The series of financial crises that have occurred in recent years have been defining for the covered bonds market. And none more so than the sovereign debt crisis in Europe, which left a vacuum this low-risk asset was left to fill. This is illustrated perfectly by the events in Spain, both a major covered bond market, and a sovereign issuer that has seen turbulent times. Lisa Cooper reports.

To view the digital version of this report, please click here.

Covered bonds have been the darling of the Spanish banking system in recent years, offering cheap finance in a country with a booming housing and mortgage market. All that changed with the onset of the financial crisis across southern Europe. Debt problems in Europe have cast a pall over the Iberian Peninsula and closed the door on capital markets.

In recent weeks there has been evidence of a shift in sentiment, with signs that Spain has managed to disassociate itself from its profligate neighbour Portugal. The resulting normalisation of interest rates has reopened the window for high quality financial issuance.

Spain accounts for almost a third of European outstanding covered bonds. Its large construction and mortgage market and fragmented banking sector combine to offer investors an array of risk profiles and pay off variables.

Pre-crisis, Spanish cajas (savings banks) numbered around 40, although mergers have brought this figure down to 17. Many were traditionally unable to issue senior unsecured notes because of their small size and inadequate credit rating. Instead, they accessed the markets via covered bonds.

Before the start of the subprime crisis, covered bonds yielded barely more than a few basis points over the swap curve. But as government bond spreads widened and bank balance sheets took a battering, yields ballooned – particularly in countries perceived as higher risk, such as Spain and other southern European nations. In early 2011, with the spread for 10-year bonos (Spanish sovereign bonds) around 250bp above German bunds, and yields for covered bonds significantly wider still, the market was firmly shut to all but the strongest Spanish issuers.

“Looking at the asset/liability profile of the margins the banks make on their assets, it became difficult to fund at these high levels on the liability side, especially for longer dated maturities,” said Torsten Elling, co-head of rates syndicate at Barclays Capital.

As Spain’s credit position weakened, investors were disbarred by credit limits from buying Spanish assets in any significant volume. While the strongest names, such as Santander and BBVA, retained market access, weaker cajas and multi-issuer structures were locked out.

“This was not a covered bond move, but a Spain move,” said Jose Sarafana, head of covered bond strategy at SG in Paris. “At the beginning of this year, funds and other investors would no longer buy any type of Spanish risk, be it sovereign or agency or covered bonds.”

Reaping rewards

In recent weeks government and central bank programmes to restructure the banking sector and pension system have begun to pay dividends. The sovereign debt spread started to tighten and investors have felt reassured about the health of the economy, alleviating concerns of a European bailout. By mid-April the spread on Spanish 10-year bonos had fallen to around 190bp, over 60bp tighter than at the start of the year.

Inevitably, a tightening of government bond spreads has caused Spanish covered bond yields to tighten by a similar margin. Cedulas Hipotecarias issued in January priced at a spread of 240-250bp over mid-swaps. By mid-May yields had narrowed to mid-swaps plus 185-195bp as investor confidence returned.

“Another major driver has been continuous strong domestic demand,” said Frank Will, head of covered bond and frequent borrower strategy at RBS. “Iberian investors have bought 44% of the deals.”

The improvement in investor appetite is also having an impact on maturities. Earlier deals were typically issued for only up to two or three years. More recent transactions have included a number of successful five-year deals, such as April’s €1.25bn issue from La Caixa.

What is more, a number of covered bonds have started to trade inside the sovereign bond curve – a phenomenon that is being seen not only in Spain but also in Italy and Portugal. In some cases they are trading tighter for purely technical reasons, thanks to a lack of liquidity in the secondary market. But it has happened with several liquid names too.

“The risk premium that investors expect for covered bonds over government bonds has been diminished and now in some cases is flat for new issues and even negative in outstanding covered bonds,” said Elling. For example Banco Santander, with three-quarters of its income stream originating outside Spain, is rated Triple A – higher than the sovereign. Its covered bonds are currently priced around 160bp over mid-swaps, compared with mid-swaps plus 180bp for Spanish government debt.

The recent spread tightening means market access is no longer reserved exclusively for the strongest Spanish banks. Around ten different issuers have launched covered bonds so far this year, and more cajas are likely to follow. “We have seen nearly €20bn of Spanish covered bond issuance this year, which is more than we had expected back in January for the whole year,” said Sarafana.

Spanish issuance this year is up 70% on the same period in 2010, according to Heiko Langer, senior covered bond analyst at BNP Paribas. However, the large volume of maturing bonds means that net growth is close to zero.

So does all this mean a return to the good old days for Spain’s covered bond issuance? Well, not quite.

“We have seen quite a bit of volatility in sovereign spreads, which means it can be tricky to pick the right window of opportunity to issue covered bonds,” said Langer. Recent negative headlines about Greece, for example, are enough to soften sentiment towards Cedulas. Spreads are likely to remain volatile, driven by developments in the European debt crisis.

In addition, Spain’s construction sector has all but ground to a halt, limiting demand for new mortgages. And, despite the reform effort, the multitude of smaller cajas in particular still need to find ways to resolve their funding needs, with many continuing to hold a high level of problem assets on their balance sheets. Until those issues are resolved, market access will remain tricky for many of the cajas that in the past depended on covered bonds.

