The extension of municipal bonds throughout China represents an effort to bring desperately needed transparency to opaque local government financing and avert a debt crisis.

If the Chinese proverb “rich is the man with no debts” is to be believed, then local authorities throughout the country have been growing steadily poorer from decades of fundraising through opaque local government financing vehicles (LGFVs).

Concerns about spiralling debt among local and regional governments (LRGs) have mounted as the economy has slowed, sparking a revolution in transparency through regulatory changes aimed at encouraging a transition away from LGFVs and into municipal bonds.

LRG debt is viewed by many analysts as a serious threat to the economy and recent interest-rate cuts by the People’s Bank of China have failed to lower borrowing costs for many lower-rated issuers, compounding concerns about default.

For some time, experts have argued that the only long-term solution to local debt is the creation of an active municipal bond market, something that since 2012 the central bank has been exploring.

“Continuous borrowing by local governments to fund infrastructure and other spending has led to the build-up of a substantial debt pile. This is estimated to be around US$2.5trn–$3trn. This municipal bond programme was designed as an attempt to make provincial governments more responsible for their borrowing. Whether it has succeeded in doing that, however, is another matter,” said Danae Kyriakopoulou, senior economist at the Centre for Economics and Business Research.

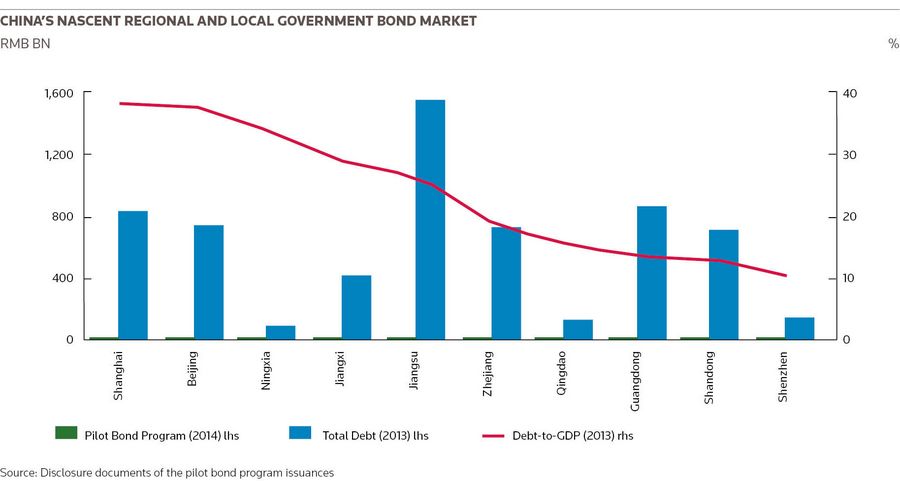

Despite broad recognition that LRG debt in China is a problem, up-to-date figures about it are impossible to come by. The last Chinese national audit report in June 2013 put the combined debt of local governments at Rmb17.9trn (US$2.86trn), up 67% from the last audit in 2011. A year ago, Reuters cited estimates that local governments might owe up to US$4trn, 42% of China’s GDP, and an updated audit is expected this summer.

Need for transparency

Andre de Silva, head of global EM rates research at HSBC, said: “One of investors’ major concerns is that the structure of local government debt is so opaque. With the emergence of over 8,000 LGFVs, it has been difficult to grasp the magnitude and nature of the debt. Even the central government is finding it a challenge, as the National Audit Office discovered when it went through the books. Creating greater transparency is crucial.”

As provincial governments start to suffer from a slowdown in growth and a sluggish property market, China’s leaders have grown nervous. In April, the Shenzhen-based Kaisa Group became the first Chinese property developer to default on its overseas debt, put at US$2.5bn.

Nahed Ennasr, chief strategist at Fathom Consulting, said: “The problem posed by municipal debt is a symptom of a slowing economy and overcapacity. Our view is that China is experiencing a hard landing. They have just cut their benchmark rate and we have seen the first international default on the debt market, Kaisa – and we will see much more coming.”

The LRG debt has grown despite restrictions banning local borrowing 20 years ago, largely because central government under-funded ambitious development plans, forcing provinces to push ahead with costly infrastructure projects bankrolled by risky, unregulated borrowing off-balance sheets through LGFVs using shadow-banking products and short-term loans.

Crackdown

Regulators launched a crackdown last year and in a series of steps empowered the 32 provincial authorities and some city-level governments to issue muni bonds. Investors have responded enthusiastically, with the Standard & Poor’s China provincial bond index gaining almost 10% in the past 12 months.

In March this year, the government announced that it would allow LRGs to convert as much as Rmb1trn (US$160bn) of existing high-yielding debt into municipal bonds in a bid to cut debt-servicing costs, potentially reducing interest payments by as much as Rmb50bn a year.

