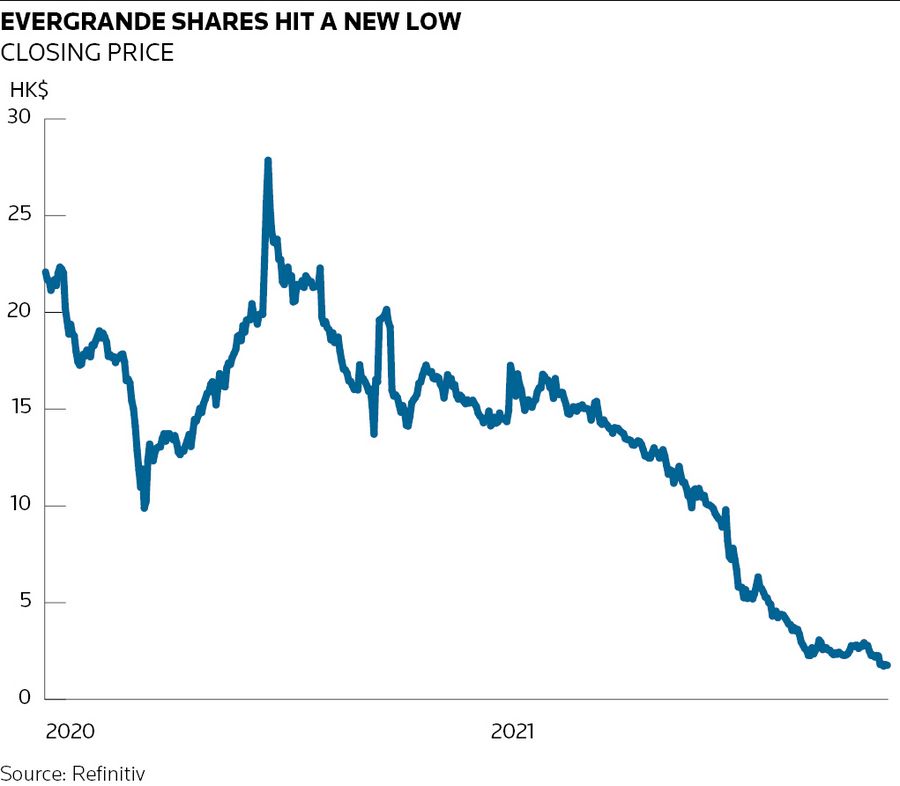

China Evergrande Group is in technical default, marking the largest offshore bond default from an Asian issuer.

The developer failed to pay an overdue US$82.5m bond coupon by December 6, the end of a 30-day grace period.

The failed payment marks the company's first offshore default on a public bond, and will trigger cross-default provisions on around US$19bn of international bonds.

Evergrande, once China's top property developer, has more than 1,300 real estate projects and around US$300bn in liabilities, but has been struggling to service its bonds since September.

Evergrande's missed payment was confirmed by a source close to the bondholders, as well as Fitch. The ratings agency on December 9 downgraded Evergrande and its subsidiaries, Hengda Real Estate Group and Tianji Holding, to RD (restricted default), from C, following the non-payment. Fitch affirmed the senior unsecured ratings of bonds issued by Evergrande and its subsidiaries at C, with a recovery rating of RR6. Historically, RR6 securities only recover up to 10% of their principal and related interest following a default.

The next steps for Evergrande are unclear as the company has yet to make an official statement about its missed payment and did not immediately respond to a request for comment.

Evergrande had said in a filing on December 3 that it may not be able to fulfil its pledge to guarantee payment on US$260m of debt, details of which it did not provide, and it planned to restructure its offshore obligations. The Guangdong provincial government summoned Evergrande's chairman Hui Ka Yan and sent a working group to the company to "oversee risk management, strengthen internal controls and maintain normal operations".

On December 6, the last day of the grace period for the missed coupon payment, Evergrande said it had set up a risk management committee that includes officials from state-owned entities which "will play an important role in mitigating and eliminating the future risks of the group".

Market participants have been left to speculate about how the government will control the Evergrande implosion, and if bondholders have any hope of curtailing losses. As of the end of September, Evergrande bondholders included Eastspring Investments, BlackRock, AllianceBernstein and Ashmore, according to Refinitiv data. None of the firms responded to requests for confirmation that they still hold Evergrande notes.

"I'm not sure what a ‘risk management committee’ is but my guess is that this is a unique case given the size [of the debt], and the central and provincial government is asking Evergrande to proactively manage the fallout and not have a messy default," said a portfolio manager, who does not hold Evergrande bonds. "I don’t really think it will work."

One DCM syndicate banker reckoned the lack of investor noise around the default is a sign that Evergrande is already in negotiations with its bondholders. The company is likely to make a formal announcement after it has finalised more details, she said.

A Hong Kong-based lawyer said a slower announcement may be better for bondholders as it provides more time for Evergrande to assess its assets, in particular its more opaque onshore holdings, to better tackle its debt.

“I would expect that the company comes forward with a proposal to the offshore guys [bondholders] that includes all of the offshore bonds in one go,” said the lawyer. “I’m personally struggling to see them formulate this proposal in the near term because they don’t know yet what is going on onshore, how much they can keep control over the completion of ongoing projects” or how much they will sell or dispose of these projects.

Government intervention

Government involvement does not necessarily benefit bondholders, and market watchers think a bailout is unlikely.

Instead, the Chinese government is keen to keep mainland property buyers happy by completing Evergrande's unfinished projects, said the syndicate banker.

“The government ultimately has limited love for the offshore bondholders,” said the lawyer. “That said, I’m not necessarily of the view that the government is out there with a mission to inflict pain on the offshore bondholders. For them, it’s a bit of an afterthought.”

Andrew Sheng, a distinguished fellow at the Asia Global Institute of the University of Hong Kong, said Evergrande had systemic implications on the housing market, given its size, "so it would not be surprising that if the largest liabilities of the borrower is to housebuyers, then the contractual obligations of the company would need to be taken into consideration".

A Greater China DCM head from a European bank said it was clear that creditors closer to the assets would get paid first. "All other bonds have similar terms, you can't say that if the government's priority is to ensure project completion and delivery it is putting bondholders at a disadvantage."

A person close to Evergrande said the company intended to follow international market standards and principles in dealing with its restructuring, and aimed to "formulate and implement a viable restructuring plan" of its offshore debt for the benefit of all stakeholders.

Offshore bondholders will be structurally and contractually subordinated to those onshore with operational and financial exposure when Evergrande undergoes restructuring. Its US dollar bonds were trading at mid-10s to mid-20s handle, reflecting the market's weak expectations for recovery.

China has yet to voice a clear shift in policy with regard to the embattled property sector, but there have been signs that its tone is softening.

The People's Bank of China and China Banking and Insurance Regulatory Commission have tried to reassure the market, saying that any risks from Evergrande's problem to the broader property sector can be contained.

In addition, the PBoC on December 6 cut the bank reserve ratio requirement by 50bp, a move widely viewed as a signal of policy easing. The message sent out from the Politburo, the ruling Communist Party's top decision-making body, also fuelled speculation that the government might adopt a more dovish approach towards property companies.

"We've seen more step-in this time, with different government departments coming out to calm the market," said a DCM head from a Chinese investment bank. "Stability is the main concern and the government's priority is to ensure project completion and delivery to homebuyers. The ultimate outcome of the restructuring, however, is hard to say."

The DCM head said the government had intervened in the Evergrande case because of the company's size. The government was likely to allow smaller players to go bankrupt, unless it increased instability, he said.

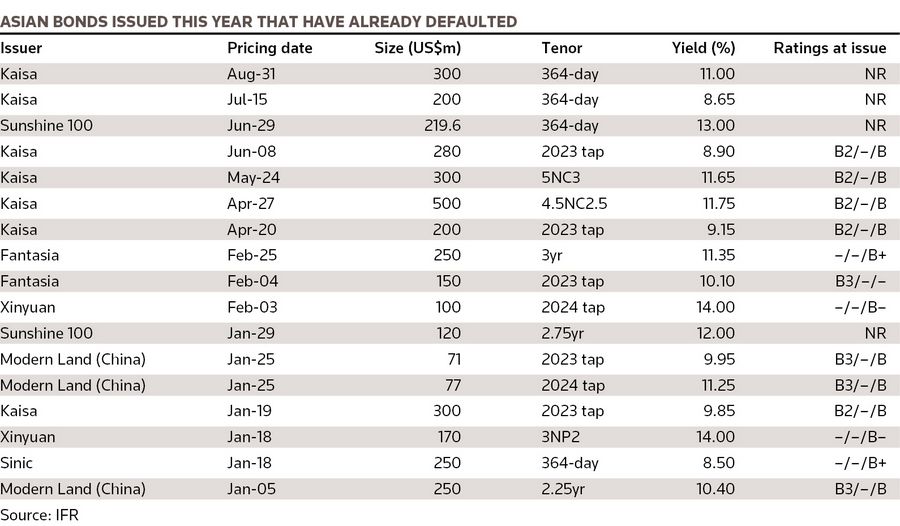

Kaisa defaults

Evergrande's default was followed by that of Kaisa Group Holdings, which failed to pay its US$400m 6.5% senior notes due on December 7 after bondholders rejected a proposal to extend the maturity, according to a source close to the situation. There is no grace period for the bond repayment, and the missed payment will trigger a cross-default on other notes.

Kaisa has about US$12bn of offshore debt.

Like Evergrande, Kaisa is yet to make an official announcement about the missed payment. The company did not immediately respond to a request for comment.

Fitch on December 9 cut Kaisa's issuer rating to RD from C. The ratings agency affirmed the senior unsecured ratings of Kaisa's bonds at C with a recovery rating of RR4.

Given the size of Evergrande and Kaisa, in terms of their property projects and debt, both visible and invisible intervention from the authorities is expected during any restructuring process to limit contagion risk, said market participants. But ultimately the default of both companies had been long expected, and the market was ready for their fall.

"The market has already anticipated the default of Evergrande and Kaisa, reflected in both the stock and bond prices," said the European bank's Greater China DCM head. "I don't think the defaults in themselves this week have much impact on the market."