To view the digital version, please click here.

IFR: How big can the Schuldschein market realistically become?

Paul Kuhn, BayernLB: Well, in 2008, it was over €20bn. At that time, the capital markets were illiquid for several weeks but we had issuers coming along and creating demand for those kinds of volumes and it was very easy to bring issuers and investors together. So it was possible at that time to place more than €20bn and we saw order books of €1.6bn, €1.7bn for single deals. That shows you the possibilities of the Schuldschein market, which pretty much approached debt capital market volumes for each and every transaction.

IFR: So what are the expectations for the market this year across corporate, public-sector and financial institutions?

Paul Kuhn, BayernLB: I think that we will see a little bit less than last year, because 2012 was such a successful year relative to the last 10 years. Other than 2008, it was the most active year. We saw several transactions that were pre-funding 2013 needs. The first six to eight weeks of the year were less active than I had possibly foreseen. So there might be a little bit less volume from my perspective.

Christian Porath, BNP Paribas: From the client perspective, I think the institutional side will be bigger…

Hassan Farhadi, Helaba: Assuming the economic world remains relatively stable, and bearing in mind the fact that corporate are currently well funded, we may see a shift back towards municipalities, utilities and SMEs. We will most likely see more issuers from these segments with smaller notional amounts – between €20 and €50m.

If there is one sector that could move the Schuldscheine market, it’s the financial sector.

We’re seeing demand from investors who want non-mark-to-market assets in their inventory and we see more and more foreign banks coming to the sector, which could shift the market dramatically in terms of volume.

But in general I think we’re in a well-funded situation in the corporate world and we have very low yields. Because of this, if we talk about the German borrowers, it will make it untenable for many investors to participate. Our investor enquiry is huge but the spread environment won’t necessarily fit.

Johannes Maerklin, Deutsche Bank: You have to distinguish between domestic and non-domestic risk. Non-domestic risk could more than compensate for the reduction of domestic issuance. From what we’re seeing, interest from non-domestic borrowers is huge so we have a very optimistic scenario for this market.

Christian Porath, BNP Paribas: It’s also important to bear in mind the originate-to-distribute model of the banks. With Schuldscheine you don’t need to do the swap; it’s really just buying and selling and this fits the new world for the banks perfectly. This is a business we will continue to push more than doing [bond] transactions where you need to do the swap, you need to charge CVA, it’s very competitive and it takes a lot of credit lines etc etc.

Claudia Hopstein, HSBC Germany: From our point of view, looking in particular on the corporate side, we think that there will be a slight increase versus 2012 so we would estimate volumes to range between €13bn and €15bn equivalent because of the increasing proportion of foreign currency-denominated issuance and refinancing. The huge 2008 issuance volume, which came with a lot of five-year paper needs to be refinanced around now.

We also expect a large number of first-time issuers from the German Mittelstand, partly due to disintermediation. At the same time, we expect to see a broader international issuer base from Europe. The acceptance of this German market is increasing every day. Take French corporates. They have good experiences in the Schuldschein market and this will attract new French issuers as well as repeat issuers. That’s also true for other European countries.

Maik Laske, HSH-Nordbank: But we’ll also see more and more German mid-cap names that want to raise €20m to €40m and which are closely evaluating and assessing different alternatives. People might laugh but there are also German Mittelstand bond segments on the Stuttgart and Dusseldorf stock exchanges and there are potential candidates for Schuldscheine that will benefit from the difficulties those initiatives are experiencing.

Oliver Rupprecht, NordLB: We have several sectors that are growing, including, as mentioned earlier, utilities. Utility companies have quite big debt requirements. Because of their background – they’re owned by the states or the cities – they have strong ratings so we think we’ll see strong demand there as well.

Christian Porath, BNP Paribas: In certain markets like France, they are trying to replicate Schuldscheine, so that might take away some of the issuers that would otherwise come to Germany.

Richard Waddington, Commerzbank: That’s an interesting point. But if you looked at any PP-type product on a pan-European basis, Schuldscheine seem to be making more headway than any other product in terms of expanding beyond its traditional market into other territories.