However, in April it was revealed that several LRGs have had to postpone bond auctions as banks – reluctant to be saddled with poor assets at low rates of return – balked at the low yields on offer. The response by China’s government was to do what it does best: flex its muscle. It has forced banks to swap muni bonds for debt, with the concession that they can count the new munis as guaranteed collateral with the central bank.

Kyriakopoulou of the CEBR said that elsewhere swaps of this kind would be akin to a default. “If you had seen that in a country like Greece, for example, it would immediately be considered a default but in the case of China it is not. What is happening is that there is a high level of debt and local governments are struggling to find the funds to repay it,” he said.

“Instead of letting them default, the central government is imposing a debt swap on the banks, whereby the banks unilaterally swap their short-term high-interest debt with a low-interest higher maturity debt. The People’s Bank of China has promised to then let the banks use these bonds as collateral for further lending. It is a form of easing policy.

“It’s worrying, but we should keep in mind that China is an economy in transition. These targeted measures of easing policy can be more effective than lowering interest rates and letting the market allocate credit to the most efficient uses given the nature of China’s economy,” he said.

“Currently the Chinese economy is pretty much driven by fixed-asset investment. Demand might still be pretty high but having said that the central authority is trying to rebalance the economy from fixed-asset investment or infrastructure-driven to more consumption driven. So let’s see how that works – it is going to take some time”

Terry Gao, director of international public finance at Fitch, points out that although the yields on munis are low, the government has offered clear benefits for the banks.

“The yield is just a bit higher than the treasury bond, but the central government also set some rules that the banks can benefit from: for example, the risk weight factor for all these bonds issued under the swap programme is only 20% and this could benefit the banks’ capital adequacy. So although people know that the yield may not be high, the government has made interventions that can help buyers.”

Swapping appears to have broken the logjam and in mid-May, after a one-month delay, the heavily indebted Jiangsu Province was able to sell the first batch of muni bonds among LRGs this year, auctioning issues totalling Rmb52.2bn at a price not much higher than the yields China pays on its sovereign bonds.

Despite the hiccups, analysts broadly welcome the muni bond programme, pointing to a range of benefits for Chinese financial markets and the country’s fiscal health.

Changing model

Gao at Fitch sees it as part of a broader ambition to change the economic model, saying: “Currently the Chinese economy is pretty much driven by fixed-asset investment. Demand might still be pretty high but having said that the central authority is trying to rebalance the economy from fixed-asset investment or infrastructure-driven to more consumption driven. So let’s see how that works – it is going to take some time.”

He believes muni bonds will give China’s subnationals more flexibility to meet their funding needs and help them achieve a better debt maturity profile; will encourage them to shift away from off-budget shadow financing; and will also allow for more accurate pricing of risk.

The measures amount to a revolution in transparency in local government finance, many details of which remain hidden from public scrutiny. Guangdong, for example, qualified for its bond auction by becoming one of the first local governments to publicise its debt load (Rmb62bn at the end of 2013).

Yet there remain doubts about filling the gap left by LGFVs with a huge expansion of the municipal bond market. There are concerns in particular about rating arrangements in China, with some analysts referring to compliant domestic agencies and possible collaboration between them, issuers and the state-owned banks.

Fitch, Moody’s and Standard & Poor’s only rate offshore-issued Chinese bonds, and opinions about domestic risk vary considerably. In November 2014, for example, S&P warned that half of China’s provinces might warrant junk-level credit ratings.

In March 2015, Moody’s analysts reported that if they were to apply global methodology to upper-tier LRGs, their ratings would be “no more than two notches below that of the sovereign government”.

Moral hazard

“China is trying to attract more international investors in the local market, the onshore market, but to do that they need international ratings agencies such as S&P, Fitch and Moody’s to rate their bonds – corporate bonds, for example – which is not happening at the moment. So LRG debt can be risky. It can be rated Triple A, but goodness knows what the real rating is,” said Ennasr at Fathom Consulting.

Above all, there is uncertainty about what might happen in the case of a default. Analysts say yields that have been lower for local issues than for central government bonds imply that investors believe a central government bailout is guaranteed.

In August 2014, S&P said the expectation of some investors that the central government would support the bonds derives from the country’s unitary political system and the strong controls that it exerts over LRG bond issuances – but pointed out that the central government has grown increasingly wary of moral hazard – which may mean that it will allow LRGs to default.

De Silva at HSBC said: “There have been no actual defaults yet on LGFV bonds and loans in China. However, defaults should occur so that investors can price in adequate default risk premium. Borrowers will then be differentiated and this can help deter unnecessary fundraising.”

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com