To view the digital version, please click here.

IFR: Thanks to all of you for attending IFR’s inaugural Schuldschein roundtable. Given the impressive growth of the corporate Schuldschein segment in particular, and in light of the market’s notable issuer and buyside internationalisation, this discussion is very timely. The first question I’d like to ask is very simple: why are Schuldscheine (SSD) so hot and why now?

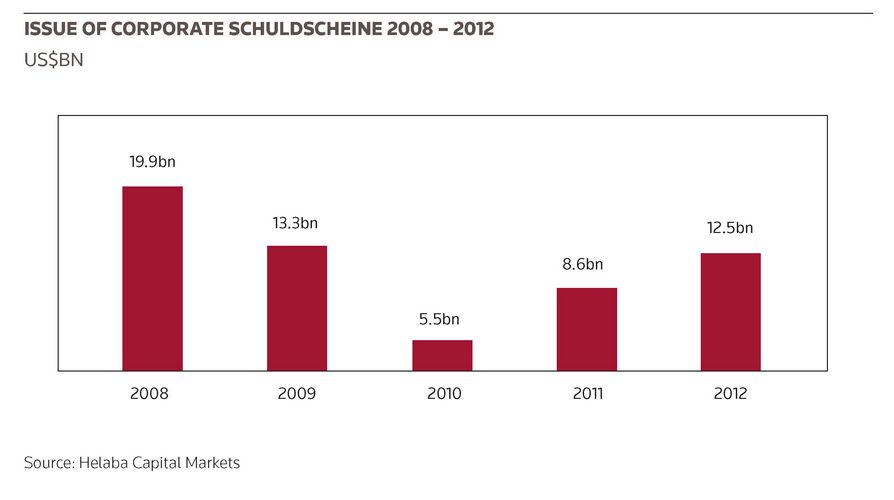

Hassan Farhadi, Helaba: The Schuldschein format is obviously well known in Germany and it’s become more and more popular since the global financial crisis of 2007-08. Our clients always looked at Schuldscheine as an option but we certainly didn’t see such a high level of interest, because they expected to find windows in the bond market to raise funds.

But as the financial crisis deepened, this was no longer possible [as the bond market closed] so more and more mandates came to Schuldsheine.

A key reason for the growth of the market has been the development of the non-German investor base; we’ve found more and more investors worldwide. I was at a conference in Vienna when a senior political figure from Singapore read my name badge label and said: ‘ah, you do all that Schuldscheine stuff’, and they weren’t clients at the time.

We’re also seeing international investors as well as foreign banks coming into the market looking for relationships with Western European corporations and credits. From the Helaba point of view, we are not particularly working internationally but in pushing the product, we found this very, very international investor base from around the world. There’s almost no country we haven’t sold it yet and it’s growing dramatically. Demand is still there and investors are still by-and-large willing to accept the spreads that are in the market now. This definitely supports the market. German saving banks as well as real-money accounts are looking for the kinds of credits that are coming to market in this format.

Claudia Hopstein, HSBC Germany: From an HSBC point of view, the Schuldschein is a very traditional, long established German private placement product. Many of us around the table have been doing this sort of business for years. It’s a base product for corporates that are concerned about disclosure or which have financing requirements that are too small for the public bond markets.

At the same time, as Hassan said, this market has experienced a global push since the global financial crisis and the bank crisis. On the corporate side, it’s really about disintermediation. It’s also about new financing sources and alternative markets. At the same time, we are facing an investor base that is searching for yield and diversification so it’s a perfect fit.

Many European countries provide issuers with a strong and stable background and this is what the investor base is after. And of course there have been interruptions in the bond market while the Schuldschein market has been very stable and less volatile. We’ve all been working to market the product and at the same time expand the investor and issuer base. Many foreign investors like the market because they wouldn’t have access to these sorts of issuers in other segments.

IFR: Ansgar, why does the Schuldschein market stay open when other markets are interrupted? What’s so special about it?

