Banks’ willingness to underwrite is at a six-year high.

To see the full digital edition of this report, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com

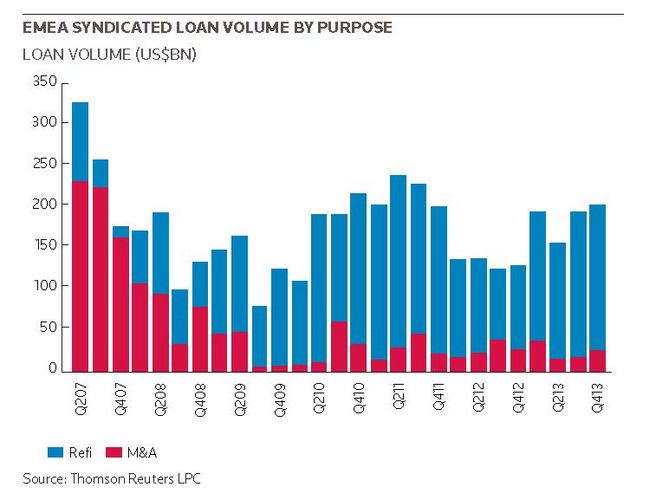

Lending conditions in Europe’s syndicated loan market are ripe for more M&A activity in 2014 amid more positive macro conditions, banks’ renewed enthusiasm to underwrite and a host of cash rich investors eager to put money to work.

Corporates and sponsors are taking advantage of a myriad catalysts for M&A to occur and a pipeline of event-driven transactions is building, after a 2013 dominated by refinancings.

“Loan markets across all sectors remain quite robust as we enter 2014. European borrowers have taken advantage of newly available options to tap alternative markets such as the US loan market and bond markets. Provided we benefit from a degree of economic stability throughout 2014 – including even modest economic recovery – we should see a build-up of the M&A pipeline,” Chris Lovgren, global head of loan syndications at Natixis said.

In high grade, UK engineering firm AMEC’s proposed US$3.2bn cash and share offer for Swiss peer Foster Wheeler is backed with a £1bn plus debt financing. The US$1.595bn cash component of the offer will be funded through existing cash and the new financing.

”Borrowers are looking for low-cost, callable-at-par financing options while investors are looking for attractive relative-value products in floating rate form”

In leveraged, private equity firm Dering Capital is in advanced talks to buy French broadcasting masts operator TDF and has approached banks to provide a debt financing which could total around €2bn to €2.5bn. Other potential deals include the potential sales of German packaging group Mauser by Dubai Holding, German skin patch maker LTS Lohmann and Nordic payment services company Nets Holding.

“M&A is expected to increase in 2014 and around 35%–40% of activity during the first quarter is likely to be event-driven transactions. It was a record year for bond issuance in 2013 but the loan market also surprised many people by achieving the largest volumes since 2007 and we expect a further significant shift towards loan product in 2014,” Mathew Cestar, head of leveraged finance in EMEA at Credit Suisse said.

”Borrowers are looking for low-cost, callable-at-par financing options while investors are looking for attractive relative-value products in floating rate form.”

Desire to underwrite

After a period of balance sheet reduction, banks’ willingness to underwrite is at a six-year high, driven by banks wanting to rebuild portfolios, boost interest income, as well as bolster relationships with key clients amid improving capital positions and reduced funding costs.

Institutional investors are also stepping up efforts to lend, attracted by good yields on senior, floating-rate paper. US and European institutional investors are competing to finance transactions in Europe beyond the traditional leveraged transactions into crossover credits and infrastructure deals.

Competition from different sources of liquidity means 2014 will be a borrowers market if macro conditions remain positive. Loans are expected to get more aggressive in terms of pricing and documents.

“A tightening of monetary policy in the form of tapering, even a modest taper, could result in rising yield requirements. This would make recourse to debt capital markets more expensive and potentially put a break on M&A activity. However, this could be compensated by an overbanked European market suffering from low deal volumes, as bank liquidity is expected to remain substantial throughout 2014,” Lovgren said.

Claire Ruckin; Alasdair Reilly