Elsewhere

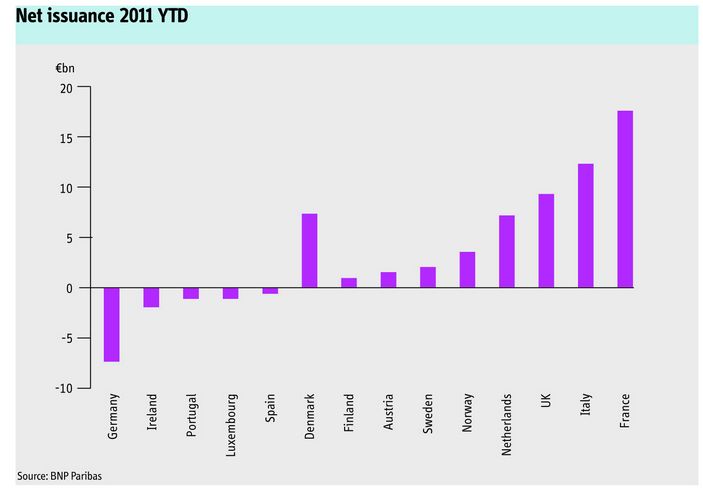

Away from Spain, the covered bond market continues to boom. Issuance has reached record levels this year in Europe, with nearly €120bn sold in the first quarter. France is leading the way with over €25bn of deals so far this year, and Germany added a further €16bn.

The French housing market remains strong and low interest rates continue to fuel demand, so banks still have plenty of assets on their balance sheets and further credit lines available. With Obligations Foncieres offering a cheaper source of funding than asset-backed or mortgage-backed securities, and legal changes also helping French issuers, supply is likely to remain strong.

The Italian covered bond market is also gaining momentum, with around €12bn of new issuance this year, up from just €3bn last year. Recent entrants in the covered bond arena, increasing numbers of Italian banks are now coming to market.

Germany, by contrast, has a negative net supply, with the balance sheets of its major mortgage banks decreasing and much lower refinancing of outstanding debt. This has driven down spreads, making Pfandbriefe expensive compared with other European bonds. Typical yields are around mid-swaps plus 10bp, in comparison with mid-swaps plus 60-80bps for French Obligations Foncieres.

On the demand side, where yields are sufficient investors are keen to snap up the wealth of new issuance. Many new players are coming to the covered bond market for the first time, particularly credit investors, attracted by the high yields currently available, and also by the lack of issuance in the unsecured credit market. Many are making the switch away from asset-backed and mortgage-backed securities and senior unsecured investments in favour of covered bonds.

Lack of liquidity in the secondary market is also pushing investors towards new issues in record numbers. Combined with favourable treatment under Basle III banking rules – covered bonds demand less regulatory capital than other asset classes, bringing many bank treasuries into the market – demand is booming. Things look set to remain that way for the foreseeable future.

But despite strong overall demand, it is still only the stronger names and healthier nations that are able to access funding via covered bonds. In the other European countries struggling in the wake of the debt crisis, such as Portugal, Greece and Ireland, the vast majority of investors continue to stay away. With country limits keeping them at bay they are unlikely to return any time soon.

“Banks [in Ireland] are very dependent on short-term central bank funding, so if they could access longer term funding at a reasonable price, they would be very keen to do so,” said Langer. But government bond issuance must re-emerge before any covered bond activity can return, and there is little sign of this happening at present.

| Spanish issuance 2011 YTD | |||||

|---|---|---|---|---|---|

| Supply date | Coupon (%) | Volume(€bn) | Redemption | Issued at mid-swaps | Current (mid-swaps) |

| 04-Jan-11 | 4.125 | 1.5 | Jan-14 | 225 | 140 |

| 05-Jan-11 | 4.625 | 1 | Jan-16 | 225 | 158 |

| 14-Jan-11 | 4.875 | 0.5 | Jan-13 | 310 | 165 |

| 26-Jan-11 | 4.5 | 0.65 | Feb-13 | 270 | 165 |

| 02-Feb-11 | 4.75 | 2 | Feb-16 | 200 | 161 |

| 03-Feb-11 | 4.5 | 1.2 | Feb-13 | 260 | 176 |

| 10-Feb-11 | 5 | 2 | Feb-16 | 220 | 204 |

| 28-Feb-11 | 4.375 | 2 | Mar-15 | 180 | 140 |

| 08-Mar-11 | 4.75 | 1.25 | Mar-15 | 200 | 187 |

| 09-Mar-11 | 5.5 | 0.5 | Mar-16 | 250 | 244 |

| 21-Mar-11 | 4.25 | 2 | Mar-15 | 155 | 154 |

| 21-Mar-11 | 4.625 | 0.6 | Mar-15 | 190 | 173 |

| 23-Mar-11 | 4.875 | 0.75 | Mar-14 | 240 | 250 |

| 31-Mar-11 | 5.25 | 0.6 | Apr-15 | 235 | 241 |

| 12-Apr-11 | 5.125 | 1.25 | Apr-16 | 195 | 213 |

| Source: Barclays Capital | |||||