Ansger Wittenbrink, DZ Bank: There is one huge advantage for investors: balance sheet valuation. They can value corporate Schuldscheine at par and don’t have to mark them to market. This is the main advantage for corporate Schuldscheine investors.

IFR: Indeed. So the market is wide open, issuers can get good execution, and volatility is low. But how do you see the market evolving? Will it be the international aspect, Johannes?

Johannes Maerklin, Deutsche Bank: If you talk about the internationalisation of the Schuldschein market, since 2008, we’ve seen heavy supply of non-domestic risk that was supposed to have been distributed into Germany or at least into Europe. But international demand has caught up since this product meets the needs of every investor who can buy unlisted loan-style instruments. There’s not really any restriction on this kind of product; it’s more about getting familiar with the product itself so it’s a matter of investor education.

With regards to investors, most of the buyers are still on the financial institutions side and they’re seeking German mid-cap risk which is well received so creates ongoing demand. At Deutsche Bank, we see ourselves as one of the dominant houses sourcing non domestic risk and educating international borrowers about this product throughout the DB platform.

IFR: There is one specific example I wanted to bring up, which is illustrative of how the market is developing. And that’s the issue for [French borrower] Neopost, which was distributed in Taiwan. To the extent you can talk about this, how did that come about?

Johannes Maerklin, Deutsche Bank: Well, Schuldscheine come with a loan-style wrapper under German law with quite standardised capital market-style documentation and it clearly has advantages for borrowers instead of, let’s say issuing a syndicated loan with a 200-page English law document.

As long as the financial covenants and pari passu language are in line with existing debt, there are no restrictions on selling this product outside Germany. It just happens that not only Taiwanese banks but Asian banks in general are getting familiar with this product; as are European banks and banks globally. Nothing restricts them from buying. And as Claudia said, it’s a good instrument for diversifying risk on the asset side with names that investors are invariably not able to purchase in other formats in other markets.

IFR: Where do Schuldscheine fit into the overall DCM landscape, Maik?

Maik Laske, HSH-Nordbank: Schuldscheine have become a cornerstone in the funding toolkit of corporates. Particularly during volatile times, even the well-known, big traditional DAX names have raised funding in the Schuldschein market. The expectation now is that there will be a much stronger focus on fewer privately-placed transactions in much smaller average sizes than you’ve seen in the previous years. This, of course, allows corporates that have limited funding needs or time to raise funds through the traditional loan market and which wouldn’t have access to DCM given liquidity constraints.

I find it quite interesting that if you sum up the amount of outstanding Schuldscheine in the German market, you get to something like €70bn to €72bn against something like €230bn to €240bn in the corporate bond market. That demonstrates the visibility, the dominance, and the importance of Schuldscheine in the general landscape.

IFR: Is one of the potential drawbacks of Schuldscheine, Christoph, liquidity and tradability? You can only transfer Schuldscheine by assignment like in the loan market whereas corporate DCM operates in bigger size and is much more liquid. Is the fact that Schuldscheine are buy-and-hold instruments a real drawback?

Chrhistoph Zender, LBBW: Well Schuldscheine are buy-and-hold investments. I would say roughly 95% is buy-and-hold. You only see 5% offered in the secondary market. But from the point of view of borrowers, they also like to have private placements which are placed firm with investors. They are not really keen on improving the secondary market.

IFR: But is that changing, Richard in light of the globalisation on the buyside and as we see more institutional investors coming into the Schuldschein market?

Richard Waddington, Commerzbank: If you look at the investors that are buying SSD, which is principally banks and some institutions because it’s a non mark-to-market product, the fundamental demand is principally buy-and-hold. But we are seeing some paper in the secondary market and I think over time we will see this increasing. But I don’t think it will grow to the same extent that you see in the secondary loan market, where there is a reasonable level of liquidity.

If you look at the [liquidity] extremes, you have bonds; lower down the scale you have loans and beyond that you have Schuldscheine. We’ve worked to create more liquidity because it is a relatively easy product to trade [notwithstanding] consent issues, but ultimately one of the things that’s clearly a negative is the relatively small issue sizes for SSD.