IFR: There is a debate about whether we’re ever going to get a pan-European private placement market. Does anyone believe that medium term, we’re going to get some supportive regulatory action that will support the creation of a pan-European PP market? Could Schuldscheine fit into that or will they remain fiercely independent?

Raoul Hessling, Commerzbank: I think the Schuldschein fits very nicely into that, because until now we’ve only seen national solutions to private placements. We’ve seen Austrian retail bonds, we’ve seen French PP and there are Scandinavian and Benelux variations to that. Schuldscheine are, to my knowledge, the only private placement product that really fits into the trend to internationalisation, so we have Italian, French or UK borrowers using it and, international investors buying it. So it’s completely international right now: we have French corporates using the Schuldschein market to raise US dollars in Asia.

IFR: So is the Schuldschein market the model for the European private placement market? Do we start to expand the way that Schuldscheine work to other countries?

Oliver Rupprecht, NordLB: Well, we don’t have a specific Schuldschein law, so it’s different to Pfandbriefe, where there is a specific law. With Schuldscheine, it’s about trust in the documentation, the way that the banks are dealing with the product and trust in the borrower.

IFR: I wanted to touch on prospects for the structured Schuldschein market. Investors seeking very specifically tailor-made risk profiles or risk pay offs have found solutions in the Schuldschein market in the past. Do we expect to see the structured SSD market evolving in 2013 and beyond?

Paul Kuhn, BayernLB: I think as long as the pipeline of regular Schuldscheine exists and there’s a steady flow of new deals, there will be limited interest by investors for structured products.

Hassan Farhadi, Helaba: Most of us did billions worth of structured Schuldscheine based on government risk in the 1990s, but in those days there was no credit risk at all in government exposure so it was quite easy for real-money accounts to seek a balance sheet investment reflecting their interest-rate view. But now that we have seen governments endure major problems, and many investors like to differentiate between a credit and an interest-rate view. I think this will limit appetite for these kinds of structures.

But we may see asset-based structures using Schuldschein principles, for example, on real estate. We’re currently investigating this because we’ve seen investor demand for it so it might be an option but it’s not going to move the Schuldschein market in general. Schuldschein should remain a lean and mean instrument for senior unsecured debt and should not be mixed up with complex loan structures.

IFR: So is there general acceptance that the structured market is not going to work?

Johannes Maerklin, Deutsche Bank: It’s not about Schuldscheine; this is about investor demand for structured rate risk. It’s not linked to the Schuldschein product itself; it’s about the payoff.

Christian Porath, BNP Paribas: And for the banks, the structured rates business has shrunk dramatically partly because of Basel III issues, so there’s no liquidity.

Raoul Hessling, Commerzbank: What’s nice about Schuldscheine is the slim documentation. When you start to look at structured issuance, possibly involving inter-creditor agreements or those kinds of things, it’s counter-productive. There is room for structured Schuldscheine in certain niches where you think you can get new investors, but it’s not going to change the market.

Christian Porath, BNP Paribas: I think in multi-tranche offerings, we’ll maybe see things like callables.

IFR: So moving back to the corporate market, what might we expect to see in the coming year and beyond? Might we see bigger issue sizes, say above €500m?

