After unfavourable foreign-exchange moves and plunging offshore liquidity silenced the Dim Sum bond market at the start of 2015, signs of a revival are beginning to build.

It has been a tough start to the year for Dim Sum bonds. Unfavourable forex moves and illiquidity have silenced what had once been an exciting and growing market.

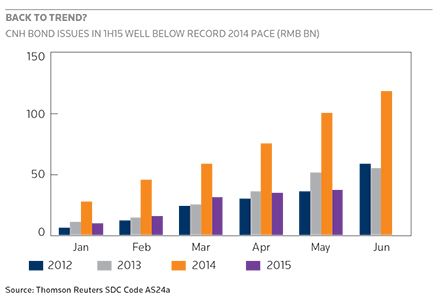

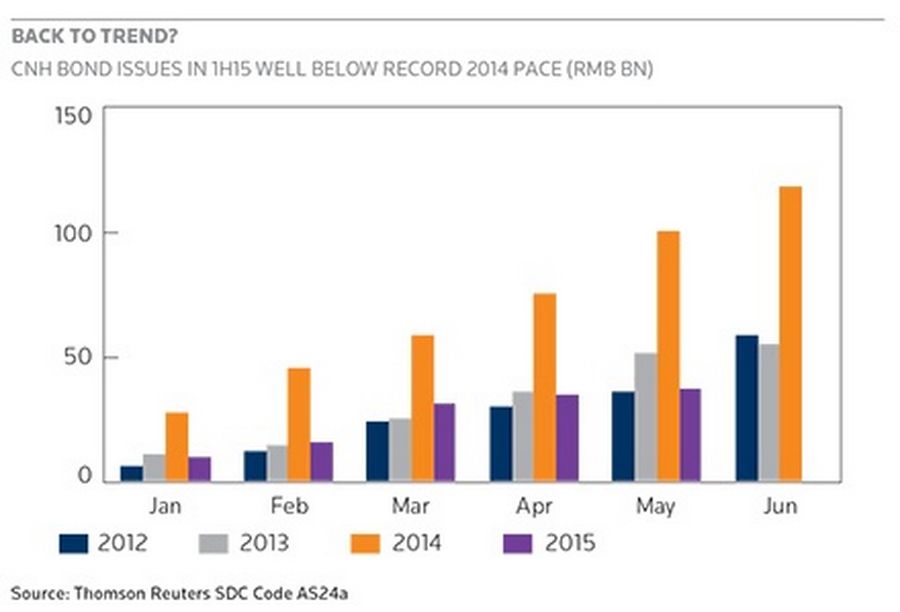

After setting a record in 2014, when Dim Sum issuance hit Rmb324bn (USD52.2bn), the market screeched to a halt in the first quarter of 2015. February was emblematically dire with issuance totalling just Rmb4.3bn, down from Rmb17.8bn in the same month last year, according to data from Thomson Reuters.

Yet, beneath the doom and gloom, Dim Sum bankers are becoming more upbeat about the prospects for the remainder of the year. The liquidity situation for offshore renminbi bonds has been improving steadily, partially due to Chinese interest rate cuts and the Shanghai-Hong Kong Stock Connect trading link, which added to the flow of funds from mainland China into Hong Kong.

With that have come a few small, albeit successful issues. The most recent was an April 29 offering of three-year Dim Sum bonds of Rmb1.3bn from China New Town at 5.5%, which drew orders of Rmb6.6bn, and Deutsche Bank’s May 21 issue of five-year Formosa bonds of Rmb1.65bn at 4.3%.

Back to trend

“The Dim Sum market is definitely coming back,” said Peter Szekely, managing director for debt capital markets, Greater China at Standard Chartered. “It’s been very quiet, but the liquidity situation has improved and more currency is moving offshore. The cost of funding has improved and we expect to see the pipeline build.”

The improvement in offshore liquidity appears to be one of the main factors behind bankers’ optimism. Waning offshore demand pushed Dim Sum yields to record highs this year, just as a series of interest rate cuts pulled mainland benchmarks lower. However, offshore yields have recovered from their March highs, and the spread between onshore and offshore bonds is beginning to stabilise.

“It’s been very quiet, but the liquidity situation has improved and more currency is moving offshore. The cost of funding has improved and we expect to see the pipeline build.”

According to HSBC’s Dim Sum Bond Index, the average yield of offshore renminbi bonds fell 35bp in April, the biggest drop in 20 months.

Bankers are expecting the next wave of Dim Sum issuers to come from mainland China, as companies seek to take advantage of declining yields to diversify their funding sources.

These companies will be mostly state-owned enterprises and banks needing to raise capital. So far this year, a few Chinese banks have issued Tier 2 bonds, but none have opted for Dim Sum. However, a few foreign banks, such as BPCE and ANZ, did so earlier in the year.

“You’ll see that most issuers will likely be Chinese,” said Frank Kwong, head of Asia Pacific bond syndication at BNP Paribas. “They are taking advantage of rates that are coming down. There are still a lot of SOEs that need to come to the market, especially Chinese banks. We haven’t seen benchmark deals from Chinese banks and I’m sure that they are all looking at the market. They need to raise diverse forms of capital and grow their benchmarks. So, we need to monitor that market as there could be opportunities there.”

Foreign issuers that had launched a spate of arbitrage-driven Dim Sum deals in March as a way to take advantage of attractive cross-currency swaps and reduce their US dollar cost of funding are not expected to play as big a part.

Many of these opportunistic issuers – mostly banks – had rushed to the Taiwanese market to issue Formosa bonds in renminbi and swap them back into dollars. The advantageous rate, however, has since dissipated and issuance in Taiwan has slowed considerably.

Deutsche Bank recently issued the largest renminbi-denominated Formosa bond for the year to date, but it was the first of its kind in over a month.

While the offshore liquidity situation has certainly improved, bankers say the currency will remain the key issue. The exchange rate versus the US dollar may have stabilised in recent weeks, but the prospects of further renminbi depreciation have not gone away.

The Dim Sum market should fare better in the second half of the year, but analysts fret that a significant movement in the currency, possibly as a result of poor economic news out of China, could send the market back into the doldrums seen at the start of the year.

Even though a weaker-than-forecast GDP figure could encourage beneficial rate cuts, this will probably not outweigh the damage of a weakening renminbi.

“The key to everything really is the currency,” said a Hong Kong-based syndicate banker. “If it is losing value and the prospects look bad, that will discourage investors, as well as issuers. More interest rate cuts could boost the market, but we have to hope the currency has stabilised. Without that, we’ll struggle.”

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com