Over time, we will see more liquidity come into the market, but secondary liquidity is never going to be a mainstay of this product. If you buy this asset, you have to accept that it is a relatively sticky instrument.

IFR: Investors typically demand some kind of concession or premium to hold an illiquid position, Christian. But I understand that the pricing on Schuldscheine is becoming very aggressive in some cases, which seems in some respects to be counterintuitive. How do you square the lack of liquidity with ever decreasing pricing?

Christian Porath, BNP Paribas: Let’s start first with why investors are buying. In general, they are looking for long duration but can’t find it in the market. We don’t normally see benchmarks going out beyond 10 years but we’ve seen Schuldscheine of 20 and 30 years and I’ve heard of banks that have gone even longer.

Second: they have flexibility around size and around fixed or floating-rate so investors are paying for the flexibility of Schuldscheine and for the long duration. Beyond that, what we’ve seen over the last few years is a big shift to credit. In the past, 90% of the Schuldscheine market was banks or Laender.

Now most of us are seeing corporate Schuldscheine becoming a much bigger segment. Why? Because the investor base is moving to credit and they want to do it with instruments they are familiar with, especially German insurance companies and pension funds, which want to take advantage both of the non mark-to-market nature of Schuldscheine and the easier documentation.

The other very interesting point is not just the shift to credit but the internationalisation of the market. In the past, German investors only bought German paper; they had some limited investments in foreign banks so at the moment they’re really looking for a diversification of the issuer base and they are going much more international. For instance, corporates in, say, Italy or Spain can raise funding in Schuldscheine even when the market is closed for them in their home countries and at low rates.

The low rate environment helps pricing. People in this market don’t look at spreads; the real-money accounts we’re speaking to look at the absolute number on the Schuldschein.

Richard Waddington, Commerzbank: When you talk about pricing being more aggressive or more competitive, if you compare it to the loan market, Schuldscheine pricing needs to be viewed as having a non-relationship premium relative to loan market pricing, which is very much driven by relationship. Yes it is becoming a more aggressive market and more players are active in it but it’s still perceived by the buyers as having a premium over the loan market in general because it’s fundamentally a non-relationship product.

Oliver Rupprecht, NordLB: At NordLB, the main investors are Sparkassen, which are a very big anchor for us; some 30%-40% of Schuldscheine are going to these clients. Of course, pricing is something they look at but the main issue is they need assets from different corporates to diversify their portfolios. That’s the main reason they’re picking up these assets. We are seeing a lot of deals getting more and more aggressively priced, but that isn’t the main topic here; it’s more about diversification.

Maik Laske, HSH-Nordbank: What we’re experiencing with investors now is they have a much more precise view of the names they’d like to invest in. In the past, this was very much an issuer-driven market but now we’re experiencing more and more reverse enquiry particularly from insurance investors looking to hit a 4% threshold. They don’t always achieve it but they have a specific view of which names they would like to invest in.

Oliver Rupprecht, NordLB: It’s worth pointing out that the companies that are going to issue, especially Mittelstand companies, don’t have the capacity to issue bonds in big size. Typical investors, especially from the Sparkassen sector and others, are looking at these companies but don’t have a relationship with them so the first step to getting a relationship is through buying Schuldscheine.

Johannes Maerklin, Deutsche Bank: Another very important thing is that mid-cap companies in Germany, Europe or elsewhere, if they were to issue listed instruments it would trigger IFRS accounting. So that’s why Schuldscheine are a preferable instrument. That’s a crucial point. Most German companies are not prepared to issue bonds for transparency or publicity purposes.

Hans Niethammer, Unicredit: But I think quite interestingly, when talking about Schuldscheine pricing and looking at the issues over the last couple of years – even those with tenors of three years and which have solid shadow ratings – very few priced below 100bp. If you compare that to, for instance, pricing levels for solid externally-rated corporates that are currently able to raise funds, especially out of Germany at well below 100bp, that should indicate that there is some sort of floor in Schuldscheine pricing, which is somewhere around the 100bp level even if we are talking about short-dated paper.