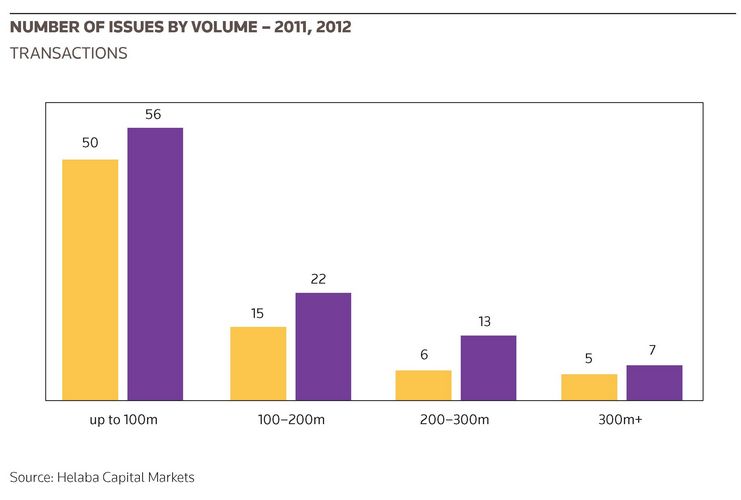

Raoul Hessling, Commerzbank: I don’t think so because if you want to go into the billion euro area, you will probably look at doing a benchmark bond. The sweet spot for Schuldscheine is somewhere around €200m, where it fits nicely into the financing toolbox. If you want to go benchmark size, you probably want a listed instrument. So I don’t think this is going to move much; it’s more about being able to get more issuers into the market. The limiting factor will not be investors; it’s going to be the number of issuers.

Richard Waddington, Commerzbank: Yes, fundamentally the limiting issue is issuer size because as Raoul says, once you step-up beyond a certain size you look to other markets and potentially getting more price tension in those markets.

Chrhistoph Zender, LBBW: Maik already mentioned it but I think we’ll see lots of smaller transactions here that range between €20m and €50m. And here we’re not talking about institutional investors or international investors; the investors are German savings banks and co-operative banks. Last year we had a perfect market with roughly 100 transactions and total volume of €12bn. The big challenge for this year will be to top that; it’ll be quite challenging.

Claudia Hopstein, HSBC Germany: We see new issuers, we see more currencies and I think we will see more tranches. I think many new names will be attracted simply by the fact there are more currencies available, and it’s not just the US dollar; it’s also Swiss franc and sterling. If companies are operating on a more international basis, they will be attracted to the idea of going out with more tranches and then it’s a question of tailoring the deal to the issuers and their financing requirements, regardless of what sort of company it is.

But I fully agree with Christoph: many new and more German Mittelstand companies will look at that market, and deal sizes will typically go down. At the same time we might have some bigger international corporates looking at Schuldscheine and then we’ll have some big issue sizes. The flexibility of this market has remained part of its beauty.

Raoul Hessling, Commerzbank: We shouldn’t forget that we had a huge increase from 2011 to 2012, of around 35%, which is a lot. I agree with Christoph and Claudia, that the number of deals will increase but volume will be stable in 2013.

Johannes Maerklin, Deutsche Bank: The question is: which deals are public knowledge?

Christian Porath, BNP Paribas: Indeed: we have a lot of issuers saying ‘no disclosure’.

Claudia Hopstein, HSBC Germany: And that’s written into the mandate letter. That’s one of the other very important features of that market, because the privacy can really be maintained. You can do broadly syndicated deals, you can do your press announcement, whatever you want and you can tell the world what you have done. But at the same time you can keep it really quiet and nobody will hear about it.

IFR: I had a macro question around the sensitivity of Schuldscheine to the rate structure. I’m thinking more about the US where there’s a lot of talk about the Fed taking its foot off the stimulus pedal and a normalisation of rates.

Paul Kuhn, BayernLB: I don’t think Schuldscheine investors are as sensitive as other investor bases. As has been indicated several times by several people already, there is a tremendous amount of liquidity available and it’s not coming from the market per se, but the investors themselves i.e. saving banks. They’re investing people’s savings and looking for security so it’s not that those investors are refinancing themselves in the market and would be affected by changes in market conditions.

Raoul Hessling, Commerzbank: I’m thinking of two drivers in this context. If interest rates start to rise, bond investors will maybe become more reluctant to buy longer-dated paper because they won’t want to recognise the mark-the-market value. Now that might be a bit tricky on the bond side but it might support the Schuldschein market where there’s no mark-to-market.

The other thing is if the economic environment gets worse it’s also a really strong driver for Schuldscheine. That’s been my experience since 2008 when it’s driven companies to build up liquidity positions and Schuldschein works perfectly in that context.

