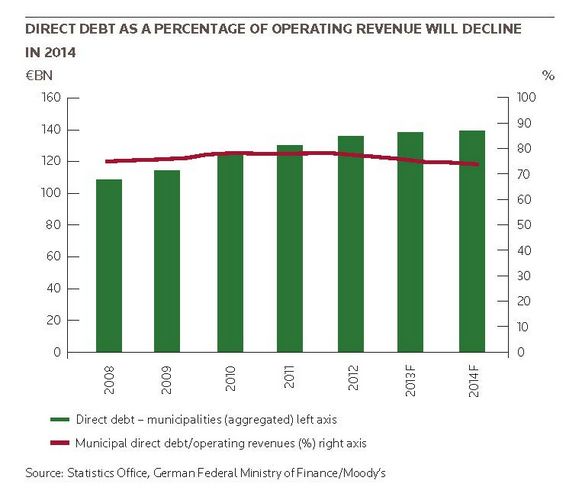

Politics also constrain its eventual size, with limits to public sector debt now enshrined in Germany’s constitutional “debt brake”, although refinancing needs mean city issuance will remain healthy (see table).

“It’s more about diversifying away from existing traditional loans by placing some of the €130bn–€140bn of outstanding debt for German municipalities in the capital markets. As far as the government is concerned, the public sector is not a growing market – there won’t be an avalanche of municipality bonds in Germany,” said Mandziara.

The money raised by the NRW joint cities issue, for example, will primarily allow the cities to refinance existing debt.

Sperlein of Moody’s said: “If the debt brake is complied with by the public sector, then overall we will not see a significant increase of the debt amount. Having said that, there was €135bn at the end of 2013 of outstanding local government debt and this has to be refinanced. Over the medium term this will not be reduced significantly; so the municipalities and cities – of which there are more than 10,000 in Germany – will have short-term and long-term refinancing needs.”

Joint issuance is clearly not for the faint-hearted – the NRW bond took more than six months to set up – but the deal has given the grand burghers a warm feeling about the muni market.

“The market is actually just defining itself at the moment. It’s evolving and I would expect it to expand. You can’t say how fast, because there’s always a trade-off with the Schuldscheindarlehen market, plus questions about how much tax revenue cities will generate. So there are a couple of things that might actually hinder exponential development – but it’s certainly a growing market,” said Lohle at Deutsche.