IFR: One thing that strikes me is if you look at our group today, it’s predominantly a DCM group except for our friends at Commerzbank. I’m just curious to know why Commerzbank still runs Schuldscheine off its loan desk when all your friendly competitors here are DCM guys.

Raoul Hessling, Commerzbank: I think the view for most of the people here is that this is a suitable product for corporates that are not rated. At the end of the day, when you look at the investor base for unrated paper, most of it goes to banks so I think it’s more appropriate to run the product off the loan side because we are able to speak the same language as the investors.

They want to understand the business model, they want to understand financial ratios and they need people who can explain that. On the bond side, there’s more of a tendency towards saying: ‘this is the rating, this is the price, will you buy it or not?’ so I think he right approach is on the loan side.

Richard Waddington, Commerzbank: It’s an interesting, point. Ultimately, Schuldscheine is a hybrid product. If you look at the group here today, it’s principally on the bond side but you do get organisations such as ourselves where the product sits on the loan side. Schuldscheine straddles both loans and bonds. If you look at the investor base, you have institutions and you also have banks that invest there so it’s not a product that automatically fits neatly on either side.

Ansgar Wittenbrink, DZ Bank: For corporate Schuldscheine, the documentation is very streamlined but it’s strongly linked to the syndicated loan market.

Hans Niethammer, Unicredit: It’s also a question of relevant funding alternatives. From a purely technical point of view, Schuldscheine are close to corporate loans. Many of the issuers we’ve seen coming to the market most recently, as was just mentioned, would just not be able to issue bonds so I think you know from that perspective, it’s closer to the loan product. At the same time, for many issuers a Schuldschein is the first step into the debt capital market, bringing it closer to the bond universe.

Maik Laske, HSH-Nordbank: From an issuer perspective, they really don’t care whether it’s handled out of a loan team or out of a bond team. They just have issues that need to be resolved and if it’s resolved by loans, Schuldscheine or bonds they don’t care as long as it’s sorted. Loan originators, bond originators and Schuldscheine originators are close friends and work as a team.

Chrhistoph Zender, LBBW: From my point of view, I must say it suits the DCM business very well. For example, if I look into a transaction of, say, €400m, you have around 100-150 single investors in the book. This means, in terms of distribution, it’s more comparable to the bond market.

Raoul Hessling, Commerzbank: I think you have to take elements of both markets at the same time. For example, if you look at placement procedure, it’s really bond style in the way that the bookbuilding, the spread ranges and all those kind of things work. But then when you look at it from the timing perspective, it’s more like a loan because you give investors four weeks to decide, you have the credit committees set up and they have to get lines from different committees so this is where it’s more like a loan. So yes it’s somewhere between and every house has to decide how it wants to approach it.

IFR: One key point that’s related to developments in Schuldscheine is how the syndicated loan market develops in Germany. In 2012, you had the rare situation where there was bigger corporate issuance in DCM than in syndicated loans. Loan bankers always tell me that refinancing for 2013 has been completed, as well as a lot of the refis coming up in 2014. In addition, there’s no real event-driven activity pipeline so it’s going to be episodic. I’m curious to get a take on loan market activity in 2013. It’s a little off topic but I think it’s related.

Raoul Hessling, Commerzbank: Looking at the Schuldscheine and syndicated loan markets and how they work together in Germany, I think what we’re going to see is that corporates are going to use the syndicated loan more for undrawn revolvers that are very thinly priced in order to pull in relationship banks who want to do to cross-sell. And they’re willing to accept this pretty low margin business.

On the other side, German corporates have discovered Schuldscheine as their product of choice, and will do funded transactions for which they’re willing to offer a decent market price. Looking back five or six years where we had revolvers and term loan tranches in the syndicated loan market, I think we’re going to see more and more loan/Schuldscheine combinations.

Schuldscheine Roundtable 2013: Part 2