Hans Niethammer, Unicredit: No-one has a crystal ball but I really think that one of the key drivers for the Schuldschein market performing so well, especially in 2012, was the German economy was regarded as the safe haven within the European economy, and I think that, especially for the German Mittelstand segment, clearly drove the market and especially investor demand from outside Germany.

Clearly, a big issue is how the crisis develops and how the markets react in the coming months. I think if the market stays volatile, which will specifically impact the publicly-traded bond market, the Schuldschein market will profit. And it will especially draw the attention of potential issuers that could also tap the unrated or non-frequent bond markets. Last year we had sound issuance volumes in the bond market but that was mainly driven by frequent issuers which have been able to tap windows as they opened up.

From the perspective of a potential issuer that had to tap the non-frequent market with all the preparations beforehand, it was much more difficult to figure out which issuance window to attack. As the Schuldschein market is a very conservative, very stable market, that was clearly driving the market to a certain extent, and therefore I’m curious to see how volatility in the bond market develops.

Christian Porath, BNP Paribas: At my former bank, I had a discussion with our treasury department and they were unwilling to sell Schuldscheine at normal prices because they saw maybe only one investor buying and their problem was if you have only one investor, you have a risk that he wants to redeem his position so we had long discussions, and I explained to them that most investors are buy-and-hold.

A lot of bank treasuries in the past felt that Schuldscheine didn’t offer stable funding. That has changed now to the extent that when they look to do benchmarks, they will also look to do Schuldscheine as well.

IFR: We’re just about out of time, so let’s wrap up with some closing remarks.

Ansgar Wittenbrink, DZ Bank: I like the Schuldschein market, because it always offers us new focuses for issuers and investors.

Claudia Hopstein, HSBC Germany: There are clear trends but the beauty of this market will remain in place.

Chrhistoph Zender, LBBW: I’ve been working in the German Schuldschein market for quite a long time. For me, it would have been unthinkable in the past to be taking part in a roundtable discussing German Schuldscheine so it’s a great honour for this very simple product.

Oliver Rupprecht, NordLB: I think the number of banks around this table shows that this topic is growing and getting better and bigger. This market is going to grow.

Hans Niethammer, Unicredit: The Schuldschein market is clearly there to stay and I think that it will be and should be regarded as a very attractive source of funding especially for German midcap companies.

Raoul Hessling, Commerzbank: I am very curious about the competition next year, because with all these sessions the awareness in the international community increases so you’re going to see not only new issuers but also new competitors.

Christian Porath, BNP Paribas: We are a truly non German house, unlike HSBC and Unicredit, which have a very strong German base so we are truly the new kid on the block. Other banks are also looking at the German markets and we truly believe it’s a strong market that fits perfectly into international DCM expansion.

Paul Kuhn, BayernLB: I am hoping for a good environment, prosperity and positive developments in the economy, because that would mean that companies would need to invest in factories and would need funds which would help the Schuldschein market.

Richard Waddington, Commerzbank: We’re going through an interesting phase in terms of the development of the Schuldschein market. We have seen the international Schuldschein market grow over the past couple of years and I believe this product will continue to internationalise. However, the international Schuldschein market is quite a different market to the domestic Schuldschein market; there is some investor crossover but fundamentally it is a different market. I think the other interesting aspect is the institutional demand for the product which is starting to develop. We think that this will be a growth area over the next 12-24 months.

Maik Laske, HSH-Nordbank: I am very much looking forward to at least a stable or slightly increasing market, but we’re looking forward to the number of issues and issuers increasing.

Johannes Maerklin, Deutsche Bank: Deutsche Bank’s view is that this market is nowhere near its limits, that there is still a lot of potential for all of us ahead, it’s a sustainable market and a sustainable product that offers great optionality for a lot of borrowers and investors. We haven’t ticked every box in terms of potential risks that we can remedy using this format and in terms of potential investors.

Hassan Farhadi, Helaba: We are quite positive on this market as well but we don’t expect it to grow dramatically this year but we are very positive that it will be more and more of a well-known instrument with more borrowers, especially from abroad.

IFR: Ladies and Gentlemen: thank you for your comments.

Schuldscheine Roundtable 2013: Participants