From moving inexorably up the maturity curve, through reinstating its auction programme, to exiting its EU/IMF bailout, Portugal made strides in returning to funding normality in 2014. It rode the wave of tightening yields, taking advantage of every opportunity that came its way. The Republic of Portugal is IFR’s SSAR Issuer of the Year.

Portugal took advantage of 2014’s benign market environment to return to a funding pattern more in line with normal market conditions, putting behind it its €78bn EU/IMF bailout programme and making a dent in its 2015 requirements.

Its 10-year yield more than halved over the course of the year – from more than 6% to less than 3%. And although this did not necessarily set it apart from its peripheral peers, what did was the fact that it “managed to monetise the improvements every step of the way”, said Myriam Zapata, a director in the SSA DCM team at Credit Agricole CIB, which acted as a bookrunner on two of the sovereign’s four syndicated issues.

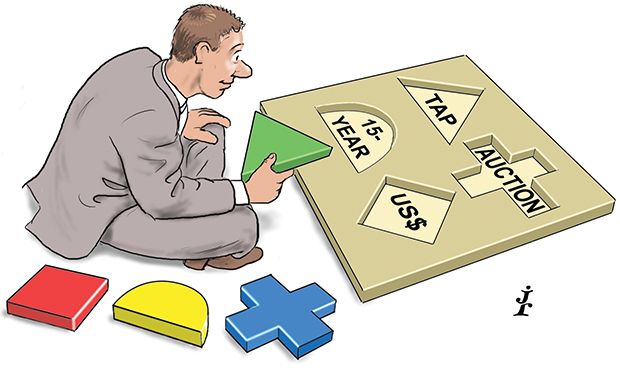

It started its assault on the market early on in the year, when it tapped its 4.75% June 2019 issue for €3.25bn on January 9. The results were encouraging for a country that had seen itself frozen out of the international scene – some 88% of the bonds were placed overseas. In all, demand topped €11bn from around 280 accounts.

“It is an expression of investors’ continued confidence in Portugal’s ability to fund as it looks to exit its bailout programme,” said Fabianna Del Canto, managing director, European syndicate at Barclays, one of the banks managing the deal.

With the trade, Portugal raised more than a quarter of the €11bn–€13bn in bond issuance envisaged for 2014, a number that included some pre-funding for 2015, and it returned just a month later with another tap, this time having the confidence to stretch out to the 10-year part of the curve.

This €3bn doubling of its 5.65% February 2024 issue followed a similar pattern, with a slightly lesser allocation to non-domestic accounts (83%) and a smaller book (€9.8bn), although the number of accounts involved crept closer to the 300 mark, at 292.

Its next trip to the syndicated market was not until July, although the interim saw it take an important step towards full normalisation, when it reinstated its auction programme in April after a three-year hiatus.

Here again, Portugal rode the wave of contracting yields, its success giving it greater freedom to decide whether to make a clean break from its bailout or seek the backstop of a precautionary loan, said Treasury secretary Isabel Castelo Branco.

“The fact that Portugal can now finance itself on its own in the market, meeting investor expectations and capturing demand that did not exist a few months ago, obviously gives us greater capacity to decide,” she said.

The choice to exit was taken just a month later and the sovereign then returned in July with what was seen as the deal that solidified its full rehabilitation into the international capital markets – its first US dollar transaction since 2010.

Investor demand was a substantial US$10bn from about 310 accounts, which allowed the sovereign to tighten the spread by 10bp from the initial price thoughts and also upsize the deal by US$500m from the US$4bn originally launched.

North America gave the nation’s return the thumbs up, accounting for 86% of the paper, the vast majority being placed with real-money investors.

All the more remarkable was the fact that the issue came amid a gathering storm regarding concerns around the Espirito Santo group.

Portugal returned to the syndicated market one more time, again pushing the boundaries.

September saw it sell €3.5bn of a new long 15-year, upsized from €3bn on the back of some €9bn of demand. Perhaps the most notable distribution statistic was that just 5.9% of the paper was placed domestically.

This acceptance saw it embark on an exchange in November, switching investors in 2015 and 2016 maturities into longer tenors, further easing its redemption profile.

“Maybe Portugal was not the biggest issuer but it was the one that showed the most spectacular improvement in market access and funding conditions,” said CA-CIB’s Zapata.

To see the digital version of the IFR Review of the Year, please click here.

To purchase printed copies or a PDF of this report, please email gloria.balbastro@thomsonreuters.com.