The rise and rise of the passive fund is yet another result of the low interest rate environment. And a worrying one.

It’s commonly acknowledged that 2016 has been a difficult year both for traders and investors. Volatility, the life-blood of performance, has been sporadic and very much a case of feast or famine. The current year always feels much tougher than the last so no doubt we will find ourselves looking back at 2016 and agreeing that it wasn’t all that bad after all.

Volatility is a little bit like a car with two steering wheels. The first one comes from the very nature of the fear and greed factors, but the second is the matter of liquidity which is, in itself, a function of the depth of markets. Many of the questions surrounding the “flash crash” in sterling in early October were framed in terms of what happens when traders hit a thin market hard.

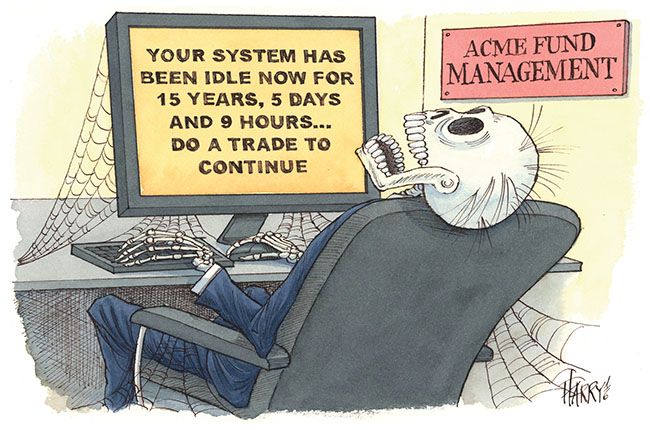

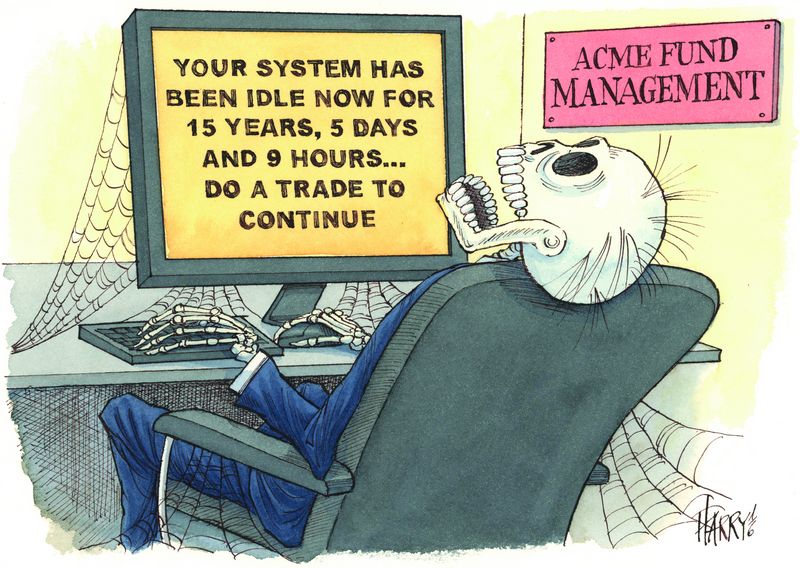

In terms of volatility things might be in the process of becoming fundamentally worse. One of the most significant but underreported events of 2016 was the merger of the two asset managers Henderson and Janus in an all-share deal. This was not an aggressive expansion by the one or the other but a defensive move by two active asset managers who see their business being eroded by passive funds. The rise and rise of the passive fund is, by the by, yet another result of the low interest rate environment.

Back to brass tacks

I reflected recently on the problem facing hedge funds. If one is leveraging 6% rates three times, one returns 18%. One can take fees of “2 and 20” out of that and still give the punter a generous return. If one is leveraging rates of 0.5% three times, one gets just 1.5%.

I know this is a gross oversimplification but when one strips out all the beta-disguised-as-alpha and go back to brass tacks that’s broadly all that’s left of the hedge fund model.

The simple truth is that long-only active managers are also being squeezed by the low return environment because a normal fee structure struggles to be supported by the underlying returns.

Passive funds can theoretically be managed by computers with no mortgages, no school fees and no dreams of owning a Porsche. Not surprisingly, they are much cheaper to run and, where fees chew up such a large proportion of the return, it’s no surprise that they look so attractive to end-users.

Subsequently, the passives are growing like Topsy while the actives are struggling to hang on. The result is the merger of Henderson and Janus in a drive towards greater efficiency – or, in plain English, cost savings.

Feel the fees

While we have all spent a large part of this year contemplating the issues surrounding Deutsche Bank and the “too big to fail” phenomenon, we are at the same time watching a similar situation – or problem, if you prefer – developing within the asset management space. Never mind plurality, feel the fee structure.

If there is one thing the internet has brought with it, it is the belief that information and knowledge (or wisdom, if you prefer) are the same thing and that they are a free gift. As the old chestnut has it, knowledge is to know that a tomato is a fruit but wisdom tells us not to put it in a fruit salad.

No actively managed fund can outperform quarter after quarter, year after year (unless of course it is managed by Bernie Madoff). But why, for heaven’s sake do clients expect this to happen or, more to the point, why are they so scared of it not happening?

Rapid growth

It has been suggested that about a fifth of assets are managed in passive vehicles but that the proportion is growing rapidly. A passive fund does nothing other than buy the aggregate of all active managers’ trades and positions. Now imagine there was only one active investor in the world and all other managers would have to follow his or her moves because he or she would be the only one who could move relative pricing.

One CIO wrote to me on the subject: “I have long held the view that the rise of passive funds will see us sleep walk into dysfunctional markets where the last active manager standing ends up making investment decisions for the whole world.”

The mouse squeaks and the herd of elephants stampedes.

Muscle-bound oafs

The centripetal effect risks creating a small cabal of muscle-bound oafs, not only of the index-tracking type but also of the actively managed ilk. Much has been written about the liquidity mismatch although, not having been tested too hard – other than maybe in February – nobody has yet been taken to the woodshed.

Problems moving chunks of assets were demonstrated in the aftermath of the Brexit referendum in June when UK real estate funds were forced to circle the wagons. I am of course not trying to compare an ETF with a property fund but the circumstances that led to the latter having to close for redemptions reminded us that all the modelling in the world cannot account for investors panicking. But what if it’s not panicking investors but the necessity to match an index that triggers an instant need to sell … and sell in volume?

There has also been increasing talk this year of stress-testing mutual funds. The greatest protection against violent market movements is the plurality of investment strategies and dispersion of funds. The greatest threats to markets, in my humble opinion, are the concentration of assets and the mistaken belief that there is safety in numbers.

In the same way in which we were taught that one should never effect an investment based on tax considerations, so it would also appear to make sense not to choose one’s investment manager based on fees – especially considering the destructive power of strict “best execution” or “lowest price at all cost” requirements.

The Janus/Henderson trade is being touted as a defensive action. If more mergers of the same ilk follow in the coming months or years – and no doubt they will – the world will be a poorer place.

Who would have thought a decade ago that by 2016 one-third of the global beer market would be controlled by a single company? Perish the thought that in 10 years from now there might be investment firms with the same reach. In the mean time, mine’s a pint.

To see the digital version of this review, please click here.

To purchase printed copies or a PDF of this review, please email gloria.balbastro